When it comes to buying a home, there are various costs to consider, including the down payment and mortgage insurance. The down payment is the initial payment made when purchasing a home, while mortgage insurance, also known as private mortgage insurance (PMI), is an additional cost that protects the lender in case the borrower defaults on the loan. Typically, if the down payment is less than 20% of the home's value, lenders require PMI to mitigate their risk. Increasing the down payment can help buyers avoid PMI, as they are assuming more of the risk, but it may not always result in a lower overall cost. Exploring different loan options, such as special first-time homebuyer programs or VA loans, can also help reduce or eliminate PMI requirements. Understanding the relationship between the down payment and mortgage insurance is crucial for homebuyers to make informed decisions and minimize their overall costs.

| Characteristics | Values |

|---|---|

| What is PMI? | Private mortgage insurance (PMI) is an extra fee for conventional mortgage borrowers putting down less than 20 percent. |

| Who does PMI protect? | PMI protects the lender in case the borrower defaults on the loan. |

| How much does PMI cost? | PMI costs range from 0.30% to 1.15% of your loan balance annually. |

| How does PMI impact monthly payments? | PMI is typically rolled into the monthly mortgage payment and can add a significant amount to the overall cost of the loan. |

| How to avoid PMI? | Put down a 20% down payment, consider a piggyback loan, or explore special first-time home buyer loans without PMI. |

| How to get rid of PMI? | PMI can be cancelled when the loan balance reaches 78% of the home's value or when the borrower reaches an 80% loan-to-value ratio. |

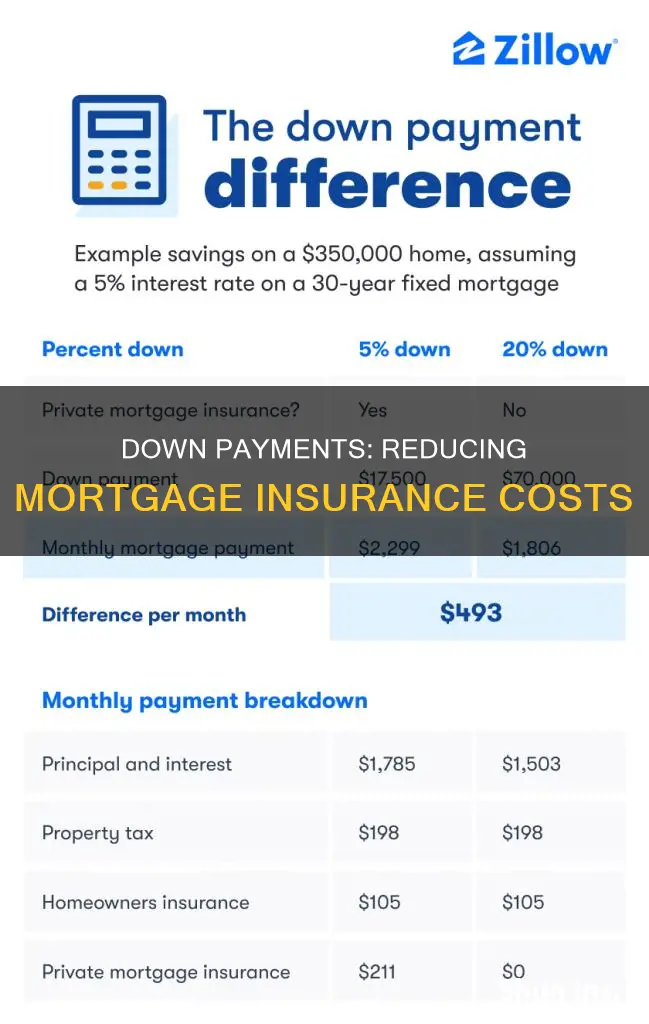

| How does down payment size impact interest rates? | A larger down payment can lead to a lower interest rate offer from the lender as it reduces the risk for the lender. |

| How does down payment size impact mortgage insurance? | A larger down payment can help avoid paying for mortgage insurance, as it reduces the default risk for the lender. |

Explore related products

What You'll Learn

- A down payment of 20% or more means no mortgage insurance is required

- Mortgage insurance protects the lender, not the borrower

- Mortgage insurance can be avoided by taking out a piggyback loan

- Mortgage insurance costs can be reduced by taking out split-premium mortgage insurance

- Lenders may waive mortgage insurance payments for a higher mortgage interest rate

![]()

A down payment of 20% or more means no mortgage insurance is required

A down payment of 20% or more on a conventional loan means that no private mortgage insurance (PMI) is required. PMI is an added insurance policy that protects the lender in the event that the borrower defaults on the loan. Typically, a lender will require PMI if the borrower's down payment is less than 20%. This is because a smaller down payment means less equity in the home and more risk for the lender.

By putting down 20% or more, borrowers can avoid the extra cost of PMI, which is typically rolled into the monthly mortgage payment. However, it's important to note that a larger down payment may result in a higher mortgage rate. This is because an uninsured mortgage, or "conventional" mortgage, costs the bank more, and they must account for the default risk in their portfolio and bottom line.

There are alternative strategies to avoid PMI without a 20% down payment. For example, some lenders offer special low- or no-down-payment mortgages for certain professionals, such as physicians, dentists, and orthodontists. These loan programs often do not require PMI. Additionally, first-time homebuyer programs may offer reduced-cost mortgage insurance or waive PMI altogether. Exploring options like lender-paid mortgage insurance or special loans for first-time homebuyers can also help reduce or eliminate PMI requirements.

While PMI can increase monthly expenses, it also enables homebuyers to enter the market without a large down payment. Once sufficient equity is built, typically at 20%, borrowers can request to cancel PMI. This option may be beneficial if building up a large down payment is challenging, allowing homebuyers to take advantage of favourable economic conditions and become homeowners sooner.

Earthquake Insurance: Is CEA Coverage Worth the Cost?

You may want to see also

Explore related products

![]()

Mortgage insurance protects the lender, not the borrower

Private mortgage insurance, or PMI, is an insurance policy that protects the lender in case the borrower defaults on a home loan. It is typically required if the down payment is less than 20% of the home's purchase price. This ensures that the lender can recover their costs in case of foreclosure. For example, if a buyer purchases a home for $300,000 and only makes a 10% down payment ($30,000), they would typically be required to pay PMI. This is because the down payment is less than 20% of the home's value.

Mortgage insurance is not required for all loans. For instance, Federal Housing Administration (FHA) loans and U.S. Department of Veterans Affairs (VA)-backed loans do not require PMI. Additionally, some lenders offer special low- or no-down-payment mortgages for certain professionals, such as physicians, dentists, and orthodontists. These loan programs typically do not require PMI and may offer other benefits such as excluding medical school debt from the applicant's debt-to-income ratio.

While PMI protects the lender, it can also benefit the borrower by allowing them to qualify for a loan that they might not otherwise be eligible for. However, it is important to note that PMI increases the overall cost of the loan and does not protect the borrower from foreclosure if they fall behind on payments.

To avoid paying PMI, borrowers can increase their down payment to at least 20% of the home's purchase price. This eliminates the need for mortgage insurance and provides the borrower with more options, such as a lower interest rate and access to extra funds. Additionally, once the loan balance drops to 78%-80% of the original loan amount, borrowers can request to cancel PMI payments.

In summary, mortgage insurance primarily serves to protect the lender in case of borrower default. While it is not mandatory in all cases, it can facilitate loan approval for borrowers who may not meet the standard requirements. By increasing their down payment and staying current on their payments, borrowers can avoid the additional cost of PMI.

Beacon's Insurance: Worth the Hype?

You may want to see also

Explore related products

$4.99 $14.99

![]()

Mortgage insurance can be avoided by taking out a piggyback loan

Mortgage insurance, also known as private mortgage insurance (PMI), is typically required if your down payment is less than 20% of the home's purchase price. It protects the lender in case the borrower defaults on the loan. While increasing your down payment to 20% or more can help you avoid PMI, there is another way to do so without having to pay such a large sum upfront: taking out a piggyback loan.

A piggyback loan is a secondary loan that you take out alongside a primary mortgage to avoid paying PMI. It allows you to make a lower down payment, typically 10%, while still reaching the 20% threshold that exempts you from PMI. In an 80/10/10 loan structure, for example, the primary mortgage covers 80% of the sales price, the piggyback loan finances 10%, and the down payment covers the remaining 10%.

Piggyback loans became popular during the housing boom in the early to mid-2000s, with approximately 30% of homebuyers in New York City using this strategy in 2006. However, they have since decreased in popularity due to the expansion of mortgage products that require less than a 20% down payment and do not require PMI. Additionally, piggyback loans come with their own set of costs and risks. They typically have higher interest rates than the first mortgage, and these rates can be variable, increasing over time. There are also additional closing costs associated with taking out a second loan, and having two loans can make it more challenging to refinance or sell your home in the future.

Therefore, while a piggyback loan can be a useful tool to avoid PMI without a large down payment, it is important to carefully consider the potential costs and risks before deciding if this strategy is right for your financial situation.

The Friendly Face of Farmers Insurance: Unveiling the Man Behind the Company's Success

You may want to see also

Explore related products

![]()

Mortgage insurance costs can be reduced by taking out split-premium mortgage insurance

Private mortgage insurance (PMI) is an added expense for borrowers who buy or refinance a home with a down payment of less than 20%. The cost of PMI increases the monthly mortgage payment, so it is important to consider alternatives. One way to avoid paying PMI is to increase the down payment to 20% or more. This reduces the loan-to-value (LTV) ratio to below 80%, which is the threshold at which mortgage insurance is typically required.

Split-premium mortgage insurance is a type of PMI that can help reduce costs for borrowers with a high debt-to-income (DTI) ratio. With this option, borrowers pay part of the mortgage insurance premium upfront as a lump sum at closing, and the remainder in smaller monthly installments. This reduces the upfront cost compared to single-premium mortgage insurance, where the full premium is paid upfront. It also lowers the monthly payments compared to borrower-paid mortgage insurance, where the premium is divided into regular monthly installments.

The upfront premium for split-premium mortgage insurance typically ranges from 0.50% to 1.25% of the loan amount, with the monthly premium based on the net loan-to-value ratio. This option allows borrowers to reduce their monthly mortgage payments, preventing their DTI from rising too high and disqualifying them from the loan. It is important to note that PMI rates vary depending on factors such as the loan amount, down payment, and credit score.

Overall, split-premium mortgage insurance can be a useful option for borrowers with a high DTI ratio, as it provides flexibility in terms of upfront and monthly costs. However, it is important to consider other options, such as lender-paid mortgage insurance or special first-time homebuyer loans without PMI, to find the most suitable choice for an individual's financial situation.

Kinguin Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Lenders may waive mortgage insurance payments for a higher mortgage interest rate

Private mortgage insurance (PMI) is a type of insurance coverage that protects the lender in case a borrower defaults on a home loan. Typically, a lender will require you to pay for PMI if your down payment is less than 20% of the home's value. This is because a smaller down payment means less equity in the home and more default risk for the lender.

One way to avoid paying for PMI is to increase your down payment to at least 20% of the home's purchase price. This will remove the need for mortgage insurance as the lender's risk is reduced. However, this option may not be feasible for everyone, as it requires a larger upfront payment.

Another option to avoid PMI is to consider lender-paid mortgage insurance. Some lenders may waive PMI payments in return for a higher mortgage interest rate. This option can be beneficial for those who cannot afford a 20% down payment but still want to avoid the recurring PMI payments. However, it's important to note that paying a higher interest rate over a longer period may end up being more costly than paying for PMI.

Additionally, there are other strategies to remove PMI without increasing your down payment or mortgage rate. One way is to build up enough equity in your home, typically to at least 20% of the home's value. At this point, you can request PMI cancellation, and once your loan balance drops to 78% of the original value, PMI will be automatically removed. Alternatively, you can also proactively request to cancel PMI payments when you reach an 80% loan-to-value ratio.

In conclusion, while increasing a down payment can help reduce mortgage insurance, there are also other strategies to consider, such as lender-paid mortgage insurance or building up home equity. Each option has its own advantages and considerations, so it's important for homebuyers to understand the various mortgage products and their requirements to make an informed decision.

Insuring an Empty House

You may want to see also

Frequently asked questions

PMI stands for Private Mortgage Insurance. It is an extra fee for borrowers who put down less than 20% of the cost of a home. It protects the lender in case the borrower defaults on the loan.

Increasing your down payment reduces your principal loan amount and, consequently, your loan-to-value ratio (LTV), which could lead to a lower interest rate offer from your lender. A higher down payment means less risk for the lender, and potentially, lower rates.

A higher down payment means you won't have to pay PMI, and you'll save on interest over the life of the loan. With more equity in your home, you'll have access to more options, such as amortization length and access to extra funds.

There are a few ways to avoid paying PMI without increasing your down payment. You could consider a piggyback loan, which is a combination of two loans: one for 80% of the home's price and the other for 10%. You could also look into special first-time home buyer loans without PMI, or a VA loan, which doesn't require a down payment or PMI.