Medicare Supplement Insurance, also known as Medigap, is an extra insurance policy that can be purchased from private insurance companies to cover the costs that Original Medicare does not, such as deductibles, copays, and coinsurance. Medigap policies require the policyholder to pay a monthly premium, the amount of which varies based on factors such as age, gender, residential area, and smoking status. The monthly premium for Medigap policies can also differ between insurance companies offering the same plan. Therefore, it is important for individuals to compare the costs of different Medigap plans and consider their specific needs and circumstances when choosing a Medicare Supplement Insurance plan.

| Characteristics | Values |

|---|---|

| Monthly fee | Yes |

| Premium amount | Depends on the policy purchased, location, and other factors; varies each year |

| Out-of-pocket costs | Yes; can vary significantly depending on coverage and health needs |

| Medigap policy | Bought from private insurance companies; costs vary |

| Medicare Advantage Plan | Low upfront costs but high deductible |

Explore related products

$14.99

What You'll Learn

- Medicare Supplement Insurance (Medigap) is extra insurance to cover out-of-pocket costs

- Medigap policies are bought from private insurance companies

- Medigap plans are lettered A to N, with plans offering the same benefits for the same letter

- Medigap costs vary depending on the insurance company and personal circumstances

- The average monthly premium for a Medicare supplement policyholder was $217

![]()

Medicare Supplement Insurance (Medigap) is extra insurance to cover out-of-pocket costs

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from a private insurance company to cover out-of-pocket costs in Original Medicare (Parts A and B). Medigap policies help cover the costs of services that are already covered by Original Medicare, such as hospital and medical insurance. It's important to note that Medigap is not available to those who do not have Original Medicare.

There are 10 different types of Medigap plans offered in most states, labelled from A-D, F, G, and K-N. The benefits of each Medigap plan vary, and some plans include extra benefits like foreign travel emergency care. It is important to review the coverage of each plan and compare them side-by-side to find the one that best meets your needs. Additionally, not all plans are offered in every state, so it is essential to check the availability in your specific state.

The cost of a Medigap policy depends on the insurance company and the specific plan chosen. The premium amount is the main differentiating factor in the prices charged by different insurance companies for the same coverage. Therefore, it is crucial to compare plans with the same letter to ensure you are getting the best price. Some companies may offer discounts, such as those for women, non-smokers, or those who pay yearly, which can further impact the overall cost of the policy.

When purchasing a Medigap policy, it is important to be aware of potential illegal practices by insurance companies and protect yourself during the shopping process. There is a six-month "Medigap Open Enrollment" period, which begins the first month you have Medicare Part B and are 65 or older. During this time, you are guaranteed the right to buy any Medigap policy, regardless of pre-existing health conditions. After this period, purchasing a Medigap policy may become more difficult or expensive.

Understanding Private Medical Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Medigap policies are bought from private insurance companies

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from private health insurance companies. Medigap policies are designed to help pay for out-of-pocket costs that are not covered by Original Medicare, which includes Part A (Hospital Insurance) and Part B (Medical Insurance). These out-of-pocket costs can include deductibles, copays, and coinsurance.

Medigap policies are available in all 50 states and Washington, D.C., and they can vary in terms of premiums and enrollment eligibility. It is important to compare Medigap policies from different insurance companies, as the costs can vary significantly even though the benefits offered are standardized and remain the same across companies. The premium amount is typically the only difference between policies with the same plan letter sold by different companies.

When purchasing a Medigap policy, individuals will need to pay a monthly premium to the private insurance company, in addition to their monthly Medicare Part B premium. The insurance company will provide information on how to pay the monthly premium. Medigap policies are guaranteed renewable as long as the premium is paid, and they will continue to be automatically renewed each year.

Some Medigap plans may offer additional benefits, such as coverage for foreign travel emergency services or discounts for specific groups, such as women, non-smokers, or married individuals. These plans can help lower overall healthcare costs by providing coverage for services that Original Medicare does not cover. It is important to note that Medigap policies do not cover healthcare costs for spouses, and spouses must purchase separate Medigap policies.

Overall, Medigap policies purchased from private insurance companies provide valuable supplemental coverage for individuals enrolled in Original Medicare, helping to reduce out-of-pocket expenses and providing additional benefits for a more comprehensive healthcare insurance plan.

Employer Access: Self-Insured Companies and Your Medical Records

You may want to see also

Explore related products

![]()

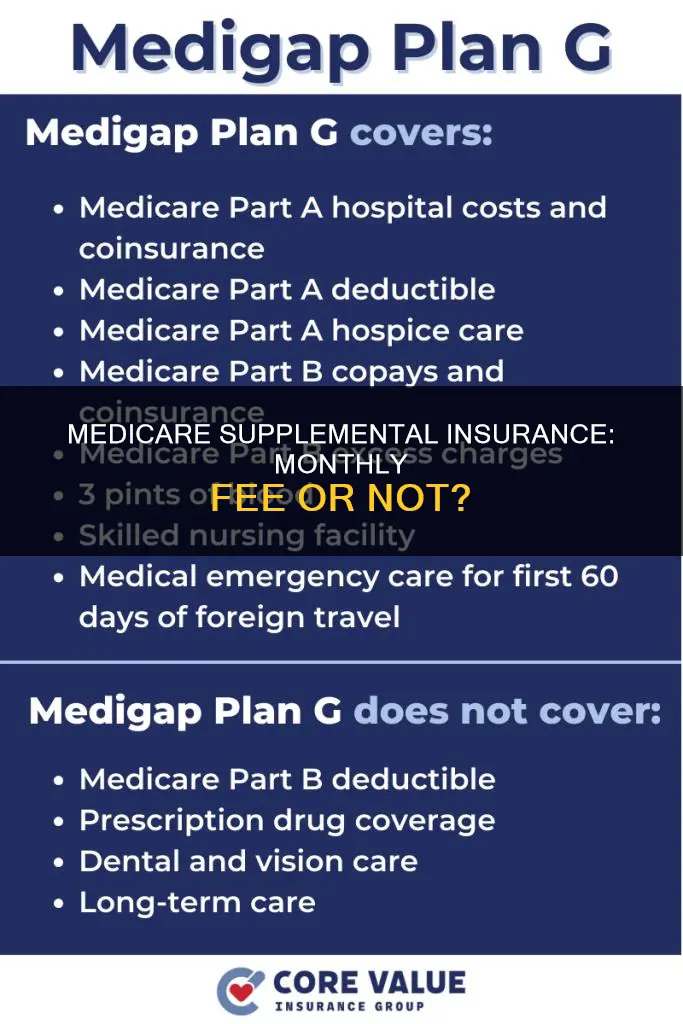

Medigap plans are lettered A to N, with plans offering the same benefits for the same letter

Medicare Supplement Insurance, also known as Medigap, is indeed subject to a monthly premium. The amount of this premium varies based on factors such as the chosen policy, location, and insurance company. Medigap policies are designed to help cover out-of-pocket expenses, such as deductibles, copays, and coinsurance, that are not covered by original Medicare (Parts A and B).

Medigap plans are lettered A to N, and each letter corresponds to a specific set of benefits. Regardless of the insurance company, plans with the same letter offer identical benefits. For example, Plan G from one company will provide the same benefits as Plan G from another company. The primary difference between Medigap plans with the same letter is the cost, which can vary significantly between insurance providers.

It is important to note that the availability of certain Medigap plans may depend on your state of residence and eligibility criteria. For instance, Plans C and F are unavailable for individuals who turned 65 on or after January 1, 2020, or for some people under the age of 65. Plans F and G offer a high-deductible option in certain states, while Plans K and L have specific out-of-pocket limits before fully covering approved services. Plan N, on the other hand, covers 100% of Part B service costs but does not include copayments for certain office and emergency room visits.

When considering a Medigap plan, it is advisable to compare plans with the same letter from different insurance companies to find the most cost-effective option. Insurance companies may offer discounts that can further influence the price of your Medigap policy. These discounts could include those for specific demographics, payment methods, or multiple policies.

Understanding Medical Bridge Insurance: Coverage Explained

You may want to see also

Explore related products

![]()

Medigap costs vary depending on the insurance company and personal circumstances

Medicare Supplement Insurance, also known as Medigap, is a supplemental coverage plan that helps with out-of-pocket costs for Medicare Parts A and B. Medigap policies are sold by private insurance companies, and the monthly premium you pay varies depending on the insurance company and your personal circumstances.

The benefits offered by each Medigap plan are standardised, meaning that the only difference between policies with the same plan letter sold by different companies is the premium amount. As such, it is important to compare Medigap plans with the same letter when shopping for a policy, as there can be significant variations in the premiums charged by different insurance companies for the same level of coverage.

The cost of a Medigap policy may depend on various factors, including the insurance company's discount policies and your enrolment status. For example, some companies offer discounts for women, non-smokers, married people, paying yearly, or using electronic funds transfer for premium payments. Additionally, if you are in your Medigap Open Enrollment Period or have a guaranteed issue right, you may be eligible for a lower premium.

Your personal circumstances, such as your age and health status, can also impact the cost of your Medigap policy. If you are under 65, your options for purchasing a Medigap plan may be limited, and switching from another health insurance plan to a Medigap plan may require passing a written health screening questionnaire. Therefore, it is essential to carefully review the rules and requirements of different insurance companies before making a decision.

In summary, when considering a Medigap policy, it is crucial to compare plans with the same letter from different insurance companies and be mindful of the potential impact of your personal circumstances on the cost of the policy. By carefully reviewing the available options and considering your individual needs, you can make an informed decision about purchasing Medicare Supplemental Insurance.

Inova Medical Group: Understanding Their Insurance Coverage

You may want to see also

Explore related products

![]()

The average monthly premium for a Medicare supplement policyholder was $217

Medicare Supplemental Insurance, also known as Medigap, is extra insurance you can buy from a private health insurance company to help pay your share of out-of-pocket costs in Original Medicare. Medigap plans are designated by the letters A–D, F, G, or K–N. Nearly 39% of policyholders chose Plan G, the most comprehensive plan for new beneficiaries in 2023. The average monthly premium among all Medicare supplement policyholders was $217.

The monthly premium for Medigap policies varies depending on the insurance company and the specific plan chosen. The premium amount is the only difference between policies with the same plan letter sold by different companies. There can be significant variations in the premiums charged by different insurance providers for identical coverage. For example, Medigap Plan M offers the same benefits and coverage regardless of the company, but the monthly cost can differ by $100 or more.

Several factors influence the cost of Medicare supplement insurance. Firstly, the type of Medigap plan chosen affects the price. Secondly, personal factors such as age, gender, residential area, and smoking status impact the premium. Additionally, the insurance company selected plays a role, as each carrier determines its own rates. Some companies offer discounts for certain groups, such as women, non-smokers, married individuals, or those who pay yearly or through electronic funds transfer.

It is important to note that Medicare supplement insurance costs can change yearly due to inflation. Therefore, it is advisable to research and compare the costs of Medigap plans in your area to make an informed decision. The timing of enrollment can also impact the monthly cost, with higher premiums for those who apply outside the Medigap open enrollment period.

Medical College of Georgia: Aetna Insurance Acceptance and Benefits

You may want to see also

Frequently asked questions

Yes, Medicare supplemental insurance, also known as Medigap, charges a monthly premium. The average monthly premium among all Medicare supplement policyholders was $217.

Medigap is extra insurance that covers the costs that Original Medicare doesn't, like deductibles, copays, and coinsurance.

Your insurance company will let you know how to pay for your monthly premium. You will also have to pay your monthly Medicare Part B premium.

The cost of your Medicare supplemental insurance depends on the type of Medigap plan you choose, your age, gender, residential area, and smoking status. The insurance company you choose also affects your costs, as each carrier determines its own rates.