Insurance is a means of protection from financial loss, and it comes in many forms, from health and life insurance to automobile and property insurance. It is a legal contract between the insurance company (the insurer) and the person or entity being insured (the insured). While insurance can provide peace of mind, it is important to understand that not all losses or services are covered by insurance policies. Exclusions and conditions may apply, and claims can be denied. Understanding the specifics of one's insurance policy is essential to knowing what is and isn't covered and how to appeal when something is not covered.

| Characteristics | Values |

|---|---|

| Insurance policies | Legal contracts between the insurance company and the insured |

| Insuring agreements | Named-perils coverage; All-risk coverage |

| Insurance coverage | May not cover everything; may need to pay full cost yourself |

| Insurance claims | May be denied |

| Insurance endorsements | Must be explained in writing before the effective date of the new or renewed policy |

| Insurance and privacy | You have the right to prevent an insurance company from disclosing your personal financial information |

| Insurance and foreign policy | OFAC reviews insurance policies to ensure they do not undermine US foreign policy goals |

Explore related products

What You'll Learn

- Consumer rights: you have the right to sue, privacy, and to opt-out of data sharing

- Insurance types: health, auto, life, liability, and home insurance all have different exclusions

- Policy conditions: insurers can deny claims if policy conditions are not met, e.g. failing to protect property

- Pre-existing conditions: the Affordable Care Act removed exclusions, but not for all plans

- OFAC compliance: OFAC reviews global insurance policies to ensure they don't undermine US foreign policy

![]()

Consumer rights: you have the right to sue, privacy, and to opt-out of data sharing

Consumers have a variety of rights that they can exercise when interacting with insurance companies, including the right to sue, privacy rights, and the right to opt out of data sharing.

Right to Sue

Consumers can sue their insurance company for denying their claim or other misconduct. Each state has statutes and case law regulating the insurance industry, including the types of lawsuits consumers can bring against an insurer. An insurance policy is a type of contract, and every state allows for breach of contract actions. Consumers can also pursue a bad faith tort lawsuit in many states. Additionally, consumers may be able to sue under their state's unfair trade practices laws. It is important to note that insurance law can be complex, time-consuming, and expensive, so it is recommended to consult with an experienced insurance attorney before taking legal action.

Privacy Rights

Privacy laws, such as the California Consumer Privacy Act (CCPA), give consumers the right to control their personal information and how it is used by businesses. Consumers can request that businesses disclose what personal information they have collected, delete their personal information, and direct businesses not to sell or share their personal information. Insurance companies are exempted from certain privacy laws, but they are still required to provide consumers with notices regarding their data practices and the opportunity to opt out of certain data sharing.

Right to Opt Out of Data Sharing

Consumers have the right to opt out of having their data sold or shared by businesses. The CCPA requires businesses that sell or share personal information to offer two or more methods for consumers to submit requests to opt out, such as a user-enabled global privacy control or a "stop selling or sharing my data switch" in internet browsers. Insurance companies are subject to privacy laws and must provide consumers with the opportunity to opt out of non-affiliate marketing disclosures and affiliate sharing in some instances.

Medical Insurance: A Necessary Safety Net for All?

You may want to see also

Explore related products

![]()

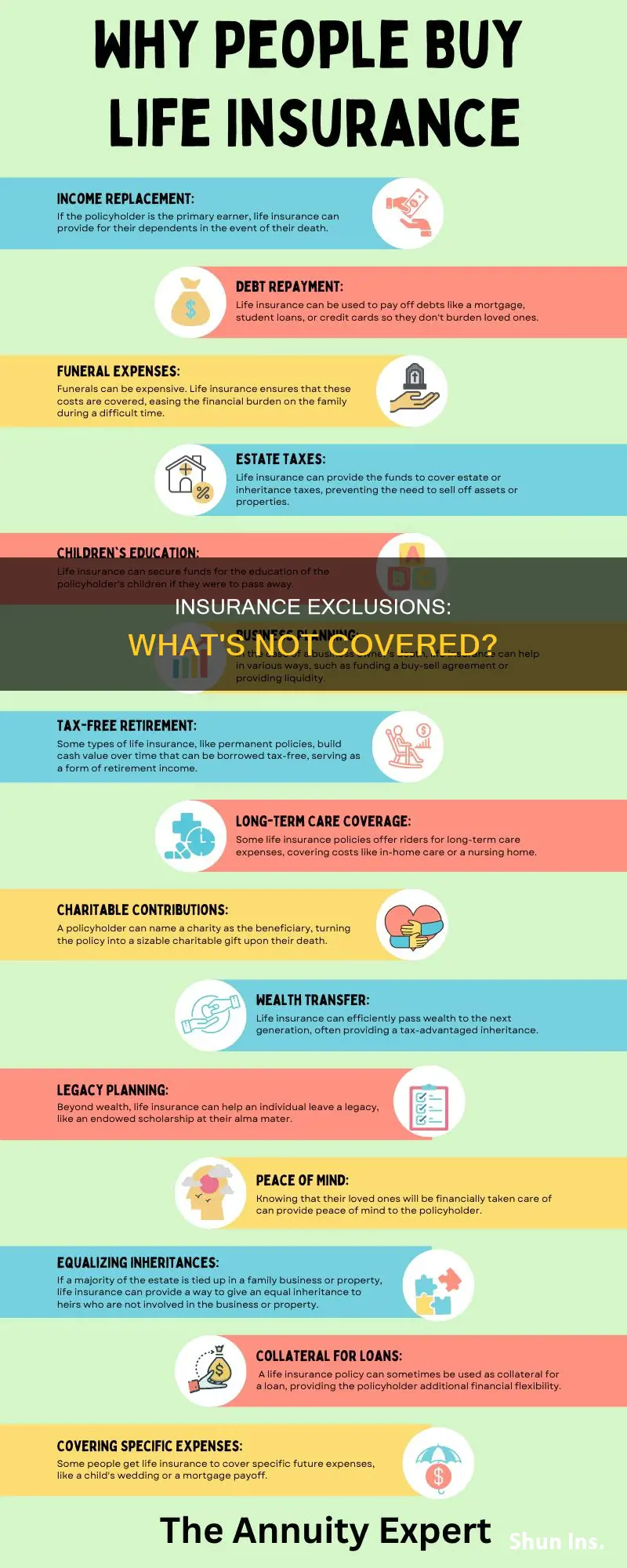

Insurance types: health, auto, life, liability, and home insurance all have different exclusions

Exclusions in insurance policies refer to provisions that eliminate coverage for certain acts, property, types of damage, or locations. These excluded costs do not count towards the plan's total out-of-pocket maximum. Exclusions vary across insurance types and providers, so it's important to carefully review your policy to understand what is and isn't covered. Here are some common exclusions for health, auto, life, liability, and home insurance:

Health Insurance

Historically, individual health insurance policies often excluded pre-existing medical conditions. However, since 2014, due to the Affordable Care Act, pre-existing condition exclusions are no longer permitted. Despite this, health insurance policies still contain various blanket exclusions that apply to all policyholders. Commonly excluded services include cosmetic surgery, weight-loss treatments, abortion, acupuncture, and dental care.

Auto Insurance

Auto insurance policies typically contain exclusions for specific drivers, meaning that claims may be denied if the incident involves an unnamed driver, even if they had permission to use the vehicle. Additionally, auto insurance often excludes incidents that occur during racing events, off-roading, or when the vehicle is used for business purposes. Mechanical failures, routine maintenance, and normal wear and tear are also generally not covered by auto insurance policies.

Life Insurance

Life insurance exclusions are designed to protect insurance companies from fraud and excessive risk. A common exclusion is the suicide clause, which denies a payout to beneficiaries if the policyholder dies by suicide within a certain timeframe of purchasing the policy. Life insurance policies may also exclude deaths resulting from illegal activities, risky hobbies (such as skydiving or rock climbing), and substance abuse.

Liability Insurance

Liability insurance typically covers damages that the policyholder is legally obligated to pay, such as bodily injury or property damage caused by the insured's actions. However, exclusions may apply in cases of intentional harm, contractual liability, or damage resulting from criminal acts.

Home Insurance

Home insurance policies commonly exclude coverage for natural disasters such as floods, earthquakes, landslides, and damage caused by earth movement. Pest infestations, mold (unless resulting from a covered peril), and war-related losses are also typically excluded from standard home insurance policies.

Dave Ramsey's Take on Medical Insurance

You may want to see also

Explore related products

![]()

Policy conditions: insurers can deny claims if policy conditions are not met, e.g. failing to protect property

An insurance policy is a legal contract between the insurance company (insurer) and the person(s), business, or entity being insured (insured). The insured purchases a policy that outlines what is covered, the exclusions that take away coverage, and the conditions that must be met in order for coverage to apply when a loss occurs.

Policy conditions are provisions inserted in the policy that qualify or place limitations on the insurer's promise to pay or perform. If the policy conditions are not met, the insurer can deny the claim. Common conditions in a policy include the requirement to file a proof of loss with the company, to protect property after a loss, and to cooperate during the company's investigation or defense of a liability lawsuit. For example, if your home is damaged, and you have not maintained your home or protected it from further damage after the incident, the insurance company may deny your claim.

It is important to understand that multi-peril policies may have specific exclusions and conditions for each type of coverage, such as collision coverage, medical payment coverage, liability coverage, and so on. The first part of an insurance policy usually identifies who is insured, what risks or property are covered, the policy limits, and the policy period (i.e., the time the policy is in force). For example, the declarations page of an automobile policy will include the description of the vehicle covered, the name of the person covered, the premium amount, and the deductible. Similarly, the declarations page of a life insurance policy will include the name of the person insured and the face amount of the policy.

In the Insuring Agreement, the insurer agrees to do certain things, such as paying losses for covered perils, providing certain services, or agreeing to defend the insured in a liability lawsuit. There are two basic forms of an insuring agreement: Named-Perils Coverage and All-Risk Coverage. Under Named-Perils Coverage, only the perils specifically listed in the policy are covered. If the peril is not listed, it is not covered. Under All-Risk Coverage, all losses are covered except those specifically excluded. If the loss is not excluded, then it is covered. Exclusions take coverage away from the Insuring Agreement. Typical examples of excluded perils under a homeowners policy are flood, earthquake, and nuclear radiation. A typical example of an excluded loss under an automobile policy is damage due to wear and tear.

If your claim is denied, you have the right to be told in writing why you have been denied coverage. If an insurance company violates your rights, you may be able to sue the company in court, including small claims court, with or without an attorney.

Umbrella Insurance: Medical Malpractice Coverage Explained

You may want to see also

Explore related products

![]()

Pre-existing conditions: the Affordable Care Act removed exclusions, but not for all plans

The Affordable Care Act (ACA), enacted in 2010 and implemented in 2014, brought significant changes to health insurance coverage, particularly regarding pre-existing conditions. The ACA introduced protections that prohibit insurance companies from denying coverage to individuals based on their health status, including pre-existing conditions. This marked a notable shift in the landscape of healthcare, offering greater accessibility to those previously facing challenges due to their medical histories.

However, it is important to note that these protections do not extend to all types of insurance plans. Specifically, "grandfathered" or "grandmothered" individual market plans, purchased independently rather than obtained through an employer, are exempt from the ACA's pre-existing condition provisions. These types of plans were acquired on or before March 23, 2010, and are not subject to the same regulations as plans offered through the Marketplace. As a result, they are not mandated to cover pre-existing conditions, and individuals with such plans may encounter exclusions or waiting periods for treatments related to their pre-existing conditions.

The distinction between Marketplace plans and grandfathered/grandmothered plans is crucial. Marketplace plans, introduced by the ACA, offer a comprehensive range of protections, including coverage for pre-existing conditions. In contrast, grandfathered/grandmothered plans are older plans that are no longer offered to new enrollees but continue to be renewed by existing policyholders. These plans may not include the same rights and protections as Marketplace plans, leaving individuals with pre-existing conditions potentially vulnerable to coverage gaps or higher costs.

It is worth noting that individuals with grandfathered plans who seek pre-existing condition coverage have options. They can switch to a Marketplace plan during Open Enrollment or purchase a Marketplace plan outside of Open Enrollment, qualifying for a Special Enrollment Period. By making this transition, individuals can ensure that their pre-existing conditions are covered, gaining access to the enhanced protections and peace of mind that comes with the ACA's regulations.

Understanding the intricacies of insurance policies is essential. Reading and comprehending the entirety of an insurance policy helps individuals make informed decisions and avoid potential issues or disagreements with their insurance provider. While the ACA has made significant strides in expanding coverage for pre-existing conditions, the specifics of an individual's plan, including any exclusions or limitations, remain critical factors in determining their healthcare journey.

Understanding the Interim: SSDI Medical Waiting Period and Health Insurance

You may want to see also

Explore related products

![]()

OFAC compliance: OFAC reviews global insurance policies to ensure they don't undermine US foreign policy

The Office of Foreign Assets Control (OFAC) is a federal agency that administers economic sanctions programs. OFAC is a division of the US Department of the Treasury and enforces, implements, and administers US economic sanctions. OFAC's regulations are based on presidential declarations of national emergency and preempt state insurance regulations.

OFAC compliance is crucial for insurance industry participants, including underwriters, brokers, and agents. They must comply with OFAC sanctions throughout their involvement with an insurance policy or other product or service. This includes checking OFAC's List of Specially Designated Nationals and Blocked Persons (SDN List) to ensure that no services are provided to those on the list.

In the context of global insurance policies, OFAC recognizes that US insurers often compete with non-US insurers who may issue policies without excluding sanctioned persons or jurisdictions. To address this, OFAC recommends that insurers apply for a specific license before issuing a global insurance policy that may involve coverage for sanctioned persons or activities. OFAC will review these policies to ensure they do not undermine US foreign policy by assessing the market position of the applicant, risk frequency, and severity.

Additionally, insurers should implement routine screening of all issued policies, policyholders, and beneficiaries to comply with OFAC regulatory requirements. OFAC also advises insurers to use a risk-based approach to sanctions compliance, with screening frequency varying depending on the size and nature of the insurer's business.

Insurers must also be aware of blocked funds due to OFAC-administered sanctions and notify policyholders accordingly. While payments to blocked persons are generally not aligned with US foreign policy objectives, there may be circumstances where payments to innocent third parties are authorized.

ACA Insurance and Medicaid: What's the Connection?

You may want to see also

Frequently asked questions

If your health insurance doesn't cover a procedure or test, you can reach out to your state's insurance commissioner, who can let you know if your health plan is running afoul of any specific rules. You can also investigate clinical trials, as sponsors may cover the cost of many tests, procedures, prescriptions, and healthcare provider visits.

An insurance policy is a legal contract between the insurance company (the insurer) and the person(s), business, or entity being insured (the insured). It's important to read the entire policy to understand what is covered, what isn't, and what conditions must be met for coverage to apply.

Named-perils coverage only covers the perils specifically listed in the policy. If the peril is not listed, it is not covered. All-risk coverage, on the other hand, covers all losses except those specifically excluded.

Typical examples of excluded perils under a homeowners policy include floods, earthquakes, and nuclear radiation.