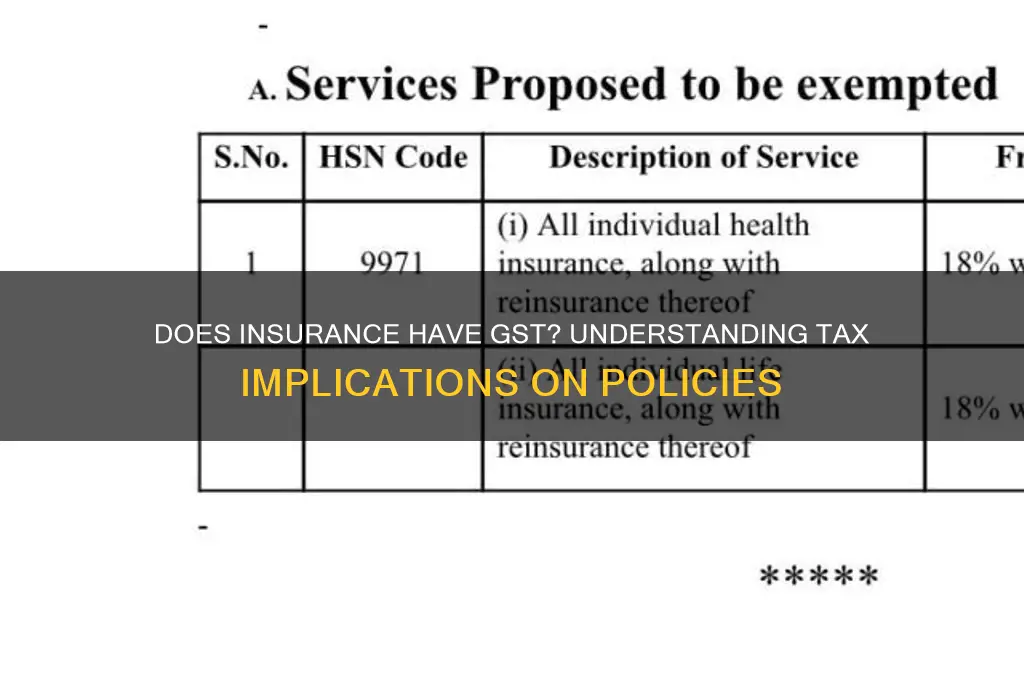

The question of whether insurance is subject to Goods and Services Tax (GST) is a common concern for policyholders and businesses alike. In many countries, including India, insurance services are indeed taxable under GST, but the rates and applicability can vary depending on the type of insurance. For instance, life insurance premiums are generally exempt from GST, while general insurance, such as health, motor, and property insurance, typically attracts a standard GST rate. Understanding the GST implications on insurance is crucial for accurate financial planning and compliance with tax regulations, as it directly impacts the overall cost of insurance policies and the claims process.

Explore related products

What You'll Learn

![]()

GST on Life Insurance Premiums

In India, the Goods and Services Tax (GST) is a comprehensive indirect tax levied on the supply of goods and services. When it comes to GST on Life Insurance Premiums, it’s essential to understand that life insurance services are indeed subject to GST, but the applicability and rate are specific. As of the latest regulations, life insurance premiums attract a GST rate of 18%. This tax is not levied on the entire premium amount but rather on the service component of the premium, which includes charges like policy administration, underwriting, and other related services. The investment portion of the premium, which is allocated towards savings or investment, is exempt from GST.

The introduction of GST on life insurance premiums replaced the earlier service tax regime, which was at a rate of 15% (including cess). The current 18% GST rate applies to all life insurance products, including term plans, endowment policies, unit-linked insurance plans (ULIPs), and others. Policyholders must pay this tax as part of their premium, and insurers are responsible for collecting and remitting it to the government. It’s important for policyholders to note that GST is not deductible under Section 80C of the Income Tax Act, unlike the premium itself, which qualifies for tax benefits.

For insurers, the GST on life insurance premiums is a pass-through cost, meaning it does not impact their profitability directly. However, it does increase the overall cost for policyholders, which could influence their decision-making when purchasing life insurance. Insurers are required to issue tax invoices clearly mentioning the GST amount separately from the premium, ensuring transparency for the policyholder. Additionally, insurers can claim input tax credit (ITC) on GST paid for certain business expenses, but this does not apply to policyholders.

Policyholders should also be aware that GST is applicable on other charges related to life insurance, such as policy renewal fees, rider premiums, and service charges. For instance, if a policyholder opts for additional riders like critical illness or accidental death benefit, the premium for these riders will also attract 18% GST. Similarly, any late fees or penalties for delayed premium payments may also be subject to GST, further adding to the overall cost.

In conclusion, GST on Life Insurance Premiums is a significant consideration for both insurers and policyholders in India. While the 18% tax rate applies to the service component of the premium, it increases the overall cost of life insurance. Policyholders must factor this into their financial planning, while insurers must ensure compliance with GST regulations, including accurate invoicing and timely remittance of tax. Understanding these nuances is crucial for making informed decisions regarding life insurance purchases and maintaining financial preparedness.

Life Insurance: Maturity Before Death?

You may want to see also

Explore related products

![]()

Health Insurance GST Applicability

In India, the applicability of Goods and Services Tax (GST) to health insurance is a topic of significant interest for policyholders and insurers alike. Under the GST regime, insurance services are classified as a supply of service, and thus, they are subject to GST. Specifically, health insurance premiums are taxed at a rate of 18% GST, which is applicable on the service component of the premium. This means that when you pay your health insurance premium, a portion of that payment goes towards the GST, which is then remitted to the government by the insurance provider.

The GST on health insurance premiums is levied on the entire premium amount, including the base premium and any additional charges such as rider premiums or service fees. It’s important to note that the GST is not applicable on the entire amount paid towards health insurance if the policy includes a savings or investment component, such as in the case of unit-linked health plans (ULHPs). In such cases, GST is only applied to the service portion of the premium, which typically includes the risk cover and administrative charges. Policyholders should carefully review their policy documents to understand how GST is calculated and applied to their specific plan.

For group health insurance policies provided by employers, the GST applicability remains the same. The 18% GST is levied on the premium paid by the employer for providing health insurance coverage to employees. However, employees do not bear this cost directly, as it is part of the employer’s expenditure. It’s worth mentioning that certain health insurance schemes, such as those offered under government-sponsored programs like Ayushman Bharat, may have different GST treatments or exemptions, but these are specific cases and not applicable to standard health insurance policies.

Policyholders should also be aware that GST paid on health insurance premiums is not eligible for tax deduction under Section 80D of the Income Tax Act. While the premium itself qualifies for tax benefits, the GST component does not. This distinction is crucial for individuals planning their tax savings and insurance investments. Insurers are required to clearly mention the GST amount separately in the premium receipts and policy documents, ensuring transparency for policyholders.

In summary, health insurance premiums in India attract an 18% GST, which is applied to the service component of the policy. This applies to both individual and group health insurance plans, with specific considerations for policies that include investment components. Understanding the GST applicability on health insurance is essential for policyholders to accurately budget for their premiums and comply with tax regulations. Always consult with your insurance provider or a tax advisor for detailed information tailored to your specific policy and circumstances.

Life Insurance Record Retention: How Long to Keep Them?

You may want to see also

Explore related products

![]()

GST Rates for General Insurance

In India, the Goods and Services Tax (GST) is applicable to various services, including general insurance. The GST rates for general insurance are standardized across the country, ensuring uniformity in taxation. As of the latest regulations, general insurance services attract a GST rate of 18%. This rate is applicable to premiums paid for policies such as motor insurance, health insurance, home insurance, and other non-life insurance products. It is important to note that this rate is levied on the gross premium charged by the insurance provider, excluding any cess or surcharge that may apply separately.

The introduction of GST replaced the earlier service tax regime, which had a rate of 15% on insurance premiums. The increase to 18% under GST means policyholders now pay a slightly higher tax on their insurance premiums. However, GST also subsumed multiple indirect taxes, simplifying the tax structure. For instance, the earlier service tax, Swachh Bharat Cess, and Krishi Kalyan Cess were consolidated into the single GST rate, making it easier for both insurers and policyholders to comply with tax regulations.

It is crucial for policyholders to understand that the GST paid on insurance premiums is not eligible for input tax credit, as insurance is considered a personal expense. This means businesses cannot claim GST paid on general insurance premiums as a credit against their GST liability. Additionally, insurers are required to collect and remit the GST to the government, ensuring compliance with tax laws. Policyholders should carefully review their insurance invoices to verify the correct application of the 18% GST rate.

Certain exemptions and special cases exist within the GST framework for general insurance. For example, life insurance policies are exempt from GST, as they are treated differently under the tax law. Similarly, specific government-mandated insurance schemes may have different tax treatments. Policyholders should consult their insurance providers or tax advisors to understand any exceptions that may apply to their specific policies.

In summary, the GST rate for general insurance in India is 18%, applied to the gross premium of non-life insurance policies. This rate ensures a standardized tax structure across the country, replacing the earlier service tax regime. While GST simplifies taxation, policyholders must be aware of its implications, including the inability to claim input tax credit. Staying informed about GST rates and exemptions is essential for making financially sound decisions regarding general insurance.

Understanding Insurance Coverage Under Your Parents' Plan

You may want to see also

Explore related products

![]()

Input Tax Credit on Insurance

In the context of Goods and Services Tax (GST), understanding the applicability of Input Tax Credit (ITC) on insurance premiums is crucial for businesses and individuals alike. When considering the question, "Does insurance have GST?" it’s important to note that most insurance services, including general insurance, health insurance, and life insurance, attract GST at the rate of 18% in India. This GST is levied on the premium paid by the policyholder. However, the eligibility for claiming ITC on these GST payments depends on the nature of the insurance and its usage for business purposes.

For businesses, the Input Tax Credit on insurance premiums can be claimed if the insurance is directly related to taxable business activities. For instance, if a company purchases health insurance for its employees or insures its business assets, the GST paid on these premiums can be claimed as ITC. This is because such insurances are considered input services that contribute to the furtherance of business. The key condition is that the insured asset or service must be used for business purposes, and the business must be GST-registered. If the insurance is for personal use or for assets not related to business, ITC cannot be claimed.

It’s essential to maintain proper documentation to claim ITC on insurance premiums. Invoices or premium receipts must clearly mention the GST amount paid, the policy details, and the GSTIN (Goods and Services Tax Identification Number) of the insured party. Additionally, the insurance policy should be in the name of the business entity claiming the ITC. Failure to provide accurate and complete documentation may result in the disallowance of the credit by tax authorities.

Another critical aspect is the reversal of ITC if the insured asset is used for both business and personal purposes. In such cases, ITC can only be claimed proportionately, based on the extent of business use. For example, if a vehicle insured for business purposes is also used for personal reasons, the ITC must be apportioned accordingly. This ensures compliance with GST laws and avoids potential penalties for incorrect claims.

Lastly, certain types of insurance, such as life insurance, are exempt from GST, and hence, no ITC can be claimed on such premiums. Businesses should carefully review the GST applicability on different insurance products to determine their eligibility for ITC. Staying updated with GST regulations and consulting tax professionals can help in maximizing ITC benefits while ensuring compliance with legal requirements. In summary, while insurance premiums generally attract GST, the availability of ITC depends on the business relevance and proper documentation of the insured services.

Infosys' Life Insurance: What Cover Does It Provide?

You may want to see also

Explore related products

![]()

GST Exemption on Specific Policies

In the realm of insurance, the application of Goods and Services Tax (GST) varies across different types of policies, with certain categories enjoying exemptions. The GST exemption on specific insurance policies is a crucial aspect that policyholders and insurers alike need to understand to ensure compliance and avoid unnecessary tax burdens. This exemption is primarily aimed at providing relief to individuals and businesses on essential insurance covers, thereby promoting financial security and risk management.

One of the key areas where GST exemption applies is health insurance. Most health insurance policies, including individual and family floater plans, are exempt from GST. This exemption extends to critical illness covers, maternity benefits, and other add-ons that are part of a comprehensive health insurance policy. The rationale behind this is to make healthcare more affordable and accessible to the general public. However, it's important to note that certain ancillary services, such as administrative charges or optional riders, might still attract GST.

Another significant category under GST exemption is life insurance. Traditional life insurance policies, term insurance plans, and endowment policies are typically exempt from GST. This exemption is designed to encourage individuals to secure their families' financial future without the added cost of taxation. However, unit-linked insurance plans (ULIPs) and certain investment-oriented policies may have different tax treatments, as they combine insurance with investment components. In such cases, the investment portion might attract GST, while the insurance component remains exempt.

Agricultural insurance is another sector that benefits from GST exemption. Policies covering crops, livestock, and other agricultural assets are exempt to support farmers and ensure food security. This exemption is particularly vital in countries with a significant agrarian population, as it helps mitigate the financial risks associated with unpredictable weather and market conditions. By removing the GST burden, governments aim to make agricultural insurance more affordable and encourage wider adoption among farmers.

Lastly, export credit insurance is often exempt from GST to promote international trade. This type of insurance protects exporters against the risk of non-payment by foreign buyers. By exempting it from GST, governments aim to reduce the cost of doing business internationally, thereby boosting export activities. This exemption is especially beneficial for small and medium-sized enterprises (SMEs) that may have limited financial resources to absorb additional tax costs.

Understanding the GST exemption on specific insurance policies is essential for both consumers and providers. It not only helps in making informed decisions but also ensures compliance with tax regulations. Policyholders should carefully review their insurance documents to identify any applicable GST charges, while insurers must accurately apply exemptions to avoid legal and financial repercussions. By leveraging these exemptions, individuals and businesses can optimize their insurance costs and enhance their overall financial planning.

Globe Life Insurance: Waiting Periods and You

You may want to see also

Frequently asked questions

Yes, insurance services in India attract Goods and Services Tax (GST). The GST rate varies depending on the type of insurance. For most general insurance policies (e.g., health, motor, home), the GST rate is 18%. For life insurance policies, the GST rate is 18% on the service component (e.g., policy administration fees).

Yes, GST is applicable on life insurance premiums, but only on the service component. The premium itself is not taxed, but the charges related to policy administration, rider fees, or other services are subject to 18% GST.

Yes, health insurance premiums are subject to GST. The GST rate for health insurance policies is 18%, which is included in the premium amount payable by the policyholder.

No, GST does not apply to insurance claims or payouts. GST is levied only on the premium paid for the insurance service, not on the amount received as a claim settlement.