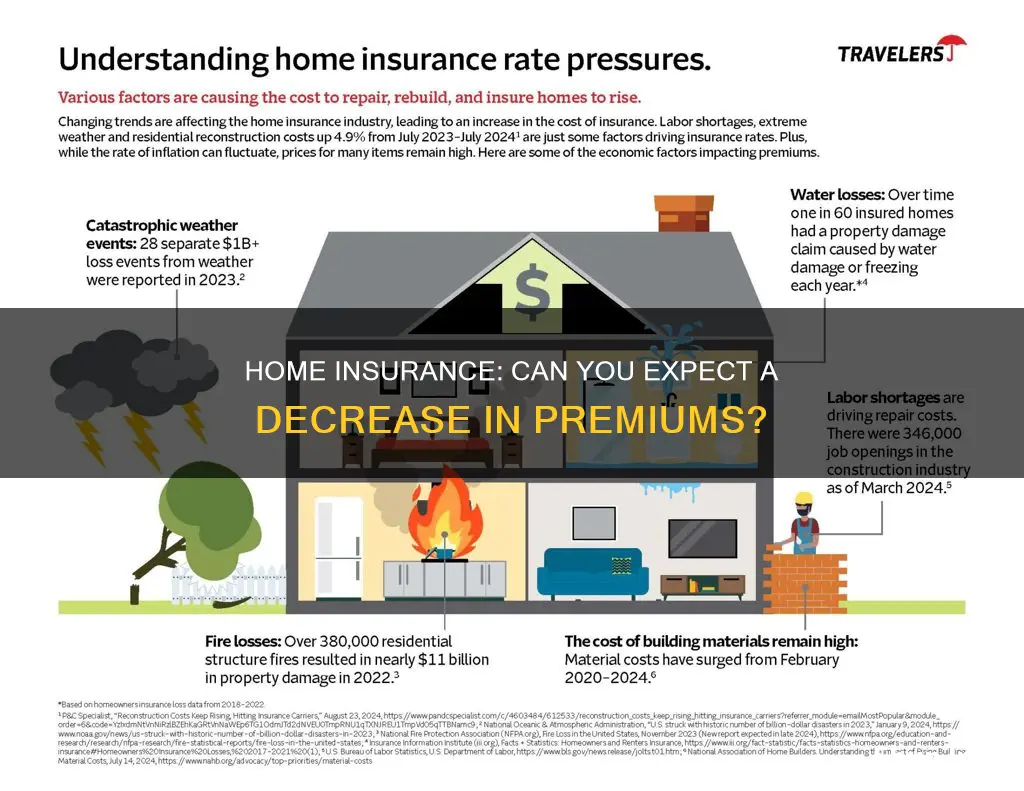

Homeowners' insurance rates have been rising sharply in recent years, outpacing inflation in several US states. This is due to a multitude of factors, including the increased frequency and severity of weather events, such as hurricanes, floods, droughts, and wildfires, which have resulted in costly insurance claims. Additionally, the rising cost of building materials and labour, as well as supply chain issues, have contributed to higher replacement costs when insurance claims are filed. Other factors include the location of the property, the history of filing claims, and the market value of the home. While insurance rates are generally increasing, there are ways to mitigate costs, such as bundling policies, taking advantage of customer retention programs, and installing smart home technology.

| Characteristics | Values |

|---|---|

| Homeowners insurance rates | Rising |

| Factors | Severe weather events, rising cost of building materials, supply chain issues, inflation, skilled labor shortage |

| Impact | Deepening the housing crisis, financial strain on homeowners |

| Solutions | Bundling policies, customer retention programs, comparison shopping, Fair Access to Insurance Requirements (FAIR) plans |

Explore related products

What You'll Learn

![]()

Inflation and insurance rates

Inflation has led to an increase in the cost of building materials, with material goods for new residential construction seeing a sharp rise. This rise in the cost of materials and labour has resulted in higher replacement costs when insurance claims are filed, and as a result, insurance companies are likely to increase premiums to cover these higher costs. The construction industry is facing a skilled labour shortage, which has resulted in added expenses related to wages, supply chain problems, and other construction issues.

Inflation has also impacted the automotive industry, with vehicle values, labour costs, the price of replacement parts, and healthcare costs all rising. This has resulted in higher insurance rates for drivers, as the cost of repairing and replacing vehicles has increased. The semiconductor chip shortage has also contributed to higher-priced cars and repair costs, further impacting insurance rates.

In addition to the direct impact of inflation on the cost of goods and services, insurance rates are also influenced by the likelihood of claims being made and the potential risks involved. For example, in the context of home insurance, severe weather events and natural disasters have become more frequent and destructive, leading to costly insurance claims. As a result, insurers adjust rates based on anticipated weather-related losses, which can drive up insurance premiums.

While inflation has a significant impact on insurance rates, there are steps that individuals can take to mitigate the financial burden. Homeowners can explore discounts, bundle policies, and maintain a good record to potentially lower their premiums. Staying informed about market trends and being proactive about protecting one's property can also help manage insurance costs.

Home Insurance: Lawn Mower Accidents Covered?

You may want to see also

Explore related products

![]()

Natural disasters

Common natural disasters covered by homeowners' insurance include wildfires, tornadoes, and wind or hail damage. However, it is important to review your specific policy as coverage can vary depending on your location and insurance provider. For example, flood damage and earthquakes are typically excluded from standard homeowners' insurance policies and require separate coverage. Additionally, sewer backup is generally not covered under homeowners' insurance or flood insurance and must be purchased separately.

The impact of natural disasters on insurance rates is influenced by several factors. Climate change has heightened the risks associated with wildfires, hurricanes, and flooding. As a result, insurance companies have had to re-evaluate their risk assessments and adjust their rates and coverage accordingly. In some cases, insurers have even exited high-risk areas or stopped offering coverage for certain disasters. This has made it challenging for homeowners in vulnerable areas to obtain affordable insurance.

The financial impact of natural disasters can be significant. Catastrophic events can lead to increased costs for transportation, housing, materials, and labour, affecting not only those directly impacted but also the surrounding areas. This, in turn, can result in higher repair and rebuild costs, further exacerbating the financial burden on homeowners.

It is crucial for homeowners to carefully review their insurance policies and understand the specific coverage provided for natural disasters. Consulting with an agent or insurance provider can help ensure that the policy adequately addresses the risks inherent to the region. Additionally, considering additional coverage options, such as extended or guaranteed replacement cost coverage, can provide further financial protection in the event of a natural disaster.

Comparing Homeowners Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Location and risk

The location of a property is a significant factor in determining homeowners insurance rates. Properties in high-risk areas, such as those prone to natural disasters like hurricanes, floods, droughts, wildfires, and tornadoes, often face higher insurance premiums. For example, states like Florida, California, Louisiana, and Arizona have experienced substantial insurance rate increases due to the frequent occurrence of hurricanes, wildfires, and other storm events.

The construction and building costs in an area can also impact insurance rates. When repairing or rebuilding a home, the cost of materials and labour can vary depending on the location. Supply chain issues, skilled labour shortages, and increased prices for building materials contribute to higher insurance premiums in certain locations.

Insurers typically adjust rates on a state-by-state basis or even specific ZIP codes, taking into account the actual and anticipated weather-related losses and the local construction costs. As a result, homeowners in certain locations may experience more significant increases in their insurance rates compared to others.

Additionally, the age and condition of a house can influence insurance rates. An older house may have higher premiums due to potential repair or maintenance issues. The replacement cost of a home, which refers to the amount needed to rebuild it at current labour and material prices, can vary across locations and impact insurance rates accordingly.

It is worth noting that insurance rates are also influenced by factors beyond location, such as the frequency of severe weather events, inflation, and an individual's history of filing claims. However, location plays a pivotal role in assessing risk and determining the cost of homeowners insurance.

DUI Impact: What Homeowners Need to Know About Insurance

You may want to see also

Explore related products

![]()

Repair and rebuild costs

The impact of severe weather events, such as hurricanes, floods, droughts, and wildfires, has also contributed to the increasing repair and rebuild costs. These events have become more frequent and destructive, leading to costly insurance claims. As a result, insurers have been adjusting rates based on anticipated weather-related losses, which vary from state to state. For example, states like Florida and California, which have experienced a higher number of natural disasters, tend to have higher insurance rates.

The location of the property plays a significant role in insurance rates. Building in wildfire-prone areas or high-risk zones can significantly influence the cost of insurance. Additionally, the market value of a home differs from its replacement cost. The replacement cost refers to the amount needed to completely rebuild the home at the current prices of labour and materials, which have been impacted by pandemic-related disruptions and inflation.

To manage repair and rebuild costs, some insurance companies offer additional living expense (ALE) coverage. ALE coverage provides financial assistance for expenses incurred when forced to live elsewhere due to disasters covered by the homeowner's insurance policy. This includes reimbursement for hotel stays, restaurant meals, emergency clothing, and other costs to maintain the policyholder's standard of living.

While repair and rebuild costs are significant factors in insurance rates, there are other considerations as well. Insurance companies assess the likelihood of claims and potential risks, and factors such as the policyholder's history of filing claims and the property's location in a high-risk area can influence the overall cost of coverage.

Zander Identity Theft Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Discounts and bundling

Homeowners insurance rates have been increasing due to various factors, including the rising cost of building materials, labour shortages, and severe weather events. However, there are ways to keep costs in check and even decrease your premiums through discounts and bundling.

One way to obtain discounts on your homeowners insurance is by bundling your policies. Many insurance companies, such as Travelers, offer discounts when you purchase multiple policies with them. Commonly, homeowners bundle their home and auto insurance policies, but you can also bundle other specialty coverages, such as boat insurance, valuables insurance, or personal umbrella protection. By consolidating your insurance needs with a single provider, you can often unlock cost savings.

In addition to bundling, insurance companies may offer various discounts to reduce your premiums. For example, Travelers offers a premium discount program called the Travelers Decreasing Deductible®, which applies a $100 credit towards your deductible each year at your annual renewal date. Similarly, having a strong track record of on-time payments and maintaining a good insurance score can help make you eligible for discounts with certain providers.

Smart home technology is another way to decrease your homeowners insurance costs. By installing smart devices that offer protection and security, you may be able to reduce your premiums. Additionally, comparison shopping and switching insurers can help you find more favourable rates. It is worth comparing quotes from multiple insurance companies, as pricing and coverage options can vary significantly between providers.

Foal Insurance: Proving Their Worth and Value

You may want to see also

Frequently asked questions

Home insurance premiums have risen sharply throughout the U.S. in the past few years. This is due to a variety of factors, including the increased frequency of severe weather events, the rising cost of building materials, and supply chain issues.

Yes, the location of your home can significantly impact your insurance rates. If your home is in a high-risk area, such as a place prone to natural disasters like hurricanes, wildfires, or floods, your insurance rates may be higher.

There are a few strategies you can use to find cheaper homeowners insurance. Comparison shopping is a good way to start, as rates can vary significantly between companies. You can also look for insurers that offer discounts, such as those that provide a discount when you bundle your home and auto insurance policies. Additionally, maintaining a strong track record of on-time payments can help boost your insurance score and potentially lower your rates.

In addition to location and weather events, other factors that can influence your insurance rates include the age and condition of your home, the cost to repair or rebuild your home in the event of damage, and your history of filing claims.