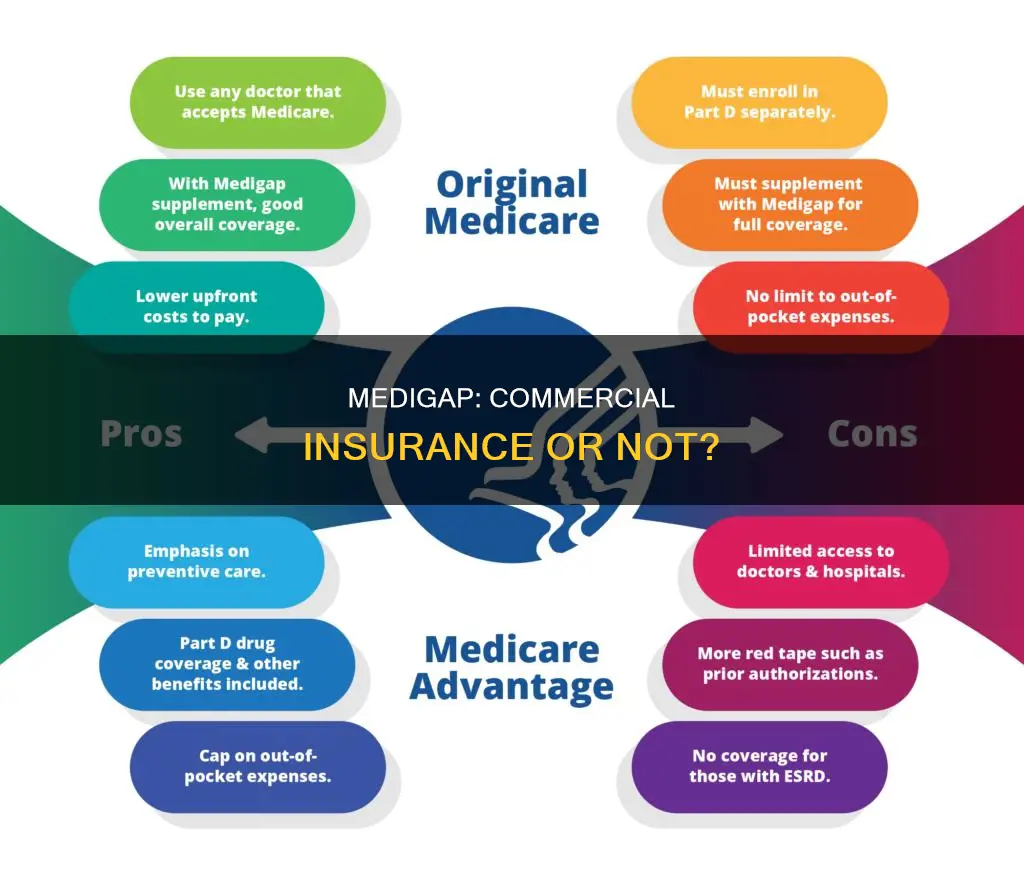

Medicare Supplement Insurance, commonly known as Medigap, is a type of commercial health insurance. It is extra insurance that can be purchased from a private health insurance company to help pay for out-of-pocket costs not covered by Original Medicare (Parts A and B). Medigap policies are designed to fill the gaps in Original Medicare coverage, and the insured must generally have Medicare Part A and Part B to be eligible for Medigap. Medigap plans are standardized and must follow federal and state laws, but costs can vary between different insurance companies. While Medigap provides supplemental coverage for individuals with Medicare Parts A and B, it does not cover spouses, who must purchase their own separate Medigap plans.

| Characteristics | Values |

|---|---|

| Type of Insurance | Commercial health insurance |

| Provider | Private insurance companies |

| Purpose | Fills "gaps" in Original Medicare Plan coverage |

| Eligibility | Must have Original Medicare – Part A and Part B |

| Coverage | Varies, but generally covers out-of-pocket costs not paid by Original Medicare |

| Cost | Varies by plan and insurance company |

| Renewal | Guaranteed renewable as long as premiums are paid |

| Spouse Coverage | Does not cover the spouse; they must purchase their own plan |

| Changes to Plans | New plans and changes to existing plans may be introduced, as seen in 2010 |

Explore related products

What You'll Learn

![]()

Medigap is a type of commercial insurance

Medigap, also known as Medicare Supplement Insurance, is a type of commercial insurance. It is extra insurance that helps pay for out-of-pocket costs that Original Medicare (Parts A and B) does not cover. Medigap policies are sold by private insurance companies and are designed to fill the gaps in Original Medicare coverage. Generally, you must have Original Medicare (Part A and Part B) to buy a Medigap policy, and you will need to pay premiums for both. Medigap policies must follow federal and state laws, and the front of the policy must clearly identify it as "Medicare Supplement Insurance".

Medigap plans are standardized and labelled with a letter, with each plan offering the same basic benefits regardless of the insurance company. The basic benefit structure for each plan is standardized by the federal government, but costs can vary between insurance companies. Medigap helps cover costs such as Part A coinsurance, hospital coverage beyond the limits of Medicare, Part A hospice/respite care coinsurance or copayment, and about 20% in out-of-pocket expenses not paid by Medicare Part B for doctor and outpatient medical expenses.

Medigap is different from Medicare Advantage (Part C), which replaces all basic government coverage with a private insurance plan. Medigap, on the other hand, supplements Parts A and B coverage and gives you more freedom of choice than Medicare Advantage. It is important to note that Medigap policies only cover the insured individual, so spouses must purchase separate policies.

Medigap is considered commercial insurance because it is provided by private insurance companies, as opposed to government-sponsored health insurance provided by federal agencies. Other common types of commercial health insurance include Preferred Provider Organization (PPO) plans and Health Maintenance Organization (HMO) plans, which are also offered by private issuers.

VA Insurance Money: Taxable Inheritance?

You may want to see also

Explore related products

![]()

Medigap policies are sold by private insurance companies

Medigap, also known as Medicare Supplement Insurance, is extra insurance that can be purchased from private health insurance companies. It helps pay for out-of-pocket costs that Original Medicare (Parts A and B) does not cover. Medigap policies are sold by private insurance companies, and they vary in cost and coverage. These policies are designed to fill the gaps in Original Medicare coverage, and the insured must generally have Original Medicare (Part A and Part B) to be eligible for a Medigap policy.

Medigap policies are standardized, meaning they must follow federal and state laws and provide the same basic benefits regardless of the insurance company. The main difference between Medigap policies offered by different companies is the cost. These policies help cover costs such as hospital stays, hospice care, and doctor visits, which can help individuals manage their medical expenses effectively.

Licensed insurance agents or brokers can sell Medigap plans to individuals with Medicare. It is important to note that Medicare does not send representatives to solicit business, and individuals should be cautious of anyone claiming to be a Medicare representative. To ensure the legitimacy of a Medigap plan, individuals can contact their state's department of insurance or visit their website to check the license status of the insurance agent.

Medigap policies are designed to provide supplemental coverage for individuals with Medicare Parts A and B. These policies can help pay for out-of-pocket expenses, such as deductibles, coinsurance, and copayments, associated with Medicare. The level of coverage chosen will determine how much of these expenses Medigap will cover. It is important to compare Medigap policies from different insurance companies to find the one that best suits an individual's needs and financial situation.

Medigap policies are considered commercial health insurance, which is provided by private companies rather than the government. Commercial health insurance plans are typically structured as Preferred Provider Organizations (PPOs) or Health Maintenance Organizations (HMOs). Medigap, therefore, falls under the category of commercial health insurance as it is sold by private insurance companies and provides supplemental coverage to individuals with Medicare.

Insurance Default: What Are the Consequences?

You may want to see also

Explore related products

![]()

Medigap policies help cover out-of-pocket costs

Medigap, also known as Medicare Supplement Insurance, is extra insurance that helps cover out-of-pocket costs that Original Medicare (Parts A and B) does not. Medigap policies are sold by private insurance companies and are designed to fill in the "gaps" in coverage that Original Medicare may not cover. These policies can help cover the costs of copayments, coinsurance, and deductibles that individuals would typically pay out-of-pocket.

To purchase a Medigap policy, one must generally already have Original Medicare (Part A and Part B). Additionally, individuals must buy separate Medigap policies for themselves; a Medigap policy will not cover any healthcare costs for a spouse. It is important to compare Medigap policies, as costs can vary, and different plans offer different levels of coverage.

Once an individual has selected their Medigap plan, they should review the details to understand their specific out-of-pocket maximum. This figure acts as a cap on annual expenses for covered services. By focusing on the out-of-pocket maximum cost, individuals can gain a clearer understanding of their potential financial exposure and make more informed decisions based on their healthcare needs and budget preferences.

The "Birthday Rule" is an important feature of Medigap. It allows individuals who already have Medigap insurance to have 60 days of "open enrollment" following their birthday each year to purchase a new Medigap policy without a medical screening or a new waiting period. This flexibility enables individuals to adjust their coverage as their healthcare needs and financial circumstances change.

In summary, Medigap policies are designed to help cover out-of-pocket costs associated with Original Medicare. They are sold by private insurance companies and can vary in terms of cost and coverage. By understanding the out-of-pocket maximums and utilizing the "Birthday Rule," individuals can make informed decisions about their healthcare coverage and ensure they have adequate protection against unexpected medical expenses.

Understanding Prepaid Insurance Adjusting Entries: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Medigap policies must follow federal and state laws

Medigap, or Medicare Supplement Insurance, is extra insurance that can be purchased from a private health insurance company to help pay out-of-pocket costs in Original Medicare. Medigap policies are designed to pay some of the health care costs that the Original Medicare Plan does not cover.

Federal Laws

- The Omnibus Budget Reconciliation Act of 1990 mandated the standardization of Medigap policies across the United States.

- The federal Medicare Improvements for Patients and Providers Act of 2008 required states to adopt changes to Medigap insurance policies, which took effect on June 1, 2010.

- The Health Insurance Portability and Accountability Act (HIPAA) restricts insurance companies from imposing pre-existing condition exclusions.

- The Balanced Budget Act provisions apply only to Medicare beneficiaries aged 65 or older.

- All newly entitled Medicare beneficiaries aged 65 or older have the right to a guaranteed issue of any Medigap policy offered for sale for six months after their Medicare entitlement begins.

State Laws

- State laws vary, but some states require insurance companies to sell designated Medigap policies to Medicare beneficiaries with disabilities. For example, Connecticut requires insurance companies to offer Plans A, B, and C to Medicare beneficiaries with disabilities if they offer these plans to older Medicare beneficiaries.

- State laws also dictate whether insurance companies may refuse to renew a Medigap policy purchased before 1992.

Documenting Insurance Audit Adjustments: A Step-by-Step Guide to Recording Payments

You may want to see also

Explore related products

![]()

Medigap policies are guaranteed renewable

Medigap, also known as Medicare Supplement Insurance, is extra insurance that can be purchased from a private health insurance company. It helps to pay for out-of-pocket costs that Original Medicare (Parts A and B) does not cover. Medigap policies are guaranteed renewable, meaning that they are automatically renewed each year as long as the individual continues to pay their premium. This ensures continuous coverage year after year.

However, there are certain situations in which a Medigap policy may not be renewable. If an individual fails to pay their premium, provides untrue information on their plan application, or if the insurance company goes out of business, their Medigap policy may not be renewed. Additionally, insurance companies may refuse to renew policies purchased before 1992, but this requires the state's approval.

It is important to note that Medigap policies are standardized, meaning that all plans with the same letter offer the same benefits, regardless of the insurer. While costs may vary between insurance companies, the benefits provided remain consistent. This standardization ensures that individuals can make informed decisions when choosing a Medigap policy that best suits their needs.

The Medigap Open Enrollment Period is a critical window for individuals interested in purchasing a Medigap policy. This six-month period begins in the first month an individual has Medicare Part B and is 65 years of age or under. During this time, individuals have the flexibility to choose any Medigap policy available in their state, even if they have health issues. After this open enrollment period ends, purchasing a Medigap policy may become more challenging, and insurers may deny coverage based on pre-existing conditions.

In summary, Medigap policies are guaranteed renewable as long as individuals fulfil their obligation to pay premiums and abide by the terms of their plan. This renewable nature of Medigap provides individuals with peace of mind, knowing that their coverage will continue without interruption as long as they meet their responsibilities.

Unraveling the Path to Becoming an Insurance Adjuster in Malaysia

You may want to see also

Frequently asked questions

Medicare Supplement Insurance, or Medigap, is extra insurance that can be purchased from a private health insurance company to help pay for out-of-pocket costs in Original Medicare.

Yes, Medigap is considered commercial insurance as it is provided by private companies rather than the government.

Anyone enrolled in Medicare Parts A and B can purchase a Medigap plan.

Medigap plans help pay for costs that Medicare doesn't cover, such as out-of-pocket expenses, deductibles, coinsurance, and extended hospital stays.

Medigap plans are standardized and must provide the same benefits, so it's important to compare costs and choose a plan that suits your needs and financial situation.