In most cases, home insurance must be in the name of the homeowner. This is because the person named on the home insurance policy is considered to have an insurable interest in the property, meaning they have a reason to want coverage. If the homeowner does not live in the property, the insurance policy should be written as a dwelling fire insurance policy.

However, there are ways to include other people on a homeowner's insurance policy. For example, if the person is related to the homeowner through marriage, adoption, or blood, they are automatically covered under the policy. Unmarried cohabitating partners can be included through an Other Members of the Household endorsement or an Additional Insured endorsement.

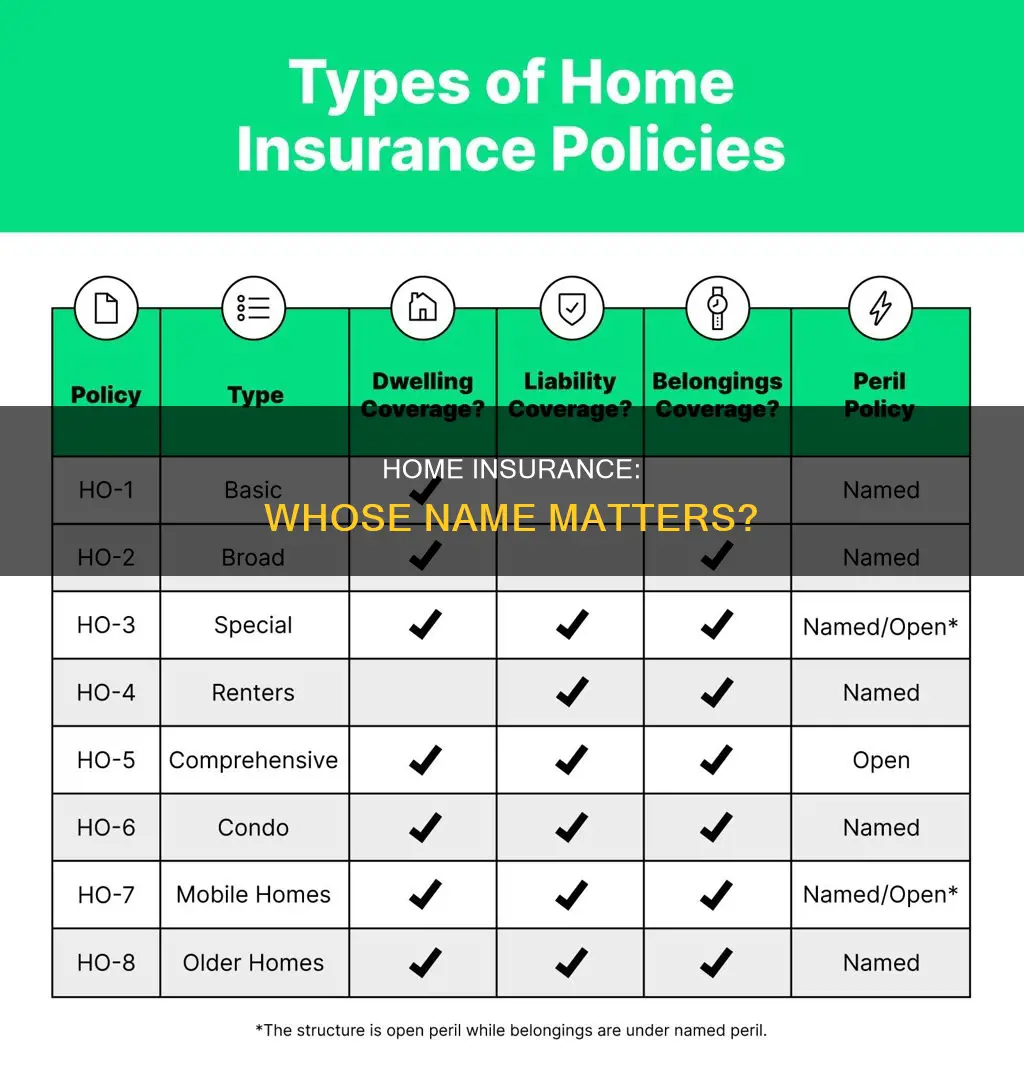

| Characteristics | Values |

|---|---|

| Who should be listed on home insurance? | The named insured, who can make changes to the policy, cancel it, or make a claim. |

| Is it necessary for all household members to be listed? | No, if one household member is the named insured, anyone related to them through marriage, adoption, or blood is covered under that policy. |

| What about unmarried cohabitating partners? | They can be covered by an "Other Members of the Household" endorsement or an "Additional Insured" endorsement. |

| Who is defined as a "Named Insured"? | Any individual or organization with a financial stake in a company or a piece of property. |

| Who is covered by the policy? | The party protected by the policy is known as the named insured. |

| What happens if the insured person dies? | The estate becomes the temporary insured until the end of the policy period, after which the policy will not be renewed. |

| What about financing companies, lienholders, or mortgagees? | They should be recorded on the policy as additional insured or loss payee but will not be named insured. |

Explore related products

What You'll Learn

![]()

Home insurance and property ownership

However, it's important to note that not everyone who lives in the home needs to be listed on the policy to be covered. For example, if the policy lists one household member as the named insured, anyone in the household who is related to that person through marriage, adoption, or blood is typically also covered under that policy. Additionally, anyone under the care of the named insured, such as a foster child, would also be covered.

For unmarried cohabitating partners, there are a couple of options to ensure that both partners are covered by the homeowner's insurance policy. One option is to add an "Other Members of the Household" endorsement, which would provide the second person with the same coverage as the named insured. Another option is to add an "Additional Insured" endorsement, which would provide the partner with more specific coverage under the policy.

It's also worth noting that if the property is transferred to someone else, such as an adult child, it's important to update the home insurance policy to reflect the new owner. The insurance name must match the name on the deed to ensure that the policy is effective and that the correct individual is covered.

In summary, while the homeowner's insurance policy should be in the name of the property owner, there are ways to include other household members or partners on the policy to ensure that they are also covered. It's always a good idea to consult with an insurance expert to determine the best way to structure your policy to fit your unique situation.

Farmers Insurance: The Reliable Choice for Customized Coverage

You may want to see also

Explore related products

![]()

The named insured

In the case of home insurance, the named insured is typically the owner of the property. This is because most insurance companies require anyone getting an insurance policy to have an insurable interest in the property. Owning a home is an insurable interest.

However, it is possible to add someone else to a homeowner's insurance policy. For example, if you own a home and let a family member live there, that family member can be added to the policy as a named insured. In this case, the family member would need to obtain their own renters insurance policy.

It is important to note that not everyone needs to be listed on a homeowner's insurance policy to be covered. If the policy lists one household member as the named insured, anyone in the household who is related to that person through marriage, adoption, or blood is covered under that policy.

Additionally, there are other ways to include someone on a homeowner's insurance policy. For example, unmarried cohabitating partners can be added with an "Other Members of the Household" endorsement or an "Additional Insured" endorsement.

Farmers Insurance Honk: The Sound of Reliable Roadside Assistance

You may want to see also

Explore related products

![]()

Additional insured

Typically, home insurance has to be in the name of the owner. Most insurance companies require anyone getting an insurance policy to have an insurable interest in the property, which means owning a home or vehicle. Therefore, the owner's name must be on the home insurance policy. However, there are scenarios where an additional insured person or entity is added to the policy.

An additional insured person or entity is added to an insurance policy on top of the main policyholder (the named insured). The named insured is the person who took out the policy and their name is on it. Under most home insurance policies, the coverage will automatically include the named insured's immediate relatives, their spouse, and their children, as long as these individuals also live in the home.

The key difference between a named insured and an additional insured is that the former is the owner of the property and has the ability to make changes to the policy, cancel it, or make a claim. An additional insured person or entity also receives coverage under the policy and has the ability to make claims. They must have an insurable interest in the property, meaning they must have some financial stake or degree of ownership. For example, if you buy a home with a partner you are not married to, one partner would be the named insured, and the other would be an additional insured.

An additional insured endorsement can be beneficial as it extends coverage. The additional insured can file a claim, and it shouldn't impact their coverage or rates. However, it can raise the price of the policy, and rates may go up if there is a claim.

The Insurance Advocate: May Nardone's Dedication to Farmers

You may want to see also

Explore related products

$24.85 $28

![]()

Home insurance and cohabitation

Home insurance is a necessity for protecting your home and assets. When it comes to cohabitation, it's important to understand how your insurance policy applies to those living with you. Here are some key points to consider:

Owner's Name on Home Insurance

Home insurance typically needs to be in the name of the property owner. This is because insurance companies require the policyholder to have an "insurable interest" in the property, which means owning the home or having a financial stake in it. So, if you don't own the home, you usually can't be the sole policyholder.

Cohabitation and Coverage

If you live with family members or unrelated individuals, it's important to ensure they are covered by your home insurance policy. While those related by blood, marriage, or adoption are often automatically covered, unmarried partners and roommates may not be. Check with your insurance provider to confirm who is covered under your specific policy.

Endorsements for Unmarried Partners

If your unmarried partner is not listed on the deed of the property, they may not be covered by your home insurance policy. In this case, you can purchase an "Other Members" endorsement to extend coverage to them. This protects their belongings and provides liability coverage. Consult your insurance agent to determine the best way to include them in your policy.

Renters Insurance

If your partner or roommate is not covered by your home insurance, they should consider purchasing renters insurance. This will protect their personal belongings and provide liability coverage. In some cases, the homeowner's insurance company may offer a joint renters policy for both residents, which can be more cost-effective.

Homeownership and Marriage

When it comes to homeownership and marriage, insurance companies have become more flexible. Many companies now offer the same rates and policies to unmarried couples as they do to married couples. This includes writing policies for unmarried couples who jointly own a home.

In conclusion, cohabitation can have an impact on your home insurance coverage. It is important to review your policy and make any necessary adjustments to ensure that everyone living in the home is adequately protected. Consult an insurance expert to determine the best way to include your partner or roommate in your policy, and don't hesitate to shop around for the best rates and coverage options.

Farmers Insurance and Unsolicited Calls: Why Your Phone May Be Ringing

You may want to see also

Explore related products

$68.99

![]()

Home insurance and death

Typically, home insurance has to be in the name of the owner of the house. However, in the event of the owner's death, the process of transferring the insurance policy to the beneficiary or new owner is relatively straightforward. Here are some key points to consider regarding home insurance and death:

Timeframe for Notification:

You usually have around 30 days to inform the home insurance company about the policyholder's death. It is essential to notify them within this timeframe to avoid cancellation of the policy.

Provide Necessary Documentation:

When contacting the insurance company, you will need to provide a death certificate to confirm the policyholder's death. It is also recommended to follow up with a phone call to clarify your options and next steps regarding the insurance coverage.

Discuss Coverage Options:

After notifying the insurance company, ask about your options for continuing coverage on the home. In some cases, the insurance company may allow you to keep the current policy in effect until it expires, especially if you are the surviving spouse or a named insured. Alternatively, they may give you a specific timeframe, such as 30 days, to purchase a new policy under your name.

Understand the Impact of Vacancy:

If the home is vacant during the probate process or while waiting for a sale, inform the insurance company. Vacant homes are at greater risk of vandalism and theft, and the insurance company may require you to add vacant home insurance coverage, which can be more expensive.

Consider Temporary Insurance:

During the probate process or if you are unsure about your plans for the property, consider obtaining temporary or short-term home insurance. These policies are typically issued in the name of the estate executor, with beneficiaries listed as additional policyholders.

Transferring the Policy:

If you are the beneficiary or new owner of the property, you will need to transfer the existing policy to your name or take out a new insurance policy. Contact the insurance company and provide proof of ownership to initiate this process.

Consult an Expert:

If you have questions or concerns about your specific situation, don't hesitate to consult a licensed insurance agent or expert. They can guide you through the process and help you navigate any unique circumstances or complexities.

Understanding Glass Buyback in Farmers Insurance Policies

You may want to see also

Frequently asked questions

Yes, house insurance has to be in the name of the owner. The person listed on the home insurance, known as the named insured, has the power to make changes to the policy, cancel it, or make a claim.

In the event of the insured's death, their estate becomes the temporary insured. The policy will not be renewed at the end of the policy period, and the heir will have to negotiate with the insurance company for coverage.

No, you cannot insure a house that you do not own. However, if you are a resident of the house, you can obtain renters insurance to cover your belongings and provide liability insurance coverage.