Homeowners insurance is essential to protect your property and assets. When comparing insurance policies, it's important to understand the different types of coverage and their limits to ensure you're adequately protected without overpaying. You can receive quotes directly from insurance agents, but they may not offer comparisons with other companies. Independent agents can provide more options, and online comparison tools allow you to view multiple quotes simultaneously. When evaluating quotes, consider factors beyond price, such as customer service and financial stability, to ensure the insurer can pay out on claims. By assessing your coverage needs and comparing policies, you can find the right balance of protection and affordability.

| Characteristics | Values |

|---|---|

| Coverage options | Structure or dwelling coverage, personal property coverage, liability coverage, alternative living expenses (ALE) coverage, flood insurance, liability coverage |

| Coverage limits | Coverage limits determine the maximum amount an insurance company will pay out in the event of a claim. |

| Customer service | Read online reviews, check with the National Association of Insurance Commissioners for complaints, and check Consumer Reports' reviews. |

| Financial stability of the insurer | A.M. Best, Moody's and S&P rate insurance companies' financial stability. |

| Discounts | Maintaining good credit can help lower homeowners insurance costs. |

| Quotes | Get quotes from insurance carriers' websites, by calling an insurance agent, or by using an insurance broker or comparison site |

| Cost | Homeowners insurance can cost more than $2,000 per year. |

Explore related products

What You'll Learn

![]()

Understand the different coverage options

Understanding the different coverage options available to you is essential when comparing home insurance policies. Homeowners insurance policies typically include four standard types of coverage:

Structure or Dwelling Coverage

This type of coverage pays for repairs or the rebuilding of your home if it is damaged or destroyed by a covered event, such as a fire, hurricane, hail, lightning, or other disasters. It is important to note that standard homeowners insurance policies do not typically cover flooding or earthquakes, which may require separate coverage. Most policies are designed to cover the full replacement cost of your home, ensuring that you have the financial means to rebuild in the event of a total loss.

Personal Property Coverage

Personal property coverage protects your belongings, including furniture, clothing, sports equipment, and other personal items, in the event of theft or destruction by a covered disaster, such as a fire or hurricane. Most companies provide coverage for a percentage of the insured value of your home, and this coverage often extends beyond your home, protecting your belongings anywhere in the world. However, there may be dollar limits for certain high-value items, such as jewelry, furs, and silverware. To insure these items to their full value, you may need to purchase additional coverage.

Liability Coverage

Liability coverage is a crucial aspect of homeowners insurance, protecting you financially if someone is injured on your property or if you accidentally cause damage to someone else's property. It helps cover medical or legal costs that may arise from such incidents. This type of coverage is especially important if you have features like a pool, frequent visitors, or high-value assets that could increase your risk exposure.

Additional Living Expenses (ALE) Coverage

ALE coverage comes into effect when your home is undergoing repairs or rebuilding after a covered incident. It helps cover the cost of temporary living expenses, such as hotel stays or rental properties, ensuring that you have a place to live while your home is being restored.

In addition to these standard coverage options, there are also different levels of coverage to consider:

- Actual Cash Value Coverage: This type of policy takes into account depreciation when paying to replace or repair your home or possessions. While it may not cover the full replacement cost, it can help offset some of the financial burden associated with covered losses.

- Replacement Cost Coverage: Unlike actual cash value coverage, replacement cost coverage does not factor in depreciation. It pays for the full cost of repairing or replacing your home or possessions, providing better financial protection.

- Guaranteed/Extended Replacement Cost Coverage: This coverage option offers the highest level of protection. It pays whatever it costs to rebuild your home, even if the expense exceeds your policy limits. This type of coverage is particularly valuable in the event of sudden increases in construction costs due to unexpected situations.

Dual Insurance: Worth the Extra Cost?

You may want to see also

Explore related products

![]()

Evaluate your coverage needs

When evaluating your coverage needs, it is essential to understand the different coverage options available to you. Homeowners insurance policies generally include four standard types of coverage:

First, structure or dwelling coverage pays to repair or replace your home if it is damaged or destroyed by a covered event, such as a fire. Make sure your policy provides enough protection to fully rebuild your home and replace your belongings. Note that the cost of rebuilding your home may differ from its market value, focusing on construction costs rather than property value.

Second, personal property coverage pays to replace personal possessions that are damaged, destroyed, or stolen in a covered incident.

Third, liability coverage pays legal and medical costs if someone is injured on your property or if you accidentally cause damage to someone else's property. For example, if a guest slips and falls or your child breaks a neighbour's window, personal liability coverage can help cover these costs. You may want to increase your liability coverage if you have a pool, frequent visitors, or high-value assets that could expose you to higher risks.

Finally, alternative living expenses (ALE) coverage helps cover the cost of living elsewhere during home repairs or rebuilding following an insurance claim.

When comparing policies, pay attention to what is considered a covered loss and ensure protection against common scenarios like fire, theft, and storm damage. Understand the coverage limits, as these determine the maximum payout in the event of a claim. Having the right limits can ensure you fully recover after a loss without facing unexpected expenses.

Additionally, consider add-ons that may not be included in standard policies but could be crucial depending on your location and specific needs. For example, flood insurance is typically not included but could be essential if you live in an area prone to flooding or hurricanes.

Exploring the Unexpected: The Farmers Insurance Museum

You may want to see also

Explore related products

![]()

Compare rates and companies

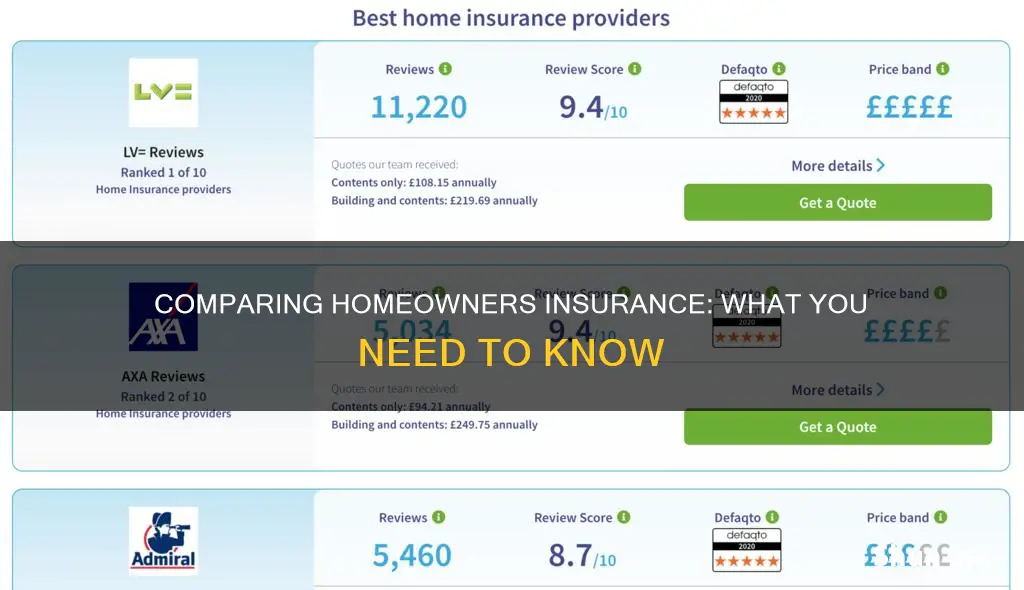

Comparing rates and companies is a crucial step in choosing the right homeowners insurance. It ensures you get the best protection for your home and belongings at a suitable price. Here are some detailed and instructive guidelines to help you compare rates and companies effectively:

Understand Coverage Options and Needs

Before comparing rates, it's essential to understand the different coverage options available. Homeowners insurance typically includes four standard types of coverage: structure or dwelling coverage, personal property coverage, liability coverage, and alternative living expenses (ALE) coverage. Structure coverage pays for repairs or rebuilding if your home is damaged or destroyed by a covered event, like a fire. Personal property coverage replaces your belongings if they are damaged, stolen, or destroyed. Liability coverage takes care of medical and legal costs if someone is injured on your property. Lastly, ALE coverage helps pay for temporary living expenses if you need to live elsewhere during home repairs. Determine which of these coverages are most important to you and any specific risks you may want to insure against, such as floods or increased liability due to a swimming pool.

Get Multiple Quotes

Once you know your coverage needs, it's time to get quotes from multiple companies. You can do this by contacting insurance carriers directly, either through their websites or by calling their agents. For a more efficient approach, consider using insurance brokers or online comparison tools like Gabi or The Zebra, which allow you to compare multiple quotes side by side. When requesting quotes, ensure you provide the same type and amount of coverage to each company for an accurate comparison.

Evaluate Coverage Limits and Deductibles

When comparing quotes, pay close attention to the coverage limits, as these determine the maximum payout in the event of a claim. Evaluate whether the limits are sufficient to fully rebuild your home and replace your belongings. Additionally, consider the standard deductibles, which may be a dollar amount (often starting at $500) or a percentage of the claim payout, and understand how these may impact your finances in the event of a claim.

Consider Customer Service and Financial Stability

Remember that price isn't the only factor. The company's customer service and responsiveness to claims are also essential. Read online reviews, check for customer complaints with the National Association of Insurance Commissioners, and consider paying a small fee to access Consumer Reports' reviews of homeowners insurance companies. Additionally, assess the financial stability of the insurer by checking their ratings with A.M. Best, Moody's, and S.P. to ensure they can pay out on claims.

Maintain Good Credit

Your credit score can impact your insurance costs. Many states use credit-based insurance scores to determine your premiums. Maintaining good financial habits, such as paying bills on time and keeping account balances low, can improve your credit score and potentially lower your insurance rates.

By following these steps, you can effectively compare rates and companies, ensuring you find the right homeowners insurance policy that offers the best protection for your home at a reasonable cost.

Trupanion Pet Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Assess customer service

When comparing homeowners insurance, assessing the customer service of different providers is crucial. Here are some detailed instructions to help you make an informed decision:

Start by checking third-party evaluations and reviews: Look for reputable sources that provide independent assessments of insurance companies and their policies. Sites like J.D. Power, the National Association of Insurance Commissioners (NAIC), Better Business Bureau, and your state's insurance department offer valuable insights into customer complaints and performance. These sources can help you understand how different insurance companies handle claims and interact with their customers.

Consider consumer surveys: Consumer surveys are a great way to gauge customer satisfaction and the overall experience policyholders have had with a particular insurance company. Look for surveys that cover various aspects of customer service, such as the ease of filing a claim, claim status communication, claim resolution, and overall value. U.S. News, for example, conducts consumer surveys and provides valuable insights into the performance of different insurance companies.

Compare customer reviews: Reading customer reviews can provide firsthand accounts of other people's experiences with the insurance company. Look for reviews that discuss the claims process, responsiveness, and overall customer treatment. Websites like The Zebra offer customer reviews, allowing you to understand the experiences of their customers and whether they felt pressured into choosing a particular policy.

Evaluate response times and accessibility: Assess how accessible the insurance company is to its customers. Consider factors such as their availability, response times, and the ease of reaching customer support representatives. Choose a company that values your time and provides prompt assistance when needed.

Research the company's reputation: It is essential to select a reliable and trustworthy insurer. Look into their financial strength score, which indicates their ability to pay out claims. A company with a strong financial standing is more likely to be dependable in the long run.

By following these steps and considering various aspects of customer service, you can make a more informed decision when choosing a homeowners insurance provider. Remember that excellent customer service can provide peace of mind and ensure a smoother experience when dealing with insurance-related matters.

Mortgage Insurance: When Does Lenders' Policy Apply?

You may want to see also

Explore related products

![]()

Evaluate financial stability

When shopping for insurance, it is important to evaluate the financial stability of the insurance company to ensure that they are financially strong enough to pay out claims to their customers, even in the event of a major disaster.

There are several third-party agencies that rate insurance companies based on rigorous analysis of their financial strength. These agencies include A.M. Best, Fitch, Kroll Bond Rating Agency (KBRA), Moody's, and Standard & Poor's. Each agency has its own rating scale, standards, and population of rated companies, and they consider factors such as financial leverage, management stability, recent performance, and the company's overall financial situation.

It is recommended to check the ratings from two or more agencies to get a more comprehensive understanding of the insurance company's financial stability. These ratings can often be accessed for free on the agencies' websites, although some may require registration or a small fee. Demotech, Inc. is another financial analysis firm that specializes in evaluating the financial stability of regional and specialty insurers. They assign Financial Stability Ratings (FSRs) based on an insurer's area of focus and execution of their business model.

In addition to third-party ratings, you can also evaluate an insurance company's financial stability by considering the quality of their investments. High-risk investments, such as junk bonds and defaulted mortgages, have led to the downfall of several large insurance companies. Therefore, it is important to assess an insurer's exposure to such investments and ensure they have limited involvement in high-risk ventures.

By considering the ratings from independent agencies and evaluating the quality of their investments, you can make a more informed decision about the financial stability of an insurance company before purchasing a policy.

Comparing House Insurance: A Quick Guide

You may want to see also

Frequently asked questions

The first step is to determine your coverage needs. You can then get multiple quotes from different companies for the same types and amounts of coverage.

You can get a quote by contacting an insurance agent or insurance company directly, either online, over the phone, or in person. You can also use an insurance broker or an online comparison site such as Gabi or The Zebra.

You will need basic information about your house, including a rough estimate of your home replacement cost. This is the amount it would take to rebuild your home in the case of a total loss and is based on labour and materials.

Homeowners insurance policies generally include four standard kinds of coverage: structure or dwelling coverage, personal property coverage, liability coverage, and alternative living expenses (ALE) coverage. You may also want to consider increasing your liability coverage if you have a pool, frequent visitors, or high-value assets.

Price is an important consideration, but it is not the only one. You should also evaluate the company's customer service by reading online reviews and checking for customer complaints. You can also check the financial stability of the insurance carrier to ensure they can pay out on claims.