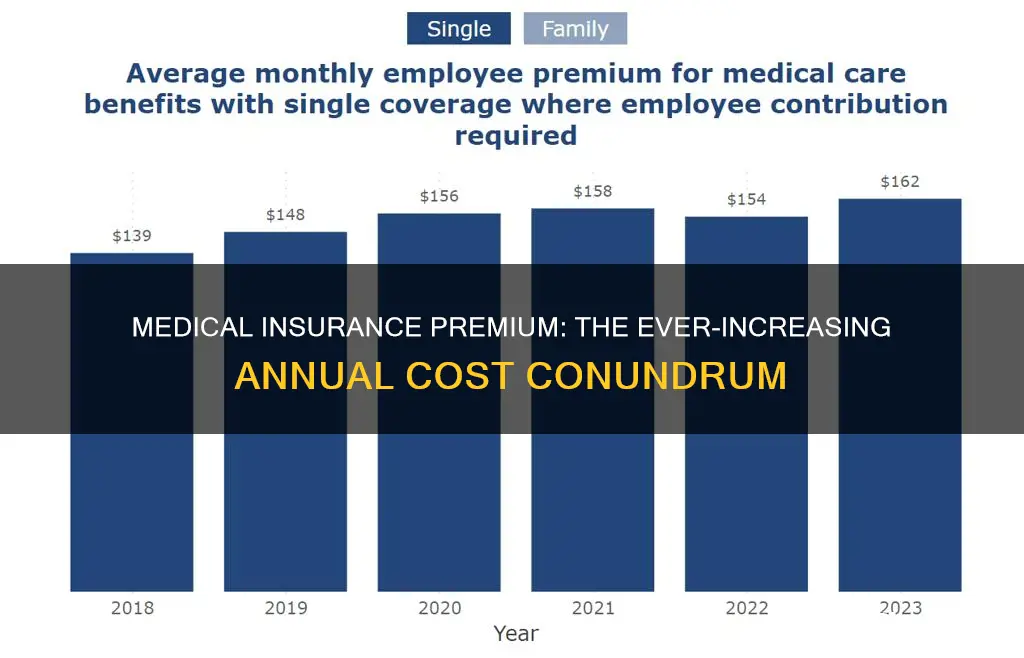

Health insurance premiums are a crucial yet expensive necessity, with 52% of policyholders experiencing a premium increase of over 25% in the past year. This begs the question: do medical insurance premiums increase every year? The answer is a qualified yes. While not all policyholders will experience an annual increase, premiums typically rise due to factors such as age, healthcare costs, medical inflation, and policy changes. As people age, their risk of requiring medical care increases, and healthcare costs and inflation are also on the rise. Policyholders can mitigate premium hikes by comparing plans, choosing higher deductibles, and reviewing coverage needs annually. Multi-year health insurance policies can also help to lock in rates and prevent annual increases.

| Characteristics | Values |

|---|---|

| Does medical insurance premium increase every year? | Yes and No. While the premium could increase every year, it is not guaranteed to increase for every policyholder every year. |

| Why does medical insurance premium increase? | Factors such as rising healthcare costs, medical inflation, aging policyholders, enhanced coverage, administrative expenses, and regulatory changes drive insurers to adjust premiums to cover higher anticipated costs. |

| Strategies to mitigate health insurance premium hikes | Comparing plans, choosing higher deductibles, participating in wellness programs, and reviewing coverage needs annually. |

| Multi-year health insurance policy | Opting for a multi-year health insurance policy can help counter rising premiums by securing the premium rate for the entire period, preventing annual hikes due to age or inflation. |

Explore related products

What You'll Learn

![]()

Medical inflation

There are several factors that contribute to medical inflation. One key factor is the adoption of advanced technologies and treatments. As medical advancements are made, the cost of healthcare services increases. This includes the development and use of new, more expensive technologies and treatments. For example, the adoption of AI tools and robotic surgeries has contributed to the rise in healthcare costs.

Another factor contributing to medical inflation is the rising demand for healthcare. As the population ages, the demand for healthcare increases, which drives up the cost of medical services and goods. This is particularly true in countries with an ageing population, such as India. The heavy reliance on imported medical equipment can also contribute to higher costs.

In addition to these factors, the high cost of living and inflation in healthcare can also contribute to medical inflation. As the cost of everyday amenities, such as groceries and fuel, increases, so does the cost of healthcare. This is because the production and distribution of medical goods and services are dependent on these everyday amenities.

The impact of medical inflation is significant. It affects not only the cost of health insurance premiums but also the financial well-being of individuals and families. In countries like India, where a large portion of the population pays for healthcare out of pocket, the rise in medical costs can be devastating. It can lead to delays in treatment, as well as financial hardship for families. This highlights the importance of investing in adequate health insurance coverage to protect against the financial risks associated with medical emergencies.

Aetna Medical Insurance: Eye Exam Coverage Explained

You may want to see also

Explore related products

![]()

Rising healthcare costs

Several factors contribute to rising healthcare costs. Firstly, medical advancements and new treatments can be expensive to develop and implement, driving up prices. Secondly, the increased demand for healthcare services due to ageing populations and the higher prevalence of chronic diseases also plays a role. As people age, their bodies become more susceptible to diseases and injuries, leading to a higher need for medical care.

Inflation is another critical factor in rising healthcare costs. Medical inflation refers to the annual increase in the cost of medical services and goods. This includes everything from hospital stays and surgeries to prescription medications. Inflation in the healthcare sector can be influenced by various factors, including labour costs, the price of medical supplies, and administrative expenses associated with managing insurance plans and processing claims.

The structure of the healthcare system also impacts costs. In the US, for example, private insurance companies often pay higher prices for healthcare services than public insurance programs like Medicare and Medicaid. This can drive up overall healthcare spending and influence insurance premiums. Additionally, regulatory changes and policy decisions can significantly affect healthcare costs. For instance, the Trump administration's proposed cuts to Medicaid and the elimination of tax subsidies for Obamacare plans are expected to make healthcare less affordable for many Americans.

Applying for Medical Insurance in California: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Ageing policyholders

Insurers perceive older policyholders as higher risks, and this increased risk of requiring medical care is reflected in higher premiums. Older people are more likely to need prescription drugs, and the increased frequency of claims leads to higher costs for insurance providers. The higher costs are then passed on to the consumer through higher premiums.

The impact of ageing on health insurance premiums underscores the importance of obtaining medical insurance at a younger age when premiums are more affordable. Early enrolment can make insurance more affordable and ensure comprehensive coverage when it is most needed. It is also advisable to purchase a health insurance policy with lifetime renewability.

To manage the costs of rising premiums, policyholders can employ various strategies. These include regularly reviewing and adjusting coverage, exploring different plans, and taking advantage of available programs. Policyholders can also lower their premiums by maintaining a healthy lifestyle. Many insurance companies offer discounts for policyholders who meet specific health criteria or participate in wellness programs.

Verify Your Medical Insurance Status: Quick and Easy Steps

You may want to see also

Explore related products

![]()

Enhanced coverage

Health insurance premiums typically increase annually due to several factors, including rising healthcare costs, medical inflation, ageing policyholders, and enhanced coverage. While the increase in premiums is often inevitable, there are strategies that policyholders can employ to mitigate the impact of these rising costs.

While enhanced coverage can provide valuable peace of mind and improved financial protection in the event of medical issues, it comes at a cost. Insurance companies will often pass on the higher costs associated with enhanced coverage to their customers in the form of increased premiums. This allows them to maintain profitability while continuing to provide the expanded range of benefits.

The impact of enhanced coverage on premiums can vary depending on the specific changes made to the policy. For example, the addition of a new benefit that is rarely utilised by policyholders may have a minimal impact on premiums, while an increase in the insured sum or coverage for expensive treatments could result in a more significant rise in costs. It's important for policyholders to carefully review the terms and conditions of their insurance policy to understand the specific enhancements and their corresponding impact on premium costs.

While enhanced coverage typically leads to higher premiums, it's worth noting that there are strategies to manage these costs. Policyholders can compare plans, choose higher deductibles, participate in wellness programs, and review their coverage needs annually to find a balance between comprehensive protection and affordable premiums. Additionally, opting for multi-year health insurance policies can lock in premium rates for extended periods, shielding individuals from annual hikes due to enhanced coverage or other factors.

Applying for State Medical Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Administrative expenses

Medical insurance premiums typically increase annually due to several factors, one of which is administrative expenses. Administrative expenses refer to the costs associated with managing and administering health insurance plans, including claims processing and customer service. These expenses are necessary for insurance companies to function effectively, but they can add up and impact the overall cost of premiums.

Insurance companies need to closely monitor their administrative expenses to ensure they have enough premium income to cover these costs. While administrative expenses do not directly factor into sales or production, they are typically covered by the premiums paid by policyholders. This means that any increase in administrative expenses for the insurance company may result in higher premiums for the policyholders.

The specific administrative expenses can vary and include employee benefits, security, and cleaning services. These costs are essential to the day-to-day operations of an insurance company, such as providing a safe and secure work environment for employees and maintaining a clean and professional space. However, they can also be influenced by factors beyond the company's control, such as inflation and market trends.

In some countries, administrative costs are included in risk-equalization, which aims to create a level playing field for insurers and prevent risk selection. This means that administrative costs are considered when determining insurance premiums to ensure that all insurers are operating on a similar cost structure. This approach is seen in countries like Germany and the US, where administrative costs are recognized as a significant component impacting insurance premiums.

Understanding Insurance Payback in Medical Malpractice Cases

You may want to see also

Frequently asked questions

Yes, medical insurance premiums typically increase annually.

There are several reasons for the increase in medical insurance premiums, including rising healthcare costs, medical inflation, aging policyholders, enhanced coverage, administrative expenses, and regulatory changes.

As policyholders age, their risk of requiring medical care typically increases. Insurers often adjust premiums to reflect this increased risk, which can result in higher premiums as policyholders get older.

Medical inflation refers to the annual increase in the cost of medical services and goods. This includes everything from hospital stays and surgeries to prescription medications. Insurers adjust their premiums to cover these higher costs, which contributes to the overall rise in health insurance premiums.

Yes, there are strategies to mitigate medical insurance premium hikes, including comparing plans, choosing higher deductibles, participating in wellness programs, and reviewing coverage needs annually. Additionally, opting for a multi-year health insurance policy can help lock in the premium rate and prevent annual hikes.