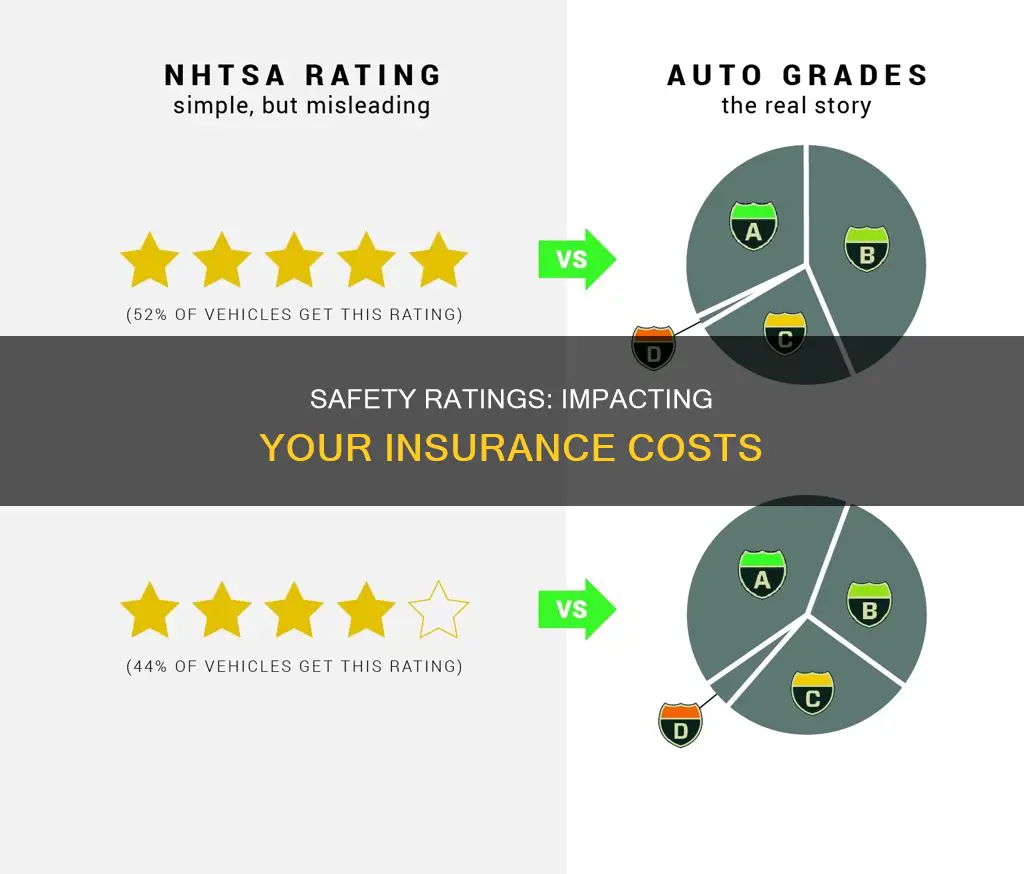

Safety ratings are one of the many factors that insurance companies consider when determining insurance rates. The Insurance Institute for Highway Safety (IIHS) and the National Highway Traffic Safety Administration (NHTSA) are two independent organizations that provide safety ratings for vehicles. The IIHS evaluates vehicles in three crashworthiness categories and rates safety features like pedestrian front crash prevention and headlight effectiveness. NHTSA, on the other hand, uses a 5-star rating system and conducts frontal, side, and rollover tests. While safety features like advanced driver assistance systems and automatic emergency braking can reduce insurance costs, they can also make vehicles more expensive to repair after accidents. Therefore, safety ratings do not always translate to lower insurance rates.

| Characteristics | Values |

|---|---|

| Factors affecting insurance cost | Anti-theft devices, vehicle size, driving history, driving activity, coverage options, deductibles, credit score, address |

| Safety features that reduce insurance costs | Airbags, anti-lock brakes, seat belts, daytime running lights, anti-theft devices, advanced driver assistance systems, automatic emergency braking, lane departure warning system, blind spot monitoring, rear automatic braking, blind spot intervention, forward collision warning system |

| Safety rating providers | Insurance Institute for Highway Safety (IIHS), National Highway Traffic Safety Administration (NHTSA) |

| IIHS rating categories | Good, Acceptable, Marginal, Poor |

| NHTSA rating categories | 5-Star Safety Ratings |

Explore related products

What You'll Learn

- Safety ratings don't always equal lower insurance rates

- Safety features can make vehicles more expensive to repair

- The Insurance Institute for Highway Safety (IIHS) and the National Highway Traffic Safety Administration (NHTSA) provide safety ratings

- Vehicle size and weight can affect insurance costs

- Safety features can reduce insurance costs

![]()

Safety ratings don't always equal lower insurance rates

Safety ratings are one of the many factors that insurance companies consider when determining insurance premiums. The Insurance Institute for Highway Safety (IIHS) and the National Highway Traffic Safety Administration (NHTSA) are two organisations that provide safety ratings for vehicles. The IIHS evaluates vehicles in three crashworthiness categories, while the NHTSA uses a 5-star scoring system. Both organisations assess how vehicles perform in crashes and how likely the risk of injury is to the passengers.

While safety ratings can influence insurance rates, they don't always result in lower premiums. This is because safety features that reduce accidents, such as sensors on mirrors, fenders, and bumpers, can also increase repair costs in the event of an accident. Other factors, such as vehicle size, driving history, and coverage amounts, can also impact insurance costs.

Advanced safety features, such as advanced driver assistance systems, automatic emergency braking, and lane departure warning systems, can reduce insurance costs. However, not all insurance companies recognise these features when calculating premiums. Additionally, the cost of these advanced safety systems may outweigh any potential savings on insurance.

When considering the impact of safety ratings on insurance rates, it's important to shop around and obtain quotes from multiple insurance providers. Contacting insurance providers directly and comparing rates for vehicles with and without optional safety features can help determine the value of these safety features in reducing insurance premiums.

In summary, while safety ratings can be a factor in determining insurance rates, they don't always guarantee lower premiums. Other factors, such as repair costs, vehicle characteristics, and individual insurance provider policies, can also influence the final insurance cost.

The Future of Auto Insurance: Is 21st Century a Good Choice?

You may want to see also

Explore related products

![]()

Safety features can make vehicles more expensive to repair

Secondly, the labour involved in repairing safety features can be costly. Newly installed radars and cameras must be calibrated, which requires special tools and hours of work. This is also true of sensors, which need to be recalibrated correctly, or there can be serious safety implications.

Thirdly, safety features can be more easily damaged. Large-diameter wheels with low-profile tires, for example, are more prone to damage from potholes.

Finally, older models with safety features may be more expensive to repair as they may be out of warranty.

Despite these additional costs, safety features are still worth investing in. They can save lives and prevent accidents, and insurance companies do take safety ratings into account when determining premiums. However, at present, the increase in repair costs is passed on to consumers, and insurance companies are yet to offer lower premiums for safer vehicles. This may change in the future as the technology becomes more common and effective at reducing accidents.

Employee National Insurance: Current Rate Explained

You may want to see also

Explore related products

![]()

The Insurance Institute for Highway Safety (IIHS) and the National Highway Traffic Safety Administration (NHTSA) provide safety ratings

NHTSA, on the other hand, is a government agency under the Department of Transportation. It has been testing vehicles since 1978, starting with frontal-impact crashes and later expanding to side and rollover crash tests. NHTSA's 5-Star Safety Ratings program evaluates vehicles' performance in frontal, side, and rollover crashes, with the latter being unique among safety rating organizations. The agency also provides Ease of Use Ratings for car seats and Uniform Tire Quality Grading Systems (UTQGS) ratings for tires.

Both organizations' safety ratings serve as valuable references for consumers when purchasing a vehicle. However, it is important to note that safety ratings do not always directly translate to lower insurance rates. While safety features can reduce accidents, they may also increase repair costs in the event of a crash. Additionally, other factors, such as vehicle size, driving history, and coverage options, also come into play when determining insurance costs.

To make informed decisions, consumers can refer to resources such as NHTSA's Vehicle Comparison Tool, which provides access to safety ratings and recall information. Additionally, contacting auto insurance providers for quotes on specific vehicles can help determine the impact of safety features on insurance rates.

Pennsylvania Insurance: Why the High Rates?

You may want to see also

Explore related products

![GMW Gun Magnet [2-Pack] | 30 lbs. Rating Magnetic Gun Mount | HQ Rubber Coated Gun Magnet Buckler Series for Car, Truck, Desks, Safes, and Walls | Indoor Gun Racks| Concealed Gun Holder for Handgun](https://m.media-amazon.com/images/I/71tzGiA6eFL._AC_UL320_.jpg)

![]()

Vehicle size and weight can affect insurance costs

Safety ratings are one of the many factors that insurance companies use to determine insurance premiums. While safety features can lower insurance costs, they don't always result in lower insurance rates. For example, safety features that reduce accidents, such as mirrors, fenders, and bumpers with sensors, can also increase repair costs in the event of an accident.

Vehicle size and weight are significant factors in determining insurance costs. Firstly, larger vehicles may have better crashworthiness compared to smaller vehicles due to their size and weight, resulting in lower insurance premiums. This is because small cars tend to be involved in more accidents and are therefore more expensive to insure. For instance, the Honda Accord, a relatively inexpensive vehicle, is the most stolen car in the country, and this factor drives up insurance premiums for this car despite its safety.

Secondly, modifications to a vehicle's wheel size can affect weight and, consequently, fuel efficiency and performance. Larger wheels increase weight, lower fuel efficiency, and put greater stress on the engine. This is particularly relevant for SUVs, which already have higher fuel consumption than smaller cars. Insurers consider off-road driving with larger wheels to be more dangerous due to the increased risk of accidents, tire punctures, or suspension damage. Therefore, modifications that increase wheel size may result in higher insurance premiums due to higher replacement costs and greater cosmetic damage risk.

Additionally, larger custom wheels often require specialized repairs, increasing repair costs. Furthermore, larger wheels may result in losing eligibility for eco-friendly driving discounts offered by some insurers, further contributing to higher insurance premiums.

In summary, while safety ratings and vehicle size and weight can influence insurance costs, other factors such as repair costs, the likelihood of theft, driving record, and vehicle usage also play a significant role in determining insurance premiums.

Freeze Auto Insurance: Yes or No?

You may want to see also

Explore related products

![]()

Safety features can reduce insurance costs

Safety features can have an impact on insurance costs, although it is important to note that this is not the only factor that insurance companies consider. Safety ratings are determined by testing agencies such as the Insurance Institute for Highway Safety (IIHS) and the National Highway Traffic Safety Administration (NHTSA). IIHS rates vehicles as good, acceptable, marginal, or poor, while NHTSA uses a 5-star rating system. These ratings provide valuable information about a vehicle's crashworthiness and crash avoidance capabilities.

When it comes to insurance costs, safety features can play a role in reducing premiums. Advanced safety features, such as automatic emergency braking, lane departure warning systems, and blind-spot monitoring, can lower insurance rates. These features not only protect you and your passengers but also demonstrate to insurance providers that the vehicle is safer, which may lead to reduced costs. Additionally, anti-theft devices are considered safety features that can lower insurance rates because they reduce the likelihood of vehicle theft.

However, it is important to consider that safety features can also increase repair costs in the event of an accident. This increase in repair costs may offset any potential savings from reduced insurance rates. The overall impact on insurance costs depends on various factors, including the specific safety features, the vehicle's size and weight, and the insurance provider's policies.

While safety ratings and features are important considerations, insurance companies also take into account other factors such as driving history, credit score, address, and coverage selections. These factors collectively contribute to determining insurance rates. Therefore, it is advisable to shop around for insurance quotes and consider multiple factors when making a decision.

In summary, safety features can indeed reduce insurance costs, but they are just one piece of the puzzle. Insurance companies consider a multitude of factors to determine rates, and it is essential to carefully review the details of different insurance providers to make an informed choice.

Joint Auto Insurance: Can We Get It?

You may want to see also

Frequently asked questions

Yes, a vehicle's safety rating is factored into insurance costs.

Most vehicles on the road today automatically come with airbags, anti-lock brakes, seat belts, daytime running lights, and anti-theft devices.

You can determine your vehicle's safety rating by looking up your car on the websites of The Insurance Institute for Highway Safety (IIHS) or the National Highway Traffic Safety Administration (NHTSA).

NHTSA uses a 5-Star scoring system, while the IIHS issues grades of Good, Acceptable, Marginal, and Poor. IIHS also rates safety-related features like pedestrian front crash prevention and headlight effectiveness.

Not always. While safety features that reduce accidents can lower insurance rates, they can also make vehicles more expensive to repair when accidents do happen.