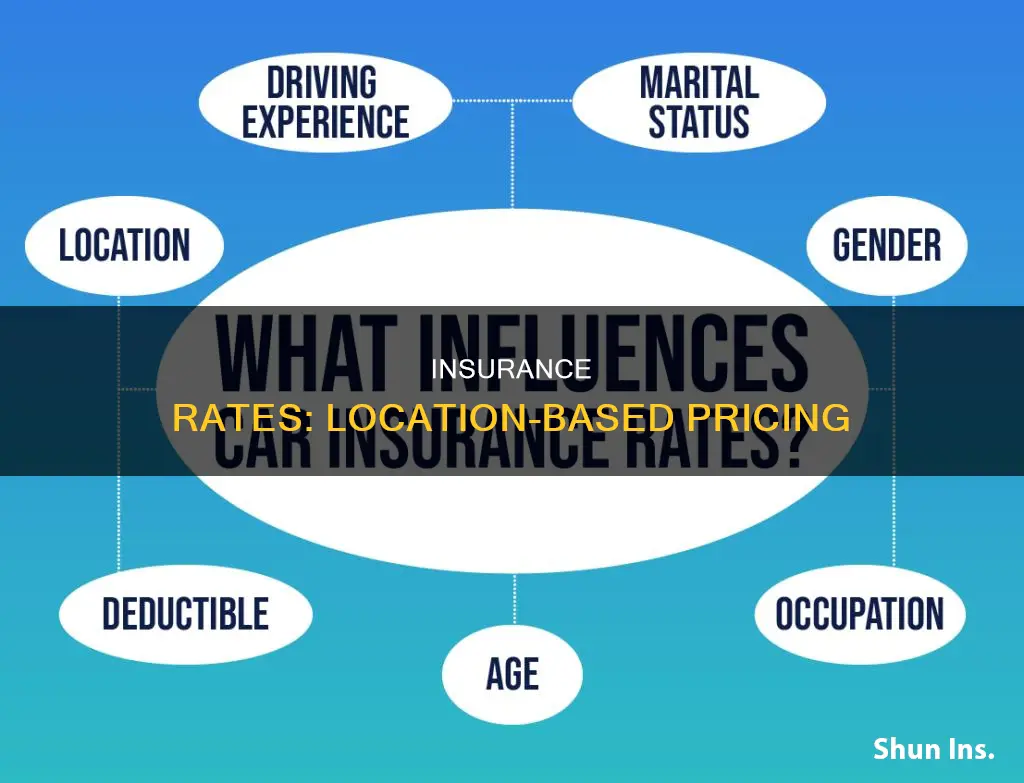

The cost of insurance is calculated based on a variety of factors, including personal factors like age, gender, and marital status, and vehicle-related factors like the make and model of the car, its age, and its safety features. However, location also plays a significant role in determining insurance premiums. Insurance companies consider the type and frequency of claims filed in a particular area, as well as the costs of parts and labor for repairs. Additionally, factors such as crime rates, population density, weather conditions, and road risks can influence the price of insurance in a specific location. As a result, insurance premiums can vary between different cities, neighborhoods, and even ZIP codes.

| Characteristics | Values |

|---|---|

| Type of location | Urban, rural, coastal, etc. |

| Population density | High, low |

| Crime rates | High, low |

| Traffic volume | High, low |

| Average expenses | High, low |

| Natural disasters | Prone, not prone |

| State regulations | Strict, relaxed |

| Number of insurance companies | Monopolistic, competitive |

| Discounts | Available, not available |

Explore related products

What You'll Learn

![]()

Urban vs. rural areas

Insurance premiums are calculated based on a multitude of factors, including personal factors such as age, gender, marital status, driving history, and credit score, as well as vehicle-related factors like the make and model of the car, its age, and safety features. However, location is also a significant factor in determining insurance premiums.

Urban areas, with their high volume of traffic, increased likelihood of theft or vandalism, and higher crime rates, are often considered riskier by insurance companies. As a result, individuals living in these areas may face higher insurance premiums. The cost of repairs and labour in bigger cities can also contribute to higher insurance rates. Additionally, factors like population density and weather conditions can further influence insurance rates, with certain ZIP codes or neighbourhoods deemed higher risk.

On the other hand, rural areas typically have lower traffic and crime rates, resulting in a lower risk profile. However, rural areas come with their own set of risks, such as a higher likelihood of animal collisions. Interestingly, some predominantly rural states, like Montana, have higher-than-average car insurance rates due to residents travelling longer distances as part of their daily routines, increasing the likelihood of accidents.

While location is a key factor, it's important to remember that insurance companies use their own formulas to calculate premiums, and state regulations also play a crucial role in determining car insurance rates. The cost of insurance can vary significantly between different urban and rural areas, so it's always a good idea to compare rates and consider location-specific discounts when shopping for insurance.

CCW Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Crime rates

For instance, if you live in an area with a high rate of vehicle-related crimes, you will likely pay more than residents in other parts of the town with lower crime rates. Insurance companies offer rates based on collective risk, so if you live in a neighbourhood with a high crime rate, your neighbours' insurance claims can also impact your rates.

On the other hand, if you live in an area with low crime rates, you may be eligible for discounted insurance rates. Secure parking or garaging your vehicle can also lead to insurance discounts.

When determining insurance rates, insurance companies also consider the broader location-related factors, such as the state's policy on medical benefits, the risk of natural disasters, and the cost of living. For example, states with strict insurance regulations and a high risk of natural disasters tend to have higher insurance premiums.

It is worth noting that your location is not the only factor influencing insurance premiums. Other factors include your driving history, the type of vehicle you drive, your credit score, and your personal claims history.

Excluding Barns: How Insurance Rates are Affected

You may want to see also

Explore related products

![]()

Natural disasters

The National Oceanic and Atmospheric Administration (NOAA) reported that from 2018 to 2022, 84 billion-dollar disasters (excluding floods) caused over $609 billion in damages, and these costs have continued to rise. The National Flood Insurance Program (NFIP) also reported that 90% of all natural disasters in the United States involve flooding, and the program has struggled to keep up with the volume of claims, leading to significant premium increases.

The impact of natural disasters on insurance rates is not limited to high-risk areas. Even areas less prone to catastrophic events can experience rate increases due to the nationwide impact of these trends. For example, premiums in San Francisco may rise due to wildfires in Los Angeles County. The rising costs of insurance pose challenges for homeowners, insurers, and local governments, threatening the financial stability of homeowners and potentially reducing home sales.

Homeowners in high-risk areas face difficulties in obtaining affordable insurance coverage. The average annual premium for homeowners' insurance increased by nearly 20% between 2021 and 2023, and Florida residents, for instance, are facing unprecedented premium increases due to hurricane damage. Homeowners insurance typically covers additional living expenses that arise when individuals cannot live at home due to covered damage. However, standard policies often exclude coverage for earthquakes and floods, requiring separate policies for these perils.

To mitigate the impact of natural disasters on insurance rates, it is essential to have adequate coverage in place before a disaster occurs. Homeowners should review their policies to ensure they are not underinsured and understand what is eligible for a claim. Additionally, proactive measures such as weatherproofing and fortifying homes can help reduce the severity of damage. Governments can also provide assistance through programs like the Federal Emergency Management Agency's (FEMA) Public Assistance Program, which offers grants and loans to eligible homeowners.

Sutter Health: Insurance Carrier or Not?

You may want to see also

Explore related products

![]()

Vehicle-related factors

Vehicle Type and Features

The type of vehicle you own can significantly impact your insurance rates. Sportier cars, particularly those known for their speed, often incur higher insurance rates due to the increased risk of accidents. Similarly, SUVs may have higher premiums because of the potential damage they can cause with their larger size. Engine size is another factor; vehicles with bigger engines have more horsepower, leading to higher insurance costs. As a result, a six- or eight-cylinder vehicle typically has a higher premium than a four-cylinder model.

Vehicle Cost and Value

The cost and value of your vehicle influence insurance rates. More expensive vehicles tend to be more costly to insure because of their higher purchase price and potential repair costs. Additionally, if your vehicle is financed or leased, you may be required to carry more insurance coverage, increasing your premium.

Vehicle Age and Condition

The age and condition of your vehicle are also considered. Older vehicles may have lower insurance rates because they are less expensive to repair or replace. However, if an older vehicle is in poor condition, it may be more challenging to find affordable insurance due to the increased risk of mechanical failure or breakdowns.

Vehicle Usage and Mileage

Insurance companies consider how you use your vehicle and your annual mileage. If you use your car for business or have a long commute, you're likely on the road more often, increasing your risk of an accident and, consequently, your insurance rates. On the other hand, pay-per-mile insurance programs can offer savings if you drive less by basing your premium on your actual mileage.

Vehicle Safety Features and Technology

Vehicles equipped with advanced safety features and driver-assistance technologies often qualify for insurance discounts. These features may include collision avoidance systems, lane-keeping assist, adaptive cruise control, and more. Insurers recognize the potential for these technologies to reduce accidents and claim severity, leading to lower insurance costs.

Vehicle Modifications and Customizations

Any modifications or customizations made to your vehicle can impact your insurance rates. Performance enhancements, such as engine modifications or upgraded brakes, may increase your premium due to the potential for higher speeds and performance. On the other hand, safety-related modifications, like installing an anti-theft device or advanced security system, can sometimes lead to insurance discounts.

Carrier Name Insurance: What's in a Name?

You may want to see also

Explore related products

![]()

Personal factors

Age

Young and inexperienced drivers are considered high-risk and, thus, pay higher insurance rates. According to the Insurance Institute for Highway Safety, drivers between the ages of 16 and 19 are three times more likely to be involved in a fatal crash than drivers over 20. As a result, premiums tend to decrease as drivers reach middle age and then increase again after 70.

Gender

Women typically pay less for auto insurance than men because they are less likely to be involved in accidents or serious violations and are more likely to wear seatbelts. However, some states prohibit using gender as a consideration in auto insurance rates or approvals.

Marital status

Married people may benefit from lower insurance rates, although this was not explicitly stated in the sources.

Driving history

Your driving record, including your history of moving traffic violations and at-fault accidents, is one of the biggest factors in determining your insurance rates. A history of traffic violations or accidents will likely result in higher premiums. If you have an extensive history of at-fault accidents, traffic violations, or a DUI/DWI conviction, you may struggle to find insurance and may need to resort to non-standard insurance for "risky" drivers.

Credit score

A poor credit score may lead to increased insurance premiums, as insurance companies may view you as a higher risk. However, some companies, such as Nationwide, offer to reconsider your premium if your credit took a hit due to illness, natural disaster, divorce, or other "extraordinary life circumstances."

Type of vehicle

The type of car you drive can significantly impact your insurance rates. Insurance companies will consider the make and model of your car, its age, and its safety features. For example, a brand-new sports car will typically cost more to insure than an older, safer model. Additionally, past claims from similar models, repair costs, theft rates, and comprehensive claims payments are also taken into account.

NY's No-Fault Insurance: What's Covered?

You may want to see also

Frequently asked questions

Yes, insurance companies use your address to determine the cost of your insurance premiums.

Insurance companies calculate your likelihood of an auto accident based on the county or state in which you live. They also calculate your risk of vehicle theft or vandalism based on the city or neighborhood in which you live.

If you live in a densely populated urban area, you may be at a higher risk of being involved in a car accident due to the high volume of traffic. On the other hand, if you live in a rural area with low traffic, your risk level may be lower.

Car theft and vandalism typically occur while a vehicle is parked, so the location where your car is usually parked plays a significant role in calculating your odds of theft or vandalism.

If you normally park on the street, you may be able to reduce your rates slightly by parking in a locked garage instead. If your car contains theft-deterrent equipment, you may save a small percentage on your premium.