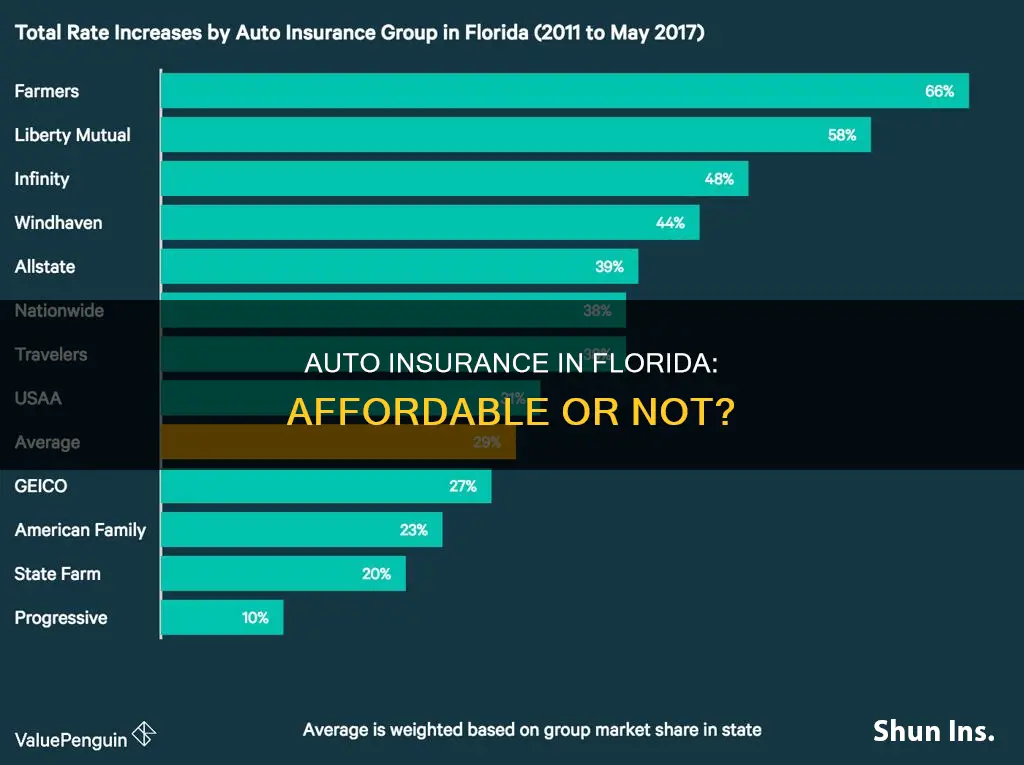

Car insurance in Florida is more expensive than the national average, with drivers in the state paying an average of $1,841 for a 6-month policy, which is 68% more than the national average. The Zebra's experts have analysed Florida car insurance quotes for multiple driver profiles, coverages, and companies to match you with the best policy.

The cheapest liability coverage in Florida is offered by Travelers, with an average monthly cost of $169, which is cheaper than Florida's average of $244 a month. The cheapest full coverage insurance in Florida is also offered by Travelers, at $168 per month.

Florida is a no-fault state, which means that regardless of who causes a car accident, each driver’s insurance covers medical expenses for them and their passengers. Florida is one of the few states that does not require bodily injury liability coverage.

| Characteristics | Values |

|---|---|

| Average annual cost of car insurance in Florida | $3,792 |

| Average monthly cost of car insurance in Florida | $316 |

| Average annual cost of minimum-liability coverage in Florida | $1,605 |

| Average monthly cost of minimum-liability coverage in Florida | $134 |

| Cheapest car insurance in Florida | Geico |

Explore related products

What You'll Learn

![]()

Florida's auto insurance rates are higher than the national average

Florida is among the most expensive states for auto insurance. Florida drivers pay $134 per month or $1,605 per year on average for minimum-coverage auto insurance. This is nearly twice the national average for minimum coverage, which is $72 per month or $869 per year. When it comes to full-coverage car insurance, drivers in the Sunshine State pay an average of $316 per month or $3,795 per year. This is around 42% more expensive than the national average cost of $223 per month or $2,681 per year.

Florida is a no-fault state, which means that regardless of who causes a car accident, each driver’s insurance covers medical expenses for them and their passengers. Florida is one of the few states that does not require bodily injury liability coverage. It’s important to note that property damage liability coverage only pays for damage to another person’s vehicle. For that reason, many Florida drivers choose to purchase full-coverage policies that include both collision coverage and comprehensive protection. Collision insurance pays for damage to your vehicle from an accident you cause, while comprehensive coverage protects your car against damage from natural disasters, theft and vandalism.

Auto Insurance at 21: Is $130 a Good Deal?

You may want to see also

Explore related products

![]()

Florida is a no-fault state

Florida's no-fault law requires drivers to carry a minimum of $10,000 in personal injury protection (PIP) insurance and $10,000 in property damage liability (PDL) insurance. PIP insurance pays for 80% of all reasonable and necessary medical expenses arising from a car accident, including emergency transportation, hospitalizations, surgical procedures, nursing services, dental work, and more. It also provides 60% of your gross wages and loss of future earning capacity if you cannot work because of your injuries. Additionally, PIP provides a $5,000 death benefit per covered individual.

The no-fault law also places restrictions on when you may seek compensation from another party. If you have severe injuries, you may be able to pursue compensation from the party who caused your crash through a claim against their liability insurance or a personal injury lawsuit. In such cases, you must prove that the other party's negligent actions caused the accident.

Mercury Auto Insurance: Understanding Your Coverage Options

You may want to see also

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UY218_.jpg)

![]()

Florida has the highest volume of litigated auto claims in the US

In 2024, Florida's car insurance rates have been fluctuating, with the average annual premium jumping from $1,544 in 2015 to $3,038 in 2024. Notably, in 2022, premiums rose by $498, and in 2024, there was a further increase of $211.

The state's high insurance costs can be attributed to various factors, including its large number of uninsured drivers, higher-risk drivers, unpredictable weather, and mandatory insurance laws. Florida's position as a no-fault state also plays a role, as drivers are required to carry personal injury protection instead of bodily injury liability coverage.

The high volume of litigated auto claims in Florida has led to significant financial losses for insurance carriers. In 2020, Florida carriers lost over $1.6 billion due to excessive litigation, reinsurance costs, and natural catastrophes. As a result, insurance companies have been taking extreme measures, such as enacting coverage restrictions and increasing rates.

To address the issue of litigated auto claims, Florida's legislature passed tort reform in March 2023. However, despite this reform, Florida continues to experience a high volume of litigated auto claims, with 20,000 to 30,000 personal injury lawsuits being filed each month.

Does Your Homeowners Insurance Actually Cover AC Units?

You may want to see also

Explore related products

![]()

Florida has an above-average number of uninsured drivers

The high number of uninsured drivers in Florida is one of the reasons why insurance costs in the state are so high. Florida drivers pay amongst the highest average auto insurance rates in the US. The average cost of a full-coverage auto insurance policy in Florida is $3,069 per year, or $256 per month. This is compared to a national average of $1,543 per year.

Florida's status as a no-fault state also contributes to high insurance costs. In Florida, drivers are required to carry Personal Injury Protection (PIP) coverage, which means that insurance companies must cover their own policyholders in the event of an accident, regardless of who is at fault. This leads to increased costs for insurance companies, which are then passed on to customers in the form of higher premiums.

The high number of uninsured drivers in Florida can also be attributed to the state's minimum insurance requirements. Florida only requires drivers to maintain $10,000 of Personal Injury Protection (PIP) coverage and $10,000 of property damage liability (PDL). This is a relatively low amount compared to other states, and it means that many drivers in Florida are underinsured. As a result, insurance companies must charge higher premiums to offset the cost of covering accidents involving underinsured drivers.

To protect themselves from the high number of uninsured and underinsured drivers in Florida, many residents choose to purchase additional insurance coverage. This includes "uninsured and underinsured motorist insurance," which will cover the cost of repairs and medical bills in the event of an accident with an uninsured or underinsured driver. This added coverage can provide peace of mind, but it also comes at an additional cost, further increasing the overall cost of auto insurance in Florida.

Whose Commercial Auto Insurance Covers Me?

You may want to see also

Explore related products

![]()

Florida has a high rate of insurance fraud

This issue is further exacerbated by Florida's previous "one-way attorney fee" system, where the insurance company was responsible for the plaintiff's legal fees if they lost the case. This system has since been abolished, but it has contributed to the current crisis, with insurance companies facing underwriting losses of over $1 billion in 2020 and 2021. The high rate of insurance fraud in Florida has led to increased premiums for homeowners and the collapse of several insurance companies, with many others choosing to leave the state or significantly increase their rates.

Truckers' Auto Insurance: The Inside Lane on Discounts

You may want to see also

Frequently asked questions

No, auto insurance in Florida is more expensive than in other states. The average cost of car insurance in Florida is $316 per month for full coverage, which is 42% higher than the national average of $223 per month.

The cost of auto insurance in Florida is determined by factors such as age, gender, location, vehicle type, marital status, and credit history.

The minimum auto insurance requirement in Florida is $10,000 in personal injury protection (PIP) and $10,000 in property damage liability insurance.

Yes, driving without auto insurance in Florida can result in the suspension of the driver's license, registration, and vehicle tags for up to three years, as well as fines ranging from $150 to $500.

Some ways to save money on auto insurance in Florida include comparing quotes from multiple providers, increasing the deductible, taking advantage of discounts, and dropping unnecessary coverage.