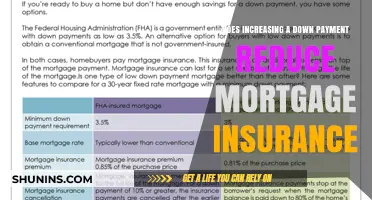

Private mortgage insurance (PMI) is an added expense for borrowers who take out a conventional mortgage with a down payment of less than 20%. It is calculated as a percentage of the mortgage loan amount and is recalculated each year. As you pay off your loan, your PMI cost will decrease. However, FHA mortgage insurance rates do not go down each year, but your MIP insurance payments do as your mortgage balance decreases.

| Characteristics | Values |

|---|---|

| Annual mortgage insurance cost | Calculated based on the first year's mortgage balance |

| Annual cost | Goes down each year as the loan balance is reduced |

| Mortgage insurance calculation | Calculated as a percentage of the mortgage loan amount |

| Mortgage insurance calculation | Not based on the home's appraised value or purchase price |

| FHA mortgage insurance rates | Do not go down each year |

| FHA MIP | Lasts 11 years or the life of the loan |

| MIP cancellation | Possible after 11 years if the original down payment was at least 10% of the purchase price |

| PMI removal | Possible once the mortgage-to-value ratio reaches 78% or 80% of the home's purchase price |

| PMI removal | Possible after reaching 20% equity in the home |

Explore related products

What You'll Learn

- Mortgage insurance rates vary depending on the type of loan

- FHA loans require mortgage insurance regardless of down payment size

- Private mortgage insurance (PMI) is required for conventional loans with less than 20% down payment

- Mortgage insurance rates are recalculated annually

- You can refinance to remove PMI or MIP once you have 20% equity

![]()

Mortgage insurance rates vary depending on the type of loan

PMI rates can vary a lot by borrower but typically range from 0.5% to 1.5% of the loan amount per year, paid in monthly instalments. You can request to cancel PMI when you reach 20% equity in your home. The Homeowners Protection Act of 1998 (HPA) mandates that mortgage lenders or servicers automatically cancel PMI when the mortgage's loan-to-value (LTV) ratio reaches 78% of the home's purchase price, or the month after the midpoint of the loan term is reached (e.g. after 15 years on a 30-year loan).

Mortgage insurance works differently for government-backed loans such as USDA and FHA mortgages. FHA loans require mortgage insurance premium (MIP) regardless of the down payment size. MIP charges two separate fees: an upfront payment of 1.75% of the loan amount, and an annual payment of 0.55% of the loan amount, paid in 12 instalments. If you put down at least 10% of the purchase price, you can remove MIP after 11 years.

USDA loans have an upfront mortgage insurance rate of 1% of the loan amount and an annual rate of 0.35%. VA loans have an upfront rate of between 0.5% and 3.6%, depending on the borrower and loan purpose.

Collision Centers: Insurance Reporting and Your Rights

You may want to see also

Explore related products

![]()

FHA loans require mortgage insurance regardless of down payment size

FHA loans, backed by the Federal Housing Administration, require mortgage insurance regardless of the down payment size. This type of insurance is known as mortgage insurance premium or MIP. MIP charges two separate fees: an upfront payment and an annual one. The upfront mortgage insurance premium (UFMIP) costs 1.75% of the loan amount, which can be paid at closing or rolled into the loan balance. The annual mortgage insurance premium (MIP) costs 0.55% of the loan amount per year, split into 12 installments and paid monthly with the mortgage payment. This annual premium may need to be paid for the life of the loan unless the borrower puts down at least 10%.

While the FHA mortgage insurance rate does not decrease each year, the dollar amount you pay for mortgage insurance does decrease as your mortgage balance decreases. Additionally, if you put down at least 10% of the purchase price, you can remove MIP after 11 years. However, if your down payment was less than 10%, you must pay MIP for the life of the loan unless you refinance.

FHA loans are a good option for homebuyers who have not saved much for their down payments. Mortgage insurance allows borrowers to buy a home with a smaller down payment and more lenient credit requirements. Without mortgage insurance, lenders would likely require a much larger down payment for borrowers to qualify for a mortgage.

Farmers Insurance and Windshield Replacement: What You Need to Know

You may want to see also

Explore related products

![]()

Private mortgage insurance (PMI) is required for conventional loans with less than 20% down payment

Private mortgage insurance (PMI) is a type of insurance that you may be required to purchase if you take out a conventional loan with a down payment of less than 20% of the purchase price. PMI protects the lender if you default on your mortgage payments. It is important to note that PMI does not protect the borrower—if you fall behind on your mortgage payments, you can still lose your home through foreclosure.

The cost of PMI varies depending on the loan type and size. It is calculated as a percentage of the mortgage loan amount, typically ranging from 0.5% to 1.5% of the loan amount per year, paid in monthly instalments. For example, if you have a $200,000 loan, and your annual mortgage insurance is 1.0%, you would pay $2,000 for mortgage insurance in the first year. As you pay off your loan, your PMI cost will decrease each year.

There are ways to avoid paying PMI on a conventional loan. One option is to take out a piggyback loan, where you make a down payment of around 10% and use a second mortgage to pay the remaining 10% of the 20% down payment. Another option is to look for lenders who offer conventional loans with smaller down payments that do not require PMI, although these loans typically come with higher interest rates.

If you are already paying PMI on a conventional loan, you can request to cancel it once you have reached 20% equity in your home. To be eligible for cancellation, you must be current on your mortgage payments, and an appraisal must verify the current property value. If you do not request cancellation, PMI will automatically be cancelled once you reach 22% equity.

Statutory Reporting: Insurance's Financial Reporting Requirements

You may want to see also

Explore related products

![]()

Mortgage insurance rates are recalculated annually

The rate of mortgage insurance also depends on the type of loan. Conventional loans and government-backed loans have different rules regarding mortgage insurance. Conventional loans require private mortgage insurance (PMI) if the down payment is less than 20%. The PMI rate depends on your credit score and can range from 0.5% to 1.5% of the loan amount per year. Government-backed loans, such as USDA and FHA mortgages, have pre-set mortgage insurance rates that are the same for every customer. For example, FHA loans have an upfront rate of 1.75% and an annual rate of 0.85%.

It's important to note that while FHA mortgage insurance rates do not decrease annually, your insurance payments will decrease as your mortgage balance decreases. Additionally, FHA mortgage insurance can be removed after 11 years if your original down payment was at least 10%. One way to remove FHA mortgage insurance is to refinance into a conventional loan or a different type of government-backed loan.

Home Insurance: Death and Policy Termination

You may want to see also

Explore related products

![]()

You can refinance to remove PMI or MIP once you have 20% equity

Mortgage insurance premiums (MIP) are usually associated with FHA loans and are required for all borrowers, regardless of their down payment. Private mortgage insurance (PMI), on the other hand, is for conventional loans with less than 20% down payment.

MIP and PMI can be removed once you have 20% equity in your home. You can request your lender to cancel your PMI once you reach this threshold. However, for FHA loans, refinancing into a conventional loan is usually the best way to remove MIP.

When you refinance, you take out a new loan to pay off your existing FHA loan. If you have at least 20% equity, you can refinance into a conventional loan without any mortgage insurance required. This option is available to those who have made all their mortgage payments on time and have a good payment history over the previous 12 months.

Refinancing your mortgage can also provide other benefits, such as changing terms, lowering your interest rate, and reducing monthly payments. It can also help you consolidate a second mortgage or other high-interest debt at a lower rate and/or longer term.

It is important to note that FHA loans originated before June 3, 2013, may qualify for MIP removal when the loan balance reaches 78% of the loan-to-value (LTV) ratio. For newer loans, refinancing into a conventional loan with no PMI is necessary once you have 20% equity.

Personal Liability Insurance: Necessary Protection or Wasteful Expense?

You may want to see also

Frequently asked questions

Mortgage insurance rates vary depending on the type of loan and the lender. For conventional loans, Private Mortgage Insurance (PMI) is required if the down payment is less than 20%. PMI rates are recalculated each year, so the cost goes down as you pay off the loan. For government-backed loans, such as FHA, VA, or USDA mortgages, the insurance rate is pre-set and may not decrease annually, but the dollar amount you pay for insurance decreases as your mortgage balance decreases.

Mortgage insurance is typically required if you buy or refinance a home with a down payment of less than 20%. It protects the lender in case you default on your loan.

The cost of mortgage insurance depends on the loan type, loan amount, and your credit score. For conventional loans, PMI rates can range from 0.5% to 1.5% of the loan amount per year. For government-backed loans, the upfront and annual insurance rates are pre-set and may vary depending on the loan program.

Yes, you can remove mortgage insurance once you have built up enough equity in your home. For conventional loans, you can request to cancel PMI when you reach 20% equity. For FHA loans, you can remove Mortgage Insurance Premium (MIP) after 11 years if your original down payment was at least 10%.

You can avoid paying mortgage insurance by making a down payment of 20% or more when buying a home. However, this may not be feasible for everyone, as it requires a large sum of cash upfront. An alternative option is to refinance into a conventional loan without PMI once you have built sufficient equity.