Car insurance rates are typically higher for younger drivers, with rates decreasing annually for drivers between the ages of 16 and 24. While some sources suggest that rates stabilize around 25, others indicate that rates continue to decrease gradually through the driver's late twenties and thirties. Various factors influence car insurance rates, including age, gender, driving experience, location, credit score, and past claims. While age is a significant factor, it is important to consider other variables that insurance companies use to determine their rates.

| Characteristics | Values |

|---|---|

| Car insurance rates decrease | Each year for drivers between 16 and 24 |

| Biggest drops | At ages 19 and 21 |

| Gender | Young men typically pay higher rates than young women |

| Rates decrease | Steadily throughout the early twenties |

| Rates stabilize | Around age 30 to 34 |

| Rates increase | In senior years |

| Rates vary | State by state and company by company |

| Rates increase | If certain risk factors change, such as causing an accident or purchasing a more expensive vehicle |

| Rates decrease | With a clean driving record |

| Rates decrease | With a clean credit history |

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

What You'll Learn

![]()

Insurance rates decrease annually for drivers aged 16-24

Insurance rates for drivers aged 16-24 decrease annually, with the most significant drops occurring in the late teens and early twenties. This is because insurance companies consider drivers in this age bracket as high-risk due to their inexperience and the behaviours associated with young drivers, such as risky driving and lower seatbelt usage. As drivers in this age group gain experience, their insurance rates will gradually decrease. By the time they reach 25, they will have graduated from the highest-risk category, and their premiums will be significantly lower than when they started driving.

The exact amount that insurance rates decrease each year for drivers aged 16-24 varies depending on several factors. These include the driver's gender, location, credit score, vehicle type, and driving history. For example, young men typically pay higher insurance rates than young women due to differences in accident rates, violation patterns, and vehicle choices. Additionally, drivers with a history of at-fault accidents, speeding tickets, or insurance lapses may find that their rates decrease more slowly or may even increase.

While insurance rates generally decrease annually for drivers aged 16-24, it is important to note that this trend can be interrupted or reversed if risk factors change. For example, purchasing a more expensive vehicle or causing an accident may result in higher insurance rates, regardless of age. Additionally, insurance companies use different formulas to calculate rates, so it is beneficial for drivers to shop around and compare quotes from multiple companies to find the most affordable option for their specific situation.

In some cases, insurance rates may temporarily increase when a driver turns 18. This is because the restrictions on a graduated license are typically removed at this age, and insurers may view this as an increased risk. However, as the driver gains more experience and moves towards their mid-twenties, their insurance rates will continue to decrease annually.

Overall, while insurance rates for drivers aged 16-24 do decrease each year, the amount of decrease varies depending on a variety of factors, and it is essential for drivers to actively compare rates and maintain a clean driving record to ensure they receive the best rates possible.

Florida's Double Auto Insurance Policy Rules

You may want to see also

Explore related products

![]()

Rates drop significantly between 18 and 19

Insurance rates are determined by a number of factors, including age, gender, driving history, credit score, and location. Age is a significant factor in determining insurance rates, with younger drivers paying more for insurance than older drivers. This is because insurance companies classify young drivers as high-risk due to their inexperience and the increased likelihood of exhibiting unsafe driving behaviours. As a driver ages, their insurance rates generally decrease as they gain more experience and develop better driving skills and judgment.

While some sources claim that insurance rates start to decrease around age 25, others suggest that the biggest drops in insurance rates occur in the late teens and early twenties, especially between the ages of 18 and 19. During these years, insurers see more driving experience and lower risk, which leads to lower premiums. It is worth noting that insurance rates for young drivers can vary depending on the state and company, and some insurance companies may even raise their quotes around the age of 18.

One reason for the decrease in insurance rates between the ages of 18 and 19 is the accumulation of driving experience. In the United States, many drivers obtain their license before the age of 18, giving them several years of driving experience by the time they reach their late teens and early twenties. As they gain experience, young drivers naturally outgrow risky behaviours associated with inexperience, such as lower seatbelt usage and missing road hazards. This leads to a lower risk profile and, consequently, lower insurance rates.

In addition to age and driving experience, gender also plays a role in insurance rates for young drivers. Young men typically pay higher insurance rates than young women due to differences in accident rates, violation patterns, and vehicle choices. However, this gender gap in insurance rates is more pronounced before the age of 25. By the time drivers reach their mid-twenties, the impact of age and gender on insurance rates begins to decrease, and other factors such as driving history and location become more significant in determining insurance premiums.

It is important to note that while insurance rates generally decrease with age, this trend can be interrupted or reversed if certain risk factors change, such as causing a car accident or purchasing a more expensive vehicle. Additionally, insurance rates may start to increase again in a driver's senior years due to age-related factors such as slower reaction times and vision changes, which can increase the risk of accidents and the cost of medical care.

Auto Insurance in California: What's the Minimum Legal Requirement?

You may want to see also

Explore related products

![]()

Male drivers pay more than females

Car insurance rates are known to decrease each year for drivers between the ages of 16 and 24, with the most significant drops occurring at ages 19 and 21. By the time they reach 25, their insurance rates have likely dropped by half compared to when they were teenagers. This is because insurance companies consider drivers aged 16 to 24 to be high-risk, so rates decrease as the driver gains experience and moves away from that category.

However, male drivers, especially those under 25, often face higher insurance rates than their female counterparts. This is because insurers consider young male drivers to be a higher risk due to differences in accident rates, violation patterns, and vehicle choices. According to the National Highway Traffic Safety Administration, men are more likely to be involved in fatal accidents due to speeding and tend to drive cars that are more expensive to insure. An FBI report also found that men are twice as likely to be arrested for serious driving violations, such as DUIs. As a result, young men may be more likely to purchase a sports car, speed, or take risks behind the wheel. These factors contribute to higher insurance rates for male drivers compared to females in the same age group.

The difference in insurance rates between young male and female drivers can be significant. On average, young men pay 14% more per year for car insurance than young women. This gap narrows as drivers age, with male drivers between 20 and 24 paying 8% more than female drivers. After a driver's 25th birthday, the difference in insurance premiums between men and women becomes negligible.

It is worth noting that some states in the US, such as California, Hawaii, Massachusetts, Michigan, North Carolina, and Pennsylvania, have prohibited the use of gender as a rating factor for car insurance premiums. In these states, insurance companies are required to charge identical rates for male and female drivers.

While gender is a factor in determining insurance rates, it is not the only consideration. Driving experience, age, credit score, driving history, and other risk factors also play a role in setting insurance premiums. Additionally, shopping around for insurance and comparing rates from different companies can help individuals find the most affordable coverage, regardless of their gender.

Auto Insurance in Florida: Affordable or Not?

You may want to see also

Explore related products

![]()

Premiums stabilise in your 30s

Car insurance rates are typically highest for teenagers and young adults. Premiums decrease each year for drivers between the ages of 16 and 24, with the most significant drops occurring at ages 19 and 21. By the time a driver reaches their early twenties, the cost of auto insurance generally begins to drop. This is because insurance companies consider drivers aged 16 to 24 to be high-risk due to their inexperience and the behaviours that come with youth. As drivers gain experience, they develop better driving skills and judgement, which leads to lower insurance rates.

While car insurance rates usually start going down in the mid-twenties for men and the mid to late twenties for women, the rate reductions plateau after that. By the time drivers reach their thirties, their premiums stabilise and remain relatively stable until they reach their fifties. At this point, age-related factors such as slower reaction times and vision changes can increase the risk of accidents, leading to higher premiums.

It is worth noting that age is not the only factor influencing car insurance premiums. Other factors such as location, credit score, driving history, and vehicle type also play a role in determining rates. Additionally, each insurance company uses a unique formula to determine its rates, so it is beneficial to shop around and compare quotes from multiple companies to find the most affordable option.

Navigating Non-Owners Auto Insurance: A Comprehensive Guide

You may want to see also

Explore related products

![]()

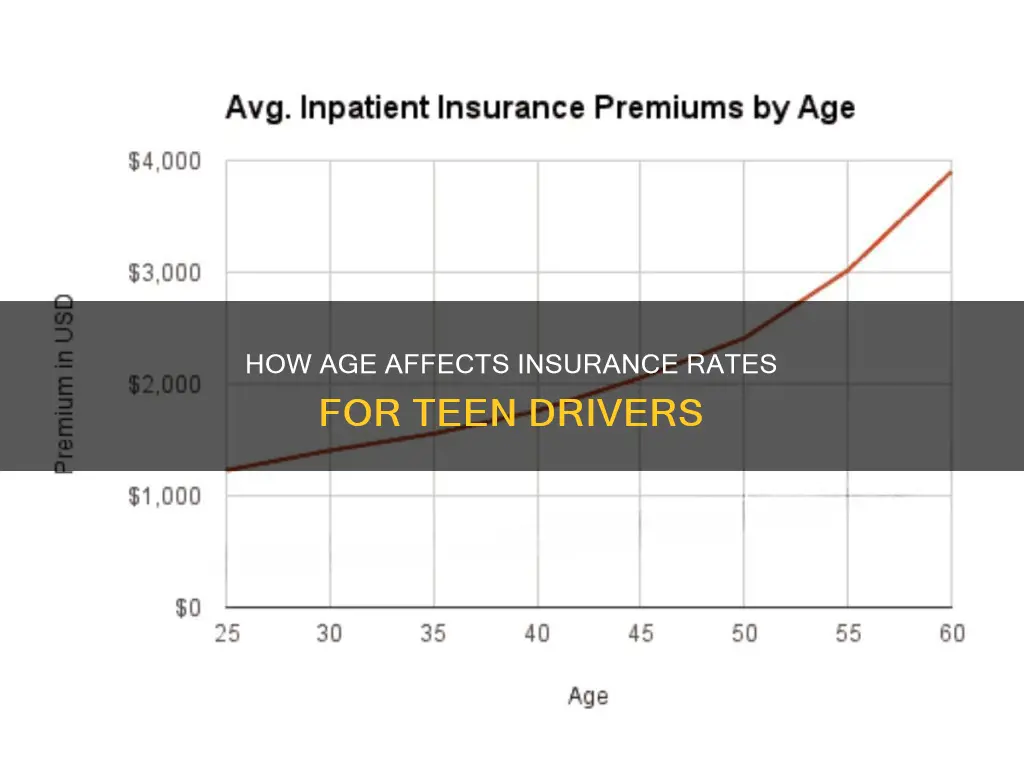

Rates may increase again in your 50s

Car insurance rates are typically highest for teenagers and young adults, with rates decreasing each year for drivers between 16 and 24. The largest decreases occur between the ages of 18 and 19, with rates stabilizing around 25. This is because younger drivers are considered high-risk due to their inexperience and the behaviours associated with youth. As drivers gain experience, they develop better driving skills and judgement, which leads to lower insurance rates.

While rates continue to decrease gradually through a driver's twenties and thirties, they eventually stabilize and remain relatively consistent until the driver reaches their fifties. At this point, rates may start to increase again due to age-related factors. For instance, as drivers approach 70, they may experience slower reaction times and changes in vision, which can increase the risk of accidents and lead to higher premiums. Additionally, older drivers may experience slower recovery and complications from injuries, increasing the cost of medical care and personal injury protection coverages.

It is important to note that insurance rates are influenced by various factors beyond age, including gender, location, credit score, driving history, and vehicle type. Gender, for example, plays a significant role, with young men typically paying higher rates than young women due to differences in accident rates, violation patterns, and vehicle choices. However, the impact of gender on insurance rates varies across states, with some states prohibiting the use of gender as a rating factor.

While age is a crucial factor in determining insurance rates for young drivers, it becomes less significant as drivers gain experience and age. Other factors, such as driving history, credit score, and vehicle choice, also come into play and can influence insurance rates regardless of age. Therefore, while rates may increase again in a driver's fifties due to age-related factors, it is essential to consider the interplay of these other factors in understanding the overall trend of insurance rates over a driver's lifetime.

Dental Claims: Auto Insurance Submission Guide

You may want to see also

Frequently asked questions

It depends on a variety of factors. While some insurance companies may raise their quotes around the age of 18, others may lower them. The biggest price cuts happen in the late teens and early twenties, especially between 18 and 19, as insurers see more experience and lower risk.

Insurance companies classify young drivers as high-risk due to their inexperience and increased likelihood of exhibiting unsafe driving behaviours. As you get older and gain more experience behind the wheel, insurance companies consider you a lower risk to insure, which causes your premium to drop. Other factors that influence the cost of insurance include location, credit score, driving history, vehicle type, and past claims.

To save on car insurance as a young driver, you can change your coverage levels, increase your deductibles, or switch to a pay-per-mile plan if you drive infrequently. Shopping around and getting quotes from different insurance companies can also help you find the cheapest option.