Transitioning from private health insurance to Medicare can be a complex process, and there are several factors to consider. Firstly, it's important to determine your Medicare enrollment period. If you've been receiving Social Security or Railroad Retirement Board benefits for at least four months before turning 65, the government will typically enroll you automatically in Medicare Parts A and B. For others, there is an initial seven-month window to enroll, starting three months before turning 65 and ending three months after your birthday month. It's worth noting that you may be eligible for Medicare earlier if you have a disability, End-Stage Renal Disease (ESRM), or ALS. When transitioning, you must decide whether to end your private insurance coverage or continue paying for it at full price, as Medicare does not automatically end your previous coverage. Additionally, you'll need to choose between Original Medicare (Parts A and B) and Medicare Advantage (Part C), which serves as an alternative to Original Medicare and offers additional coverage for services like vision, dental, and prescription drugs.

| Characteristics | Values |

|---|---|

| Initial Enrollment Period | The first time you can sign up for Medicare is usually when you turn 65 |

| Medicare Part A | Hospital Insurance |

| Medicare Part B | Medical Insurance |

| Medicare Part C | Medicare Advantage plans are comprehensive bundled plans that serve as an alternative to Original Medicare (Parts A and B) |

| Medicare Part D | Helps cover the cost of brand-name and generic drugs |

| Monthly premium | For Medicare Part B, all participants pay a monthly premium, which isn't mandatory and most people enroll only when they lack "creditable coverage" from another source |

| Late enrollment penalties | If you miss your Initial Enrollment Period, you may have to pay monthly late enrollment penalties that increase the longer you wait |

| Medicare Advantage Plan | You must have both Part A and Part B to join a Medicare Advantage Plan |

| Cost saving programs | Medicare offers programs to help lower your premiums and costs |

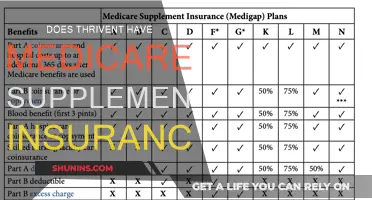

| Coverage options | Medicare offers options for additional coverage, including prescription drug coverage and extra benefits like vision, hearing, and dental |

| Marketplace coverage | If you have Medicare, you can keep your Marketplace plan but you'll pay full price for it |

| Enrollment periods | You can only join, switch, or drop a Medicare Advantage Plan or Medicare drug plan during certain enrollment periods |

| Special Enrollment Periods | You can make changes to your Medicare Advantage and Medicare drug coverage during certain life events, such as if you move or lose other coverage |

Explore related products

What You'll Learn

![]()

Understanding Medicare Parts A, B, C, and D

Medicare is a federal health insurance program for people aged 65 and over, as well as certain younger people with disabilities, and those with End-Stage Renal Disease. When you turn 65, you will have an "Initial Enrollment Period" during which you can sign up for Medicare.

Medicare is divided into four parts: A, B, C, and D, which cover everything from hospital care to doctor visits to prescription drugs. Here is a breakdown of each part:

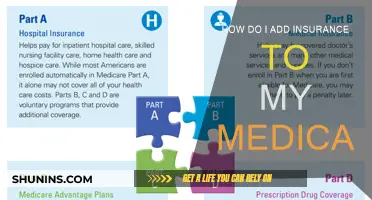

Part A: Hospital Insurance

Part A covers inpatient care in hospitals, skilled nursing facility care, hospice care, and home health care. It is free if you have worked and paid Medicare taxes for at least 10 years, or if you are eligible due to your spouse's work. However, there is a deductible for each benefit period, which was $1,632 in 2024. You will also be subject to an annual deductible, which was $240 in 2024. Part A does not cover all hospital services, and you may need to pay out-of-pocket costs for items not covered by your plan.

Part B: Medical Insurance

Part B covers doctor visits and other medical services. Most people pay a monthly premium for Part B, with the exact amount depending on their income level. If you have other insurance through your job or your spouse's job, you may want to defer signing up for Part B when you first enroll in Medicare. However, if you do not sign up for Part B during your initial enrollment and do not have other coverage, you may have to pay a late enrollment penalty.

Part C: Medicare Advantage

Part C, also known as Medicare Advantage, is an alternative to Parts A and B. It is a bundled plan offered by private companies that includes Parts A, B, and usually Part D. Part C may offer additional benefits not covered by Original Medicare, but it may also have different out-of-pocket costs. You must sign up for Part A or Part B before enrolling in Part C.

Part D: Prescription Drug Coverage

Part D helps cover the cost of prescription drugs, including recommended shots and vaccines. It is offered by private insurers and can be added to Original Medicare or included in a Medicare Advantage Plan. Each plan has different premiums, deductibles, and copayment tiers for prescription drugs, with generics costing less than brand-name medications.

When transitioning from private insurance to Medicare, it is important to review the costs, coverage, and benefits of each part to determine which plan best suits your needs and budget. You can use tools like Medicare's Plan Finder to compare plans and premiums. Additionally, if you have other insurance, it is essential to speak with your benefits administrator before making any changes to your current coverage.

Blue Cross Blue Shield: Weight Loss Medication Coverage

You may want to see also

Explore related products

$40.11 $245.95

$19.95 $19.95

![]()

How to switch from private insurance

Switching from private insurance to Medicare can be a complicated process. Here is a step-by-step guide on how to make the switch:

Step 1: Understanding Eligibility and Timing

Before switching to Medicare, it is important to understand the eligibility criteria and the ideal timing for making the switch. Your first chance to sign up for Medicare is usually during your Initial Enrollment Period, which starts three months before you turn 65 and ends three months after your 65th birthday. However, you may be eligible for Medicare earlier if you have a disability, End-Stage Renal Disease (ESRD), or ALS.

Step 2: Choosing the Right Medicare Plan

Medicare offers various plans, including Part A (Hospital Insurance), Part B (Medical Insurance), and Medicare Advantage (Part C). You can choose between Original Medicare (Parts A and B) and Medicare Advantage. Consider your specific needs and compare the costs and coverage of each plan to make an informed decision.

Step 3: Ending Your Private Insurance Coverage

Before ending your private insurance coverage, consult your benefits administrator or insurance provider to understand how your private insurance works with Medicare. If you have Marketplace coverage, you will need to update your application to end this coverage before Medicare starts. Contact your insurance company to inform them about the change and confirm the date your private insurance coverage will end.

Step 4: Enrolling in Medicare

Once you have chosen the Medicare plan that suits your needs, you can enrol by selecting "Enroll" for the desired plan at Medicare.gov/plan-compare. You can also contact the plan provider by calling or visiting their website. Alternatively, you can request a paper form to fill out and mail back to the plan provider before the enrollment period ends.

Step 5: Understanding Coordination of Benefits

If you have both Medicare and private insurance, each type of coverage is assigned a "payer". The "primary payer" pays up to its coverage limits and then sends the remaining balance to the "secondary payer". Understanding the coordination of benefits is crucial to ensure you are not left with unexpected costs. Contact Medicare's Benefits Coordination and Recovery Center for assistance in understanding how your coverage options work together.

Switching from private insurance to Medicare requires careful consideration and planning. Remember to review your options thoroughly and seek assistance from official sources, such as Medicare or the Social Security Administration (SSA), if you have any questions or concerns during the process.

Medical Insurance: Mandatory Coverage Now Abolished?

You may want to see also

Explore related products

![]()

Costs and savings

When switching from private insurance to Medicare, there are a few cost considerations to keep in mind. Firstly, it's important to understand the difference between Medicare Part A (Hospital Insurance) and Medicare Advantage (Part C). If you have Medicare Part A, you can choose to either keep your private insurance or switch to Medicare as your primary coverage. However, if you have Medicare Advantage, you should end your private insurance coverage.

Medicare premiums are a monthly amount that you pay for your chosen coverage, regardless of whether you use the services or not. Out-of-pocket costs, on the other hand, are the expenses you incur when you utilise the services covered by your plan, such as deductibles, co-pays, and coinsurance. Additionally, you may have to pay for any items or services that are not covered by your Medicare plan.

If you decide to keep your private insurance plan along with Medicare, be aware that you will need to pay full price for your private insurance. Your insurance company may also choose to terminate your private coverage. It is important to note that it is illegal for someone who knows you have Medicare to sell you a private insurance plan.

To save costs, Medicare offers programs that can help lower your premiums and out-of-pocket expenses. You can also explore options for additional coverage, such as prescription drug coverage, and extra benefits like vision, hearing, and dental care. These choices can provide more comprehensive protection and potentially reduce your overall healthcare expenses.

Finally, when switching to Medicare, timing is crucial. Your first opportunity to enrol in Medicare is during your Initial Enrollment Period, which typically begins three months before you turn 65 and ends three months after your birthday. If you miss this window, you may have to pay monthly late enrolment penalties, and your coverage may be delayed.

Health Insurance Options During Ongoing Medical Treatment

You may want to see also

Explore related products

![Orzly Glass Screen Protectors Compatible with Nintendo Switch - Premium Tempered Glass Screen Protector Twin Pack [2X Screen Guards - 0.24mm] for 6.2 Inch Tablet Screen on Nintendo Switch Console](https://m.media-amazon.com/images/I/711hVr97pNL._AC_UL320_.jpg)

![]()

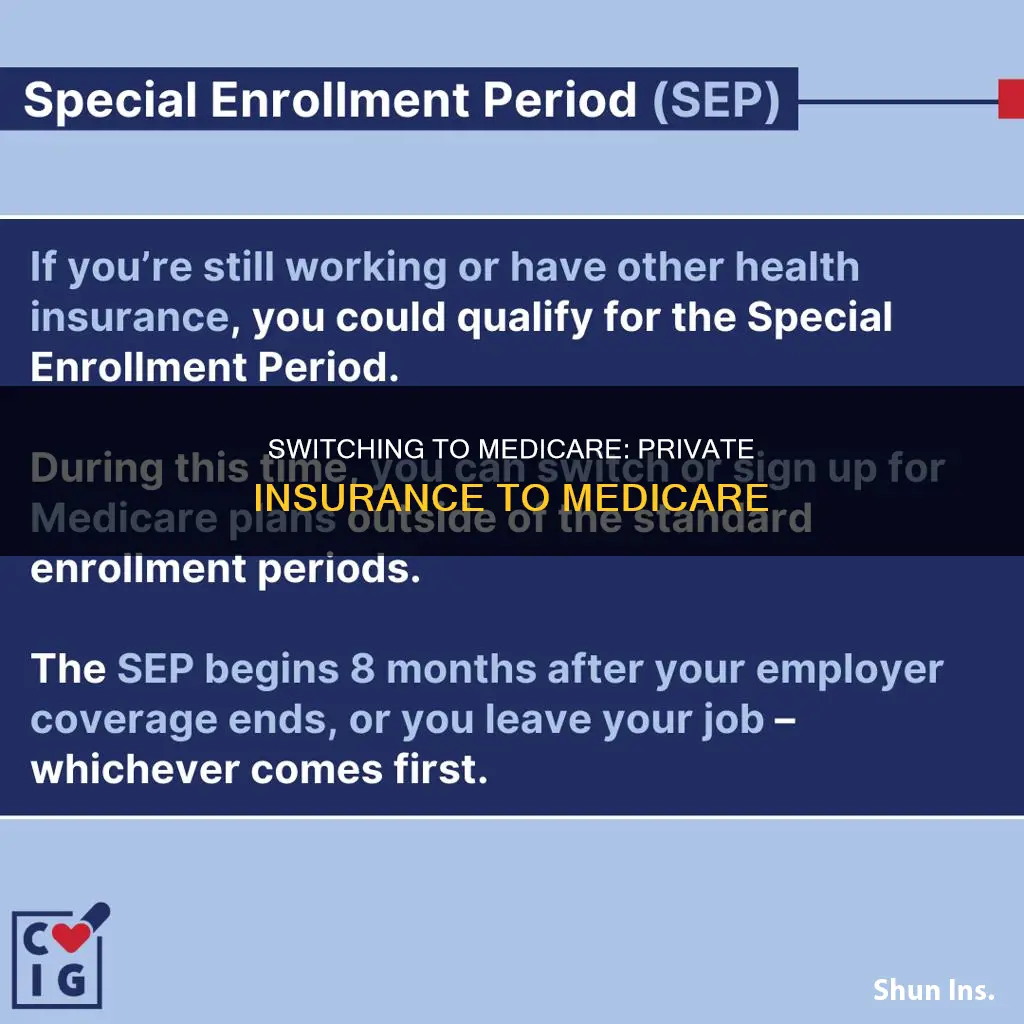

Special enrollment periods

It is important to act promptly when a change in circumstances occurs, as there are deadlines for making changes to your coverage during a SEP. You can contact Medicare to find out when and how to change your coverage. Failing to meet the deadlines may result in penalties.

If you have health insurance through your employer, it is important to sign up for Medicare Part A and Part B as soon as you are eligible, or you may face late enrollment penalties. A SEP may allow you to sign up for Medicare Part D (prescription drug coverage) if you become eligible and do not already have creditable prescription drug coverage. However, a penalty may still be incurred.

If you joined a Medicare Advantage Plan (Part C) during your Initial Enrollment Period, you can change to another Medicare Advantage Plan or switch to Original Medicare (Parts A and B) within the first three months of having Medicare Parts A and B coverage.

Medical Payments for Home Insurance: Do They Cover Lost Wages?

You may want to see also

Explore related products

![]()

Medicare Advantage Plans

Medicare Advantage, also known as Medicare Part C, is an alternative to Original Medicare. Private insurance companies that sell Medicare Advantage plans contract with the federal government to provide health insurance benefits to people eligible for Medicare.

In 2023, 49% of Medicare beneficiaries were enrolled in Medicare Advantage plans, and by 2025, over half of total Medicare enrollment is projected to be in these plans. Medicare Advantage plans may be a good choice for some, but they are not right for everyone. They offer lower costs, with many plans having no monthly premiums, and spending caps on out-of-pocket expenses. However, there may be restrictions on switching back to Original Medicare, and you may need prior authorization for certain tests or procedures, which can delay care.

If you are considering switching from private insurance to Medicare, you can choose to enroll in a Medicare Advantage plan during your Initial Enrollment Period, which is usually when you turn 65. You will need to end your Marketplace coverage and may have to pay a monthly late enrollment penalty if you miss this period. To enroll, you will need your Medicare Number and your Part A and/or Part B coverage start dates, which can be found on your Medicare card.

Christian Health Ministries: Double Insurance or Smart Strategy?

You may want to see also

Frequently asked questions

The first step is to determine your Medicare enrollment period. If you’ve received Social Security or Railroad Retirement Board benefits for at least four months before turning 65, the government will typically automatically enrol you in Medicare Parts A and B (Original Medicare) when you turn 65. If not, you can enrol during the Initial Enrollment Period, which is a seven-month window that begins three months before you turn 65 and ends three months after your 65th birthday.

There are two main types of Medicare plans: Original Medicare (Parts A and B) and Medicare Advantage (Part C). Original Medicare includes Part A (Hospital Insurance) and Part B (Medical Insurance). Medicare Advantage is an alternative to Original Medicare and offers additional coverage for services that Original Medicare doesn’t cover, such as vision, dental, hearing, prescription drugs, and more.

Yes, you can keep your private insurance plan after enrolling in Medicare, but there may be additional rules and costs depending on your specific plans. If you have Medicare and private insurance, each type of coverage is called a "payer". The "primary payer" pays up to the limits of its coverage and then sends the rest of the balance to the "secondary payer". You may need to pay a monthly premium for Medicare Part B, but delaying enrolment does not trigger a penalty as long as you enrol within eight months of losing coverage from your private insurance.

![ArmorSuit MilitaryShield Anti-Glare Screen Protector for Nintendo Switch - [Max Coverage] Anti-Bubble Matte Film](https://m.media-amazon.com/images/I/61v-t9+DLoL._AC_UL320_.jpg)