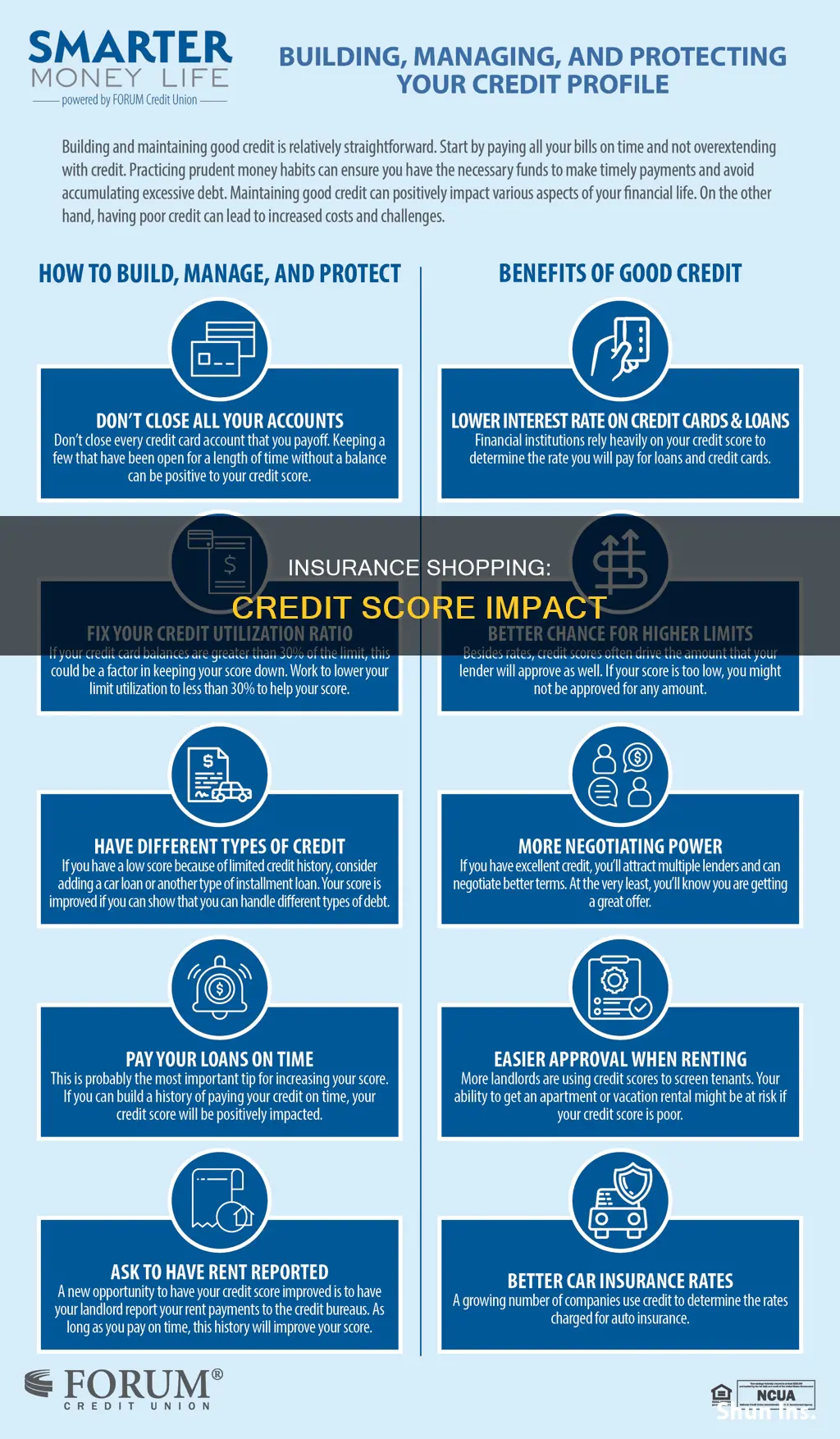

Shopping for insurance generally does not affect your credit score. While insurance companies do check your credit score when giving you a quote, this is considered a 'soft pull' or 'soft inquiry' and will not impact your credit score. A 'hard inquiry' or 'hard pull' occurs when a financial institution checks your credit history when making a lending decision, and this can lower your credit score. However, it is important to note that your credit score can impact your insurance premium or rate, with higher credit scores often resulting in lower premiums.

| Characteristics | Values |

|---|---|

| Does shopping for insurance affect credit score? | No, shopping for insurance does not affect your credit score. |

| How do insurance companies use credit scores? | Insurance companies use credit scores to predict the likelihood of a customer filing a claim and to determine insurance rates. |

| How does credit score affect insurance rates? | A good credit score can lead to lower insurance rates, while poor credit may result in higher premiums or difficulty in obtaining insurance. |

| Do all states consider credit scores for insurance? | No, some states prohibit or limit the use of credit scores in insurance, including California, Hawaii, Maryland, Michigan, and Massachusetts. |

| How can I improve my credit score? | Improving personal finance habits, such as maintaining timely payments and a good credit history, can positively impact your credit score. |

Explore related products

What You'll Learn

![]()

Getting insurance quotes: no impact on credit score

Getting an insurance quote won't affect your credit score, so you can shop around for the best rates without worrying about any negative impact on your creditworthiness. While insurance companies do check your credit score when giving you a quote, this is what's known as a 'soft pull' or 'soft inquiry'. This type of credit check won't affect your credit score, although it may show up on your credit report.

Soft inquiries are different from hard inquiries, which occur when a financial institution, such as a lender or credit card issuer, checks your credit history when making a lending decision. Hard inquiries commonly take place when you apply for a mortgage, loan or credit card, and they can lower your credit score. Soft inquiries, on the other hand, are recorded on your credit report so you can see who has inquired about your credit history, but they are not visible to lenders and do not affect your score.

Insurance companies check your credit score to gauge the risk they'll take on by insuring you. This helps them calculate insurance rates. Credit-based insurance scores can affect your eligibility for insurance and how much you pay in premiums. However, insurance companies generally can't refuse to insure you or cancel your policy based solely on your credit.

In addition, your credit score is not the only factor that affects your insurance premium. Depending on the type of insurance you're looking for, your driving history, geography, property value, and claim history can all influence how much you pay per month. So, when you're getting insurance quotes, make sure to look carefully at what the policy covers, rather than focusing solely on the price.

Breathalyzer Refusal: Insurance Impact and Consequences

You may want to see also

Explore related products

![]()

Credit-based insurance scores: affect eligibility and premiums

Credit-based insurance scores are a factor in determining eligibility and premiums. While getting a quote for insurance does require a credit check, it typically does not affect your credit score. This is because insurance quotes fall under "soft inquiries", which are not related to specific applications for new credit. Soft inquiries are recorded on your credit report, but they are not visible to lenders and do not impact your credit score.

In most states, credit-based insurance scores can impact your eligibility and premiums. Insurance companies use these scores to predict the likelihood of a customer filing an insurance claim. A higher credit score can lead to lower premiums, while poor credit may result in higher premiums or difficulty in obtaining insurance. However, it's important to note that insurance companies cannot solely rely on credit-based insurance scores to deny, cancel, or refuse to renew a policy.

The impact of credit-based insurance scores on premiums was studied by the Arkansas Insurance Department in 2017. The study found that using credit-based insurance scores decreased premiums for 57.4% of auto policies, increased premiums for 23.4%, and had no effect on 19.2% of policies.

While shopping for insurance, it is beneficial to get multiple quotes to find the best coverage and rates. Since getting quotes does not affect your credit score, you can compare prices and choose the option that suits your needs without worrying about negative consequences on your credit.

Additionally, it is worth noting that state laws differ regarding the use of credit to set insurance rates. Certain states, such as California, Hawaii, Maryland, Michigan, and Massachusetts, prohibit or limit the use of credit information in insurance. Therefore, it is advisable to contact your state's department of insurance to understand the specific rules and regulations that apply to your location.

Understanding Auto Insurance: A Beginner's Guide

You may want to see also

Explore related products

![]()

Poor credit: leads to higher insurance rates

Poor credit can have a significant impact on insurance rates, leading to higher premiums and, in some cases, difficulty in obtaining insurance. While getting a quote for insurance will not affect your credit score, insurance companies may use a credit-based insurance score when reviewing your application. This score is based on a range of factors, including your credit history and credit report.

In most states, credit-based insurance scores can affect eligibility and premiums. Poor credit can make it harder to obtain insurance and lead to higher premiums. The impact of poor credit on insurance rates varies depending on the state and the insurance company. For example, in North Carolina, a drop in credit score from Exceptional to Very Poor leads to a 74% rate increase, while in Minnesota, the same drop results in a 285% rate increase.

Insurance companies consider individuals with lower credit scores to be higher-risk. Research by the Federal Trade Commission has shown that individuals with lower credit scores are more likely to file insurance claims, even when controlling for factors such as race, income, and location. This correlation may be due to a perception of higher financial risk associated with lower credit scores.

The impact of poor credit on insurance rates can be substantial. On average, drivers with poor credit pay $1,500 more per year than those with perfect scores. Additionally, poor credit increases full coverage rates by 95% compared to good credit. For example, a driver with poor credit may pay $406 more per month with State Farm, while with Nationwide, the increase is only $95 per month.

While poor credit can lead to higher insurance rates, it is important to note that improving your credit score can take time. Strategies such as diversifying your credit, maintaining low credit card balances, and timely bill payment can help boost your credit score and potentially lead to reduced insurance premiums over time.

Avoid Insurance Hikes: Strategies Post-Speeding Ticket

You may want to see also

Explore related products

![]()

Driving record: a factor in insurance rates

Getting a car insurance quote typically requires a credit check, but it will not negatively impact your credit score. This is because car insurance quotes are considered “soft inquiries”, which are not related to specific applications for new credit. However, credit-based insurance scores can be a factor in determining eligibility and premiums. A good credit score may result in more options and lower insurance costs, while poor credit could make obtaining insurance more challenging and lead to higher premiums.

Your driving record is a significant factor in determining your insurance rates. Insurance companies use your driving history to assess your risk profile and predict the likelihood of future claims. A clean driving record indicates responsible and low-risk behaviour, suggesting that you are less likely to file claims. As a result, insurers offer lower premiums to drivers with a history of safe driving. Conversely, a driving record with accidents, traffic violations, or claims may lead to higher premiums as insurers classify these drivers as higher-risk.

The frequency and severity of claims also play a role in insurance rates. Multiple claims, regardless of fault, can indicate a pattern of higher risk or careless driving behaviour. Significant damages associated with claims can result in increased premiums. Additionally, driving records with speeding tickets, DUIs, or reckless driving charges will generally lead to higher insurance costs.

Age and driving experience are also considered, with young and inexperienced drivers often paying higher insurance rates due to their higher risk of accidents. As drivers gain experience and maintain a clean driving record, their premiums tend to decrease, typically reaching the lowest point in their mid-50s. However, as drivers age further, reaction times may decline, leading to an increase in insurance rates for seniors.

It is important to note that each insurer weighs factors differently, and other considerations, such as gender, marital status, annual mileage, and coverage choices, can also influence insurance costs. Maintaining a clean driving record and shopping around for insurance rates can help drivers obtain the best rates and ensure they are not overpaying for their coverage.

Auto Insurance Discounts for Veterans: Best Companies

You may want to see also

Explore related products

![]()

State regulations: determine use of credit-based insurance scores

In the United States, state regulations determine whether insurance companies can use credit-based insurance scores when offering or renewing a policy, or when deciding how much to charge in premiums. While most states allow insurance companies to use credit-based insurance scores, they can't be the sole reason for a decision.

Seven states forbid home and auto insurance companies from using credit-based insurance scores. These states include California, Hawaii, and Maryland. In California, insurance companies don't use credit-based scores or credit history for underwriting or rating auto policies, or for setting rates for homeowners insurance. In Hawaii, auto insurers cannot use credit ratings when setting underwriting standards and rating plans, which determine insurance premiums. In Maryland, homeowners insurance companies cannot refuse coverage, cancel a policy, refuse to renew a policy, or base insurance rates on an individual's credit history.

In states that allow insurance companies to consider credit standing, improving one's credit can help lower insurance rates. Credit-based insurance scores are based on similar factors that influence regular credit scores, such as payment history, outstanding debt, credit history length, pursuit of new credit, and credit mix.

While getting a car insurance quote does require a credit check, it typically won't hurt one's credit score as it is considered a ""soft inquiry". Soft inquiries are recorded on one's credit report but do not affect one's credit score.

Mile Auto: Good Insurance Option?

You may want to see also

Frequently asked questions

No, shopping for insurance will not affect your credit score. Getting a quote for insurance is considered a "soft inquiry" and will not impact your score.

A hard inquiry or "hard pull" occurs when a financial institution checks your credit history when making a lending decision. This can lower your credit score. A soft inquiry or "soft pull" occurs when a person or company checks your credit history as part of a background check or for other permissible purposes. Soft inquiries do not affect your credit score.

A higher credit score can lead to lower insurance premiums. Poor credit may make it harder to get insurance or lead to higher premiums. Credit-based insurance scores are used to predict the likelihood of a customer filing an insurance claim.

Your driving record, insurance history, geography, property value, and claim history can all affect your insurance premium.