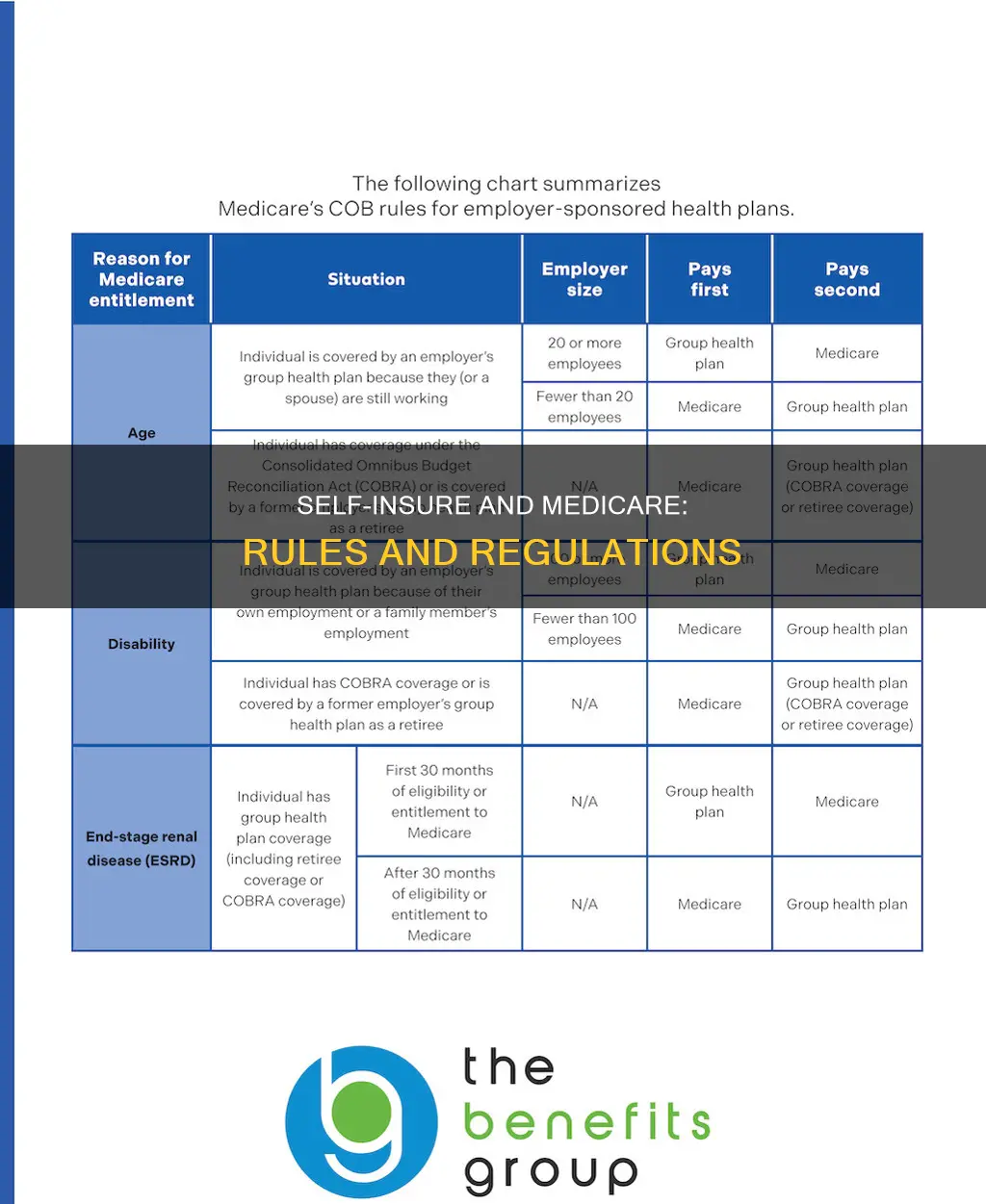

Medicare is a health insurance program for people aged 65 and over, as well as some younger people with disabilities. When an individual has Medicare and other health insurance, each type of coverage is called a payer. The primary payer pays up to the limits of its coverage, then sends the remaining balance to the secondary payer. Self-insured health insurance, on the other hand, is a type of insurance where the employer assumes the financial risk of providing healthcare benefits to its employees, rather than purchasing health insurance from an external insurer. While self-insured plans are subject to some federal regulations, such as the HIPAA rules and the ACA rules, they are exempt from certain federal requirements, such as medical loss ratio rules. The correlation between self-insured plans and Medicare rules can be observed in the coordination of benefits, where Medicare may act as the secondary payer when an individual has a self-insured plan as their primary coverage.

| Characteristics | Values |

|---|---|

| Medicare with other insurance | Each type of coverage is called a "payer". The "primary payer" pays up to its limit, then sends the remaining balance to the "secondary payer". |

| Medicare with group health coverage | TRICARE pays first for Medicare-covered services or items, and Medicare pays second. |

| Medicare with retiree coverage | You may need to sign up for Medicare Part B before they'll pay. |

| Medicare with no-fault or liability insurance claim | The liability or no-fault insurance must pay first. |

| Self-insured plans | Not subject to state-based laws and regulations. Not required to include coverage for ACA essential health benefits. |

| Self-insured plans federal requirements | Subject to HIPAA rules, ACA rules, the Pregnancy Discrimination Act, COBRA, and the No Surprises Act. |

Explore related products

What You'll Learn

![]()

Medicare and other insurance coordination of benefits

If you have Medicare and other health insurance, each type of coverage is called a "payer". The "primary payer" pays up to the limit of its coverage and then sends the remaining balance to the "secondary payer". If the "secondary payer" does not cover the remaining balance, you may be responsible for the remaining costs. This order of payment is called "coordination of benefits" (COB).

COB allows plans that provide health and/or prescription coverage for a person with Medicare to determine their respective payment responsibilities. It ensures claims are paid correctly by identifying the health benefits available to a Medicare beneficiary, coordinating the payment process, and ensuring that the primary payer, whether Medicare or other insurance, pays first.

The Benefits Coordination & Recovery Center (BCRC) takes action to identify the health benefits available to a beneficiary and coordinates the payment process to prevent mistaken payment of Medicare benefits. The BCRC does not process claims, nor does it handle any GHP-related mistaken payment recoveries or claims-specific inquiries. The Medicare Administrative Contractors (MACs), Intermediaries, and Carriers are responsible for processing claims submitted for primary or secondary payment.

If you have questions about who pays first, or if your coverage changes, you can call the Benefits Coordination & Recovery Center at 1-855-798-2627 (TTY: 1-855-797-2627). You should also tell your doctor and other healthcare providers about any changes in your insurance or coverage when you get care.

Full-Time Students: Understanding Medical Insurance Credits

You may want to see also

Explore related products

![]()

Self-insured plans and state-based laws

Self-insured health plans are not subject to state insurance laws and oversight. Instead, they are regulated at the federal level under the Employee Retirement Income Security Act (ERISA) and various provisions in other federal laws like the Health Insurance Portability and Accountability Act (HIPAA) and the Affordable Care Act (ACA).

State-based laws and regulations only pertain to fully insured plans and do not apply to self-insured plans. For example, when a state imposes rules requiring health plans to cover vasectomies or infertility treatment, these requirements do not apply to self-insured plans. This can cause frustration and confusion for residents with self-insured plans, who may not be aware that new state rules do not apply to their coverage.

There are some basic federal minimum standards that apply to self-insured plans, including HIPAA rules prohibiting employer-sponsored plans from rejecting an eligible employee or dependent based on medical history, and ACA rules prohibiting plans from imposing waiting periods for pre-existing conditions. The Pregnancy Discrimination Act applies to all health plans with 15 or more employees, including self-insured plans, and requires employer-sponsored health plans to include maternity coverage.

Self-insured plans are also subject to the Consolidated Omnibus Budget Reconciliation Act (COBRA), which allows eligible employees and their dependents to continue their coverage if a life change event would otherwise result in a coverage termination. While the majority of federal requirements do not apply to self-insured plans, there are some exceptions, such as the No Surprises Act, which protects consumers from "surprise" balance billing.

Should Businesses Provide Medical Insurance to Their Employees?

You may want to see also

Explore related products

![]()

Federal requirements for self-insured plans

Self-insured health plans, also known as self-funded health plans, are typically offered by employers or associations that assume the risk of providing coverage instead of purchasing it from an insurance company. Self-insured plans are not subject to state insurance laws and oversight but are regulated at the federal level under the Employee Retirement Income Security Act (ERISA).

Self-insured plans are required to comply with all applicable federal laws, including:

- The Health Insurance Portability and Accountability Act (HIPAA)

- The Consolidated Omnibus Budget Reconciliation Act (COBRA)

- The Americans with Disabilities Act (ADA)

- The Pregnancy Discrimination Act

- The Age Discrimination in Employment Act

- The Civil Rights Act

- Various budget reconciliation acts, such as the Tax Equity and Fiscal Responsibility Act (TEFRA)

The Affordable Care Act (ACA) has also introduced changes that impact self-insured plans. For example, sponsors of self-funded, non-Federal governmental plans can no longer opt out of as many requirements of Title XXVII. Additionally, the ACA prohibits plans from imposing waiting periods for pre-existing conditions.

Furthermore, the No Surprises Act, which took effect in 2022, protects consumers from "surprise" balance billing and applies to both self-insured and fully insured plans nationwide.

It is important to note that while self-insured plans are not subject to state insurance laws, they may still opt into certain state requirements. Additionally, there are some federal requirements that do not apply to self-insured plans, such as medical loss ratio rules and the requirement to include coverage for the ACA's essential health benefits.

Medical Insurance Enrollment: Timing and Your Options

You may want to see also

Explore related products

![]()

Self-insured plans and essential health benefits

Self-insured health plans are also known as self-funded plans. When employers want to offer health insurance to their workers, they can choose between a self-insured plan and a fully insured plan. In a self-insured plan, the employer uses its own money to cover the health claims of its employees. Most self-insured employers contract with an insurance company or third-party administrator (TPA) for plan administration, but the actual costs are covered by the employer.

Self-insured plans are not subject to state-based laws and regulations. State-based health insurance mandates do not apply to self-insured plans. For example, when a state imposes rules requiring health plans to cover vasectomies or infertility treatment, these requirements do not apply to self-insured plans. This can cause frustration and confusion for residents with self-insured plans. Nearly two-thirds of people with employer-sponsored health insurance are covered under self-insured plans.

There are some basic federal minimum standards that apply to self-insured plans. This includes the HIPAA rules that prohibit employer-sponsored plans from rejecting an eligible employee or dependent based on medical history. The ACA rules prohibit plans from imposing waiting periods for pre-existing conditions. The Pregnancy Discrimination Act applies to all health plans with 15 or more employees, including self-insured plans. Self-insured plans are also subject to COBRA, which means eligible employees and their dependents can opt to continue their coverage if a life change event would otherwise result in a coverage termination.

Self-insured plans do not have to include coverage for the ACA's essential health benefits (EHB), except for preventive care, which must be covered without cost-sharing on all non-grandfathered plans. Any essential health benefits that are covered cannot have annual or lifetime caps on the benefit amount. The EHB-benchmark plans displayed may include annual and/or lifetime dollar limits, but these limits cannot be applied to the essential health benefits. For example, abortion services are not required to be covered by health plans as part of the EHB requirement, but issuers can choose to cover them.

Dental and Vision: What Does Your Medical Insurance Cover?

You may want to see also

Explore related products

![]()

Medicare and TRICARE coverage for active duty personnel

TRICARE is a healthcare program for active-duty service members, active-duty family members, National Guard and Reserve members, and their families, retirees, retiree family members, survivors, and certain former spouses worldwide. TRICARE combines the healthcare resources of the Military Health System, including military hospitals and clinics, with a network of civilian healthcare professionals, institutions, pharmacies, and suppliers.

Each TRICARE plan has different costs for care and coverage. TRICARE offers prescription drug coverage, and beneficiaries have the same prescription coverage with any TRICARE health plan. However, if enrolled in the US Family Health Plan, separate pharmacy coverage is required. Dental coverage is also separate from TRICARE's medical coverage and is based on the individual's status.

TRICARE For Life (TFL) is Medicare-wraparound coverage for those who are TRICARE-eligible and have Medicare Part A and B, regardless of age or residence. TFL does not extend coverage to family members. To use TFL, individuals must have their Medicare card and military ID as proof of coverage. When visiting a provider, Medicare pays its portion first, and the remaining claim is sent to the TRICARE For Life claims processor.

If an individual has Medicare and other health insurance, each type of coverage is called a "payer." The "primary payer" pays up to its limit, then sends the remaining balance to the "secondary payer." If the secondary payer does not cover the remaining balance, the individual may be responsible for the remaining costs. This order of payment is called "coordination of benefits."

Self-insured plans are not subject to state-based laws and regulations that apply to fully insured plans. However, there are some federal requirements that do apply to self-insured plans, including HIPAA rules, ACA rules prohibiting waiting periods for pre-existing conditions, the Pregnancy Discrimination Act, and COBRA. Additionally, the federal No Surprises Act of 2022 protects consumers from "surprise" balance billing in both self-insured and fully insured plans. While self-insured plans are exempt from medical loss ratio rules, they must cover preventive care without cost-sharing on all non-grandfathered plans.

Car Accidents: When to Report to Insurance

You may want to see also

Frequently asked questions

Self-insured health insurance is when an employer chooses to pay for their employees' medical expenses out-of-pocket instead of purchasing health insurance. Nearly two-thirds of people with employer-sponsored health insurance are covered under self-insured plans.

Each type of insurance coverage is called a "payer". The "primary payer" pays up to the limits of its coverage, then sends the remaining balance to the "secondary payer". If the secondary payer doesn't cover the remaining balance, the patient may be responsible for the remaining costs.

Medical loss ratio rules do not apply to self-insured plans. Self-insured plans do not have to include coverage for the ACA's essential health benefits, except for preventive care, which must be covered without cost-sharing on all non-grandfathered plans.

Some basic federal minimum standards that apply to self-insured plans include HIPAA rules, ACA rules, and the Pregnancy Discrimination Act. Self-insured plans are also subject to COBRA, which allows employees to continue their coverage after a life change event.

It's important to ask your employer if you need to sign up for Medicare Part A (Hospital Insurance) and Part B (Medical Insurance) when you turn 65. If you don't, your job-based insurance might not cover your costs for services. Signing up for Medicare before your current coverage ends can help avoid a gap in coverage.