Mortgage insurance is an added expense to consider when taking out a mortgage with a down payment of less than 20%. It is designed to protect the lender in the event that the borrower defaults on their loan. Typically, borrowers making a down payment of less than 20% of the purchase price of the home are required to pay for mortgage insurance, which can be included in the monthly mortgage payment. This insurance does not reduce the principal amount of the loan but helps borrowers qualify for a loan that they might not otherwise be able to get.

| Characteristics | Values |

|---|---|

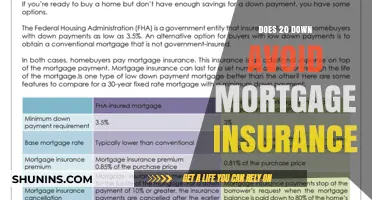

| Who does mortgage insurance protect? | The lender |

| Who needs mortgage insurance? | Those who take out a Federal Housing Administration (FHA) loan or put down less than 20% on a conventional loan. |

| What does mortgage insurance cost? | The cost varies depending on the loan amount, loan-to-value ratio (LTV), and credit score. It can be paid monthly, upfront, or rolled into the mortgage. |

| Can you get rid of mortgage insurance? | Yes, once you've paid off 20% of your loan or reached 20% equity in your home. |

| Does mortgage insurance add towards the principal? | No, mortgage insurance is an added expense on top of the principal. |

Explore related products

What You'll Learn

![]()

Mortgage insurance is paid monthly

Mortgage insurance is typically paid monthly and included in the total monthly payment made to the lender. The insurance lowers the risk to the lender of making a loan to the borrower, thereby allowing borrowers to qualify for a loan they might not otherwise be able to get. This insurance protects the lender in the event that the borrower falls behind on their payments.

There are several types of mortgage insurance, including private mortgage insurance (PMI), Federal Housing Administration (FHA) insurance, and U.S. Department of Agriculture (USDA) insurance. PMI rates vary by down payment amount and credit score but are generally paid monthly with little or no initial payment required at closing. FHA insurance includes both an upfront cost paid at closing and a monthly cost included in the borrower's monthly payment. USDA loans have an upfront guarantee fee and an annual fee that is divided into monthly installments and included in the mortgage payment.

It's important to note that mortgage insurance increases the overall cost of the loan. Additionally, it does not protect the borrower but rather ensures that the lender receives the full amount owed in the event of foreclosure. Borrowers can explore alternatives to mortgage insurance, such as piggyback" second mortgages or Department of Veterans' Affairs (VA)-backed loans, which do not require monthly mortgage insurance premiums.

While mortgage insurance is typically paid monthly, there are options for borrowers who prefer a different payment structure. For example, with lender-paid mortgage insurance (LPMI), the lender covers the premium, but the borrower pays a higher interest rate on the mortgage. Split-premium mortgage insurance allows borrowers to pay a portion upfront at closing and the remaining balance in monthly installments.

Corgi Pet Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

It protects the lender, not the borrower

Mortgage insurance is an added expense that homebuyers need to consider when taking out a mortgage with a down payment of less than 20%conventional loans with a down payment of less than 20% and is paid to the lender as a monthly premium alongside the mortgage principal and interest payment. The cost of mortgage insurance depends on the loan amount, loan-to-value ratio (LTV), and credit score, but it can add hundreds of dollars to the monthly bill.

Mortgage insurance does not add towards the principal. The principal refers to the original sum of money borrowed to purchase a home. Instead, mortgage insurance protects the lender in the event that the borrower falls behind on their payments. If the borrower defaults on their loan, the insurance pays the lender a portion of the principal. However, the borrower is still responsible for the loan and may lose their home through foreclosure if they fall too far behind.

Mortgage insurance is not always necessary. For example, if a homebuyer can make a down payment of at least 20%, they may not be required to pay for mortgage insurance. Additionally, once the borrower has accumulated 20% equity by paying down their mortgage, they may be able to request to have the mortgage insurance removed. This can lower their monthly mortgage payment by saving them money each month.

It is important to note that mortgage insurance should not be confused with mortgage life insurance or mortgage disability insurance. While mortgage insurance protects the lender, mortgage life insurance pays off the remaining mortgage if the borrower dies, and mortgage disability insurance covers the mortgage payments for a certain period if the borrower becomes disabled. Overall, while mortgage insurance does not add towards the principal, it can help homebuyers qualify for a loan with a lower down payment and competitive interest rates.

VSP Eye Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

It's required for conventional loans with 20% down payment

Private mortgage insurance (PMI) is typically required for conventional loans with a down payment of less than 20%. It is an added cost to your monthly mortgage payment. The exact amount varies depending on your loan amount, loan-to-value ratio (LTV), and credit score, but it can add hundreds of dollars to your monthly bill.

Mortgage insurance lowers the risk to the lender of making a loan to you, so you can qualify for a loan that you might not otherwise be able to get. Typically, borrowers making a down payment of less than 20% of the purchase price of the home need to pay for mortgage insurance. It increases the cost of your loan and is included in your total monthly payment to your lender, your costs at closing, or both. Mortgage insurance, no matter what kind, protects the lender – not you – in the event that you fall behind on your payments.

If you get a conventional loan, your lender could arrange for mortgage insurance with a private company. Private mortgage insurance (PMI) rates vary by down payment amount and credit score but are generally cheaper than FHA rates for borrowers with good credit. Most PMI is paid monthly, with little or no initial payment required at closing.

If you get a Federal Housing Administration (FHA) loan, your mortgage insurance premiums are paid to the FHA. FHA mortgage insurance is required for all FHA loans. It costs the same no matter your credit score, with only a slight increase in price for down payments less than five percent. FHA mortgage insurance includes both an upfront cost, paid as part of your closing costs, and a monthly cost, included in your monthly payment.

Progressive Insurance Benefits: Are They Worth the Hype?

You may want to see also

Explore related products

![Total Permanent Disability Benefits in Relation to Life Insurance / Principal Contributor, Arthur Hunter ; Associate Contributor, Mervyn Davis 1920 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

![]()

It can be removed once 20% equity is reached

Mortgage insurance is an added expense that you may need to consider when taking out a mortgage with a down payment of less than 20%. It is typically required for conventional loans with a down payment of less than 20% and helps buyers put down smaller down payments by providing added reassurance for the lender. The insurance protects the lender against the risk of the borrower defaulting on their loan. By paying mortgage insurance, buyers can qualify for a loan that they might not otherwise be able to get.

Private mortgage insurance (PMI) is the most common type of mortgage insurance for conventional loans. The cost of PMI depends on the loan amount, loan-to-value ratio (LTV), and credit score, but it can add hundreds of dollars to the monthly bill. It is usually paid monthly, alongside the mortgage principal and interest payments.

Mortgage insurance can be removed once 20% equity is reached. This can be achieved by paying down the mortgage or through an increase in the home's value. If you believe rising home values have put you over the 20% equity mark, you can contact your lender to request a review of your loan to determine if you qualify to have PMI removed. To remove PMI, you will need to ask your lender in writing to waive it and provide an appraisal of your home's value.

There are alternative options to remove PMI without reaching 20% equity. These include choosing a single premium PMI, which allows you to make a single payment to remove PMI from a conventional mortgage, or opting for lender-paid PMI, where the lender covers the PMI in exchange for a higher interest rate. Additionally, some lenders may offer a "piggyback" second mortgage as an alternative to mortgage insurance.

Mini Insured Warranty: Is It a Smart Investment?

You may want to see also

Explore related products

![NMLS Study Guide 2024-2025: 5 Full-Length MLO Practice Exams, SAFE Mortgage Loan Originator Test Prep Secrets Book with Detailed Answer Explanations: [3rd Edition]](https://m.media-amazon.com/images/I/61zi0BJms+L._AC_UL320_.jpg)

![]()

It's different from mortgage life insurance

Mortgage insurance is not the same as mortgage life insurance. Mortgage insurance is a type of insurance that helps homebuyers qualify for a loan with a lower down payment. It protects the lender in the event that the borrower falls behind on their payments. The cost of mortgage insurance is included in the borrower's monthly payments, and it can be required on specific types of loans, such as Federal Housing Administration (FHA) and U.S. Department of Agriculture (USDA) loans.

On the other hand, mortgage life insurance is a form of life insurance designed to pay off the policyholder's mortgage in the event of their death. It is a way to ensure that the policyholder's loved ones are not burdened with mortgage debt. The payout from mortgage life insurance decreases over time, meaning that the longer the policy is in effect, the lower the payout will be. This is in contrast to traditional life insurance, where the payout remains level throughout the policy term.

Mortgage protection insurance can also refer to a type of payment protection insurance (PPI). In this case, it insures monthly mortgage costs if the policyholder is unable to work due to accident, sickness, or unemployment. This type of insurance is typically only valid for a maximum of 12 to 24 months.

While both mortgage insurance and mortgage life insurance are related to homeownership, they serve different purposes. Mortgage insurance is designed to protect the lender, while mortgage life insurance provides financial protection for the policyholder's beneficiaries. Additionally, mortgage insurance is typically required for certain types of loans, whereas mortgage life insurance is optional and depends on the individual's financial goals and qualifications for coverage.

In summary, mortgage insurance and mortgage life insurance are distinct types of insurance with different objectives. Mortgage insurance helps homebuyers qualify for loans and protects lenders, while mortgage life insurance provides financial security for loved ones by paying off the policyholder's mortgage in the event of their death.

Insuring Your Home: A Guide

You may want to see also

Frequently asked questions

Mortgage insurance is a type of insurance that helps homebuyers get affordable, competitive rates and qualify for a loan with a lower down payment. It protects the lender in the event that the borrower falls behind on their payments.

Mortgage insurance is usually paid as a monthly premium alongside the mortgage principal and interest payment. The cost of mortgage insurance depends on the loan amount, loan-to-value ratio (LTV), and credit score. It can add up to about 1-2% of the loan amount but can sometimes be as high as 6%.

No, mortgage insurance does not add towards the principal. The principal refers to the original sum of money borrowed to purchase a home. Mortgage insurance is an additional cost that is paid to protect the lender in case the borrower defaults on their loan.