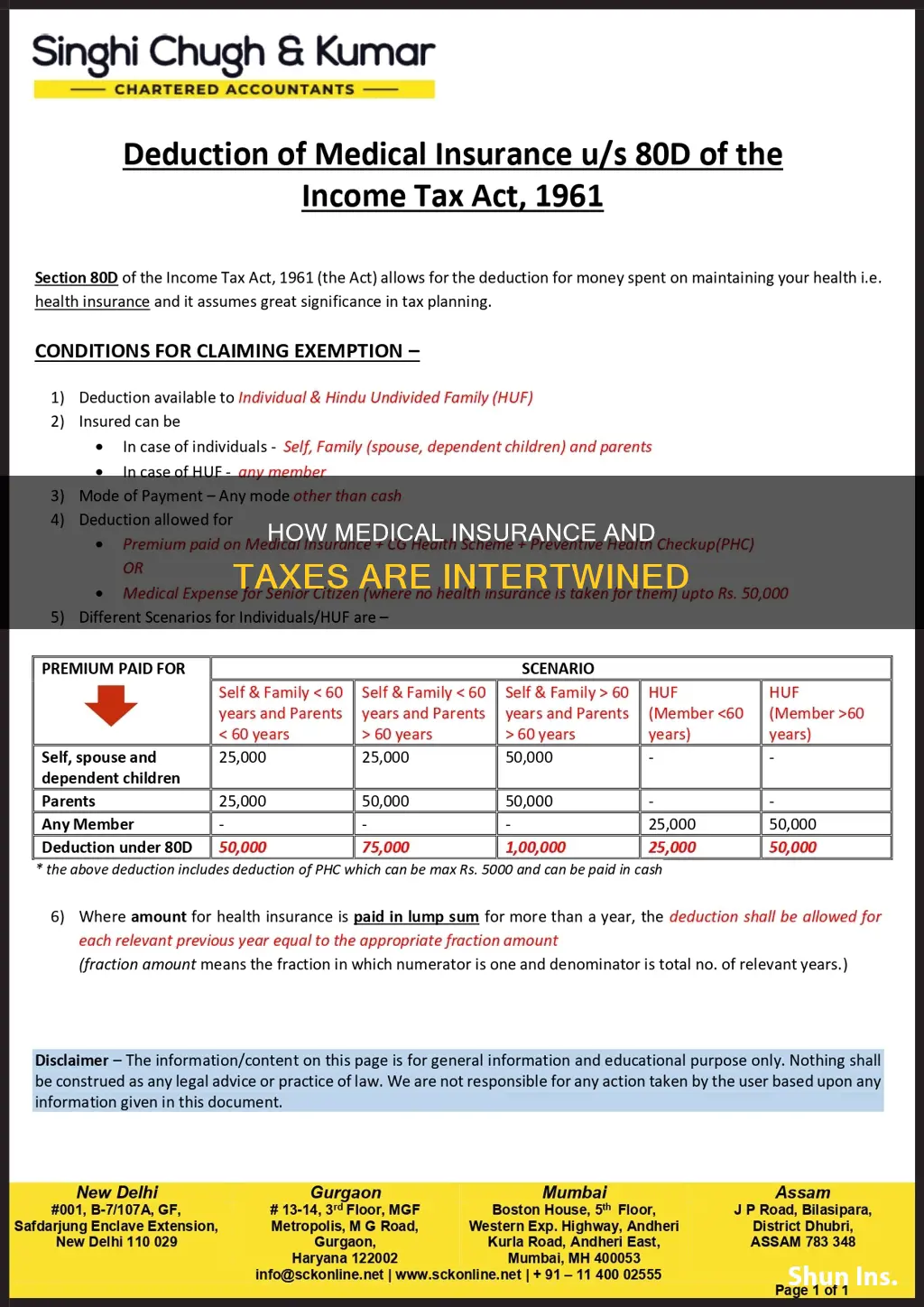

Whether an individual's medical insurance increases or decreases after taxes depends on a variety of factors, including the type of insurance plan, the source of the plan, and the individual's income. For example, if an individual is enrolled in an employer-sponsored health insurance plan, their premiums are typically deducted from their paycheck before income taxes or payroll taxes, resulting in lower tax liability. On the other hand, if an individual purchases insurance through the Health Insurance Marketplace and does not qualify for a premium tax credit, they may pay a higher price and have to file Form 8962 with their tax return. Additionally, self-employed individuals can claim deductions for themselves, their spouses, and their dependents, which can further impact their tax liability.

Characteristics and Values of Medical Insurance Premiums

| Characteristics | Values |

|---|---|

| Pre-tax medical premiums | Health insurance premiums deducted from your paycheck before your employer withholds income taxes or payroll taxes. |

| After-tax medical premiums | An option if an individual doesn’t want to participate in their employer's pre-tax plan or if their employer doesn’t offer a pre-tax plan. |

| Premium-only plan (POP) or a Section 125 cafeteria plan | Employer deducts insurance premium contributions from your payroll on a pre-tax basis. |

| Self-employed health insurance deduction | Available for the costs of medical insurance, dental insurance, and long-term care policies. |

| Premium tax credits | Help individuals and families with low to moderate incomes afford health insurance. |

| Tax deductions | Reduces taxable income and depends on the taxpayer's marginal tax rate, which rises with income. |

| Tax credits | Reduces the amount of tax you owe. |

Explore related products

What You'll Learn

![]()

Pre-tax medical premiums

To benefit from pre-tax medical premiums, you must be enrolled in your employer's health insurance plan. Employer-sponsored plans with qualifying pre-tax premiums include healthcare spending account contributions, such as health savings accounts (HSAs) and flexible spending accounts (FSAs). You can confirm if your health premiums are pre-tax by viewing your pay stub and looking for a column titled "Deductions" or something similar. If your health premium is listed in this column and your employer deducts it from your gross pay, it is a pre-tax premium.

It is important to note that pre-tax health insurance premiums may not always be deducted before certain taxes are withheld or contributed. For example, in some states, a pre-tax health premium may not be considered pre-tax for specific taxes, such as state unemployment tax.

By taking advantage of pre-tax medical premiums, employees can reduce their taxable income and save money on their health insurance costs. This benefit is particularly valuable for taxpayers in higher tax brackets.

Spousal Medical Insurance: Can You Cancel Post-Marriage?

You may want to see also

Explore related products

![]()

After-tax medical premiums

Individually purchased plans with qualifying after-tax premiums include major medical coverage, such as purchasing individual health insurance through the Health Insurance Marketplace, and supplemental/voluntary coverage, such as accident or disability insurance. One advantage of after-tax plans is that they can be dropped at any time, so they are a good option for those who anticipate dropping their coverage and enrolling in another plan during the year due to qualifying for a special enrollment period.

While different from pre-tax premiums, after-tax plans can still offer some savings. For example, premiums can be listed as an itemized deduction when filing income taxes for all medical expenses and premiums that exceed 7.5% of an individual's income. Additionally, most self-employed taxpayers can deduct health insurance premiums using Schedule 1 for Line 162 on Form 1040. Self-employed individuals with a net profit for the year may be eligible for the self-employed health insurance deduction, which is an adjustment to income rather than an itemized deduction.

Another option for individuals who want the benefits of both pre-tax and after-tax plans is a standalone HRA, such as a Qualified Small Employer HRA (QSEHRA) or Individual Coverage HRA (ICHRA). With this type of plan, individuals purchase an individual health insurance plan with their own money and then receive reimbursements from their employer for their monthly premiums and other eligible out-of-pocket medical expenses up to a set allowance amount. These reimbursements are made on a tax-free basis, providing the same tax benefits as a traditional pre-tax plan, while also allowing individuals to choose a plan that best suits their needs and take the plan with them if they leave their employer.

Switching Insurance: Medication Access and Denial

You may want to see also

Explore related products

$199.95 $245.95

![]()

Tax credits and deductions

The cost of health insurance can be reduced by enrolling in a premium-only plan (POP) or a Section 125 cafeteria plan, allowing your employer to deduct insurance premium contributions from your payroll on a pre-tax basis. This can save you up to 40% on income and payroll taxes for that portion. Pre-tax medical premiums are also excluded from federal income tax, Social Security tax, Medicare tax, and typically state and local income tax.

If you are self-employed and have a net profit for the year, you may be eligible for the self-employed health insurance deduction, which is an adjustment to income for premiums paid on a health insurance policy covering medical care for yourself, your spouse, and your dependents.

If you are enrolled in a Marketplace plan, you may be eligible for a premium tax credit (also known as PTC) to lower your monthly insurance payments. This is a refundable credit, and you must meet certain requirements and file a tax return with Form 8962, Premium Tax Credit (PTC).

Additionally, you may be able to deduct medical and dental expenses that you paid for yourself, your spouse, and your dependents during the taxable year, provided these expenses exceed 7.5% of your adjusted gross income for the year. Deductible medical expenses may include, but are not limited to, amounts paid to doctors, dentists, surgeons, inpatient hospital care, and prescription drugs.

Strategies to Negotiate Medical Bills When You Lack Insurance

You may want to see also

Explore related products

![]()

Self-employed health insurance

Self-employed individuals are responsible for securing their own health insurance coverage and paying for it. However, they can benefit from the self-employed health insurance deduction, which allows them to deduct the cost of health insurance from their taxable income. This deduction is available to independent contractors and other self-employed taxpayers who meet certain Internal Revenue Service (IRS) criteria.

To be eligible for the self-employed health insurance deduction, you must be self-employed, have a profitable business, and not have access to an employer-sponsored health plan. This includes plans sponsored by your spouse's employer or the employer of someone you work for. If you are eligible, you can deduct up to 100% of the health insurance premiums you paid during the year. This includes premiums for medical, dental, vision, and qualifying long-term care insurance for yourself, your spouse, your dependents, and any non-dependent children under 27 at the end of the tax year.

The self-employed health insurance deduction is an "above-the-line" deduction, which means you don't need to itemize your deductions to claim it. Instead, it is an adjustment to your income, reducing your adjusted gross income (AGI). This can be beneficial as it may help you qualify for other tax breaks. To claim the deduction, you can use Form 7206 to calculate the amount and then report it on Schedule 1 (Form 1040), line 17.

In addition to the self-employed health insurance deduction, there are other ways for self-employed individuals to reduce the cost of healthcare expenses. For example, self-employed workers can also take advantage of medical expense tax deductions, which are itemized deductions available to anyone, regardless of employment status. These deductions include various medical expenses not covered by insurance, such as out-of-pocket costs for treatments, visits to healthcare professionals, and transportation to medical appointments.

Understanding the End Date of Your Medical Insurance Coverage

You may want to see also

Explore related products

![]()

Employer-sponsored health insurance

The cost of health insurance can be affected by whether an individual's medical insurance premium is deducted pre-tax or after-tax. If you are enrolled in an employer-sponsored health insurance plan, you may be able to pay your premium with pre-tax money. This means that your employer deducts your health insurance premium from your paycheck before any income taxes or payroll taxes are withheld and then pays the insurance company on your behalf. This can save you up to 40% on income and payroll taxes.

Alternatively, if you do not want to participate in your employer's pre-tax plan or if your employer does not offer one, you may be able to deduct your medical premiums on an after-tax basis. In this case, any copays, prescription costs, and payments made before meeting your deductible are also considered after-tax medical expenses. Individually purchased plans with qualifying after-tax premiums include major medical coverage, such as purchasing individual health insurance through the Health Insurance Marketplace, and supplemental/voluntary coverage, such as accident or disability insurance.

It is important to note that the exclusion of premiums for employer-sponsored insurance (ESI) reduces taxable income, so it is worth more to taxpayers in higher tax brackets than to those in lower brackets. This exclusion lowers the after-tax cost of health insurance for most Americans and is the reason why most American families have health insurance coverage through their employers.

Using Medical Gap Insurance for Rent: Is It Possible?

You may want to see also

Frequently asked questions

A pre-tax medical premium is a health insurance premium that your employer deducts from your paycheck before any income taxes or payroll taxes are withheld and then pays to the insurance company on your behalf.

If your health insurance is pre-tax, your employer deducts it from your gross pay. You can confirm this by viewing your pay stub and looking for a column titled "Deductions" or something similar.

If your insurance is provided by your employer, you cannot deduct your health insurance premiums. If you pay for health insurance coverage after taxes are taken out of your paycheck, you might qualify for the medical expense deduction.

If you are enrolled in a Marketplace plan, you can use a premium tax credit to lower your monthly insurance payment. If you are self-employed, you can get a tax deduction for yourself, your spouse, and your dependents.