Summerville, South Carolina, has varying insurance rates depending on the type of insurance and several other factors. Car insurance rates in Summerville differ from driver to driver and are influenced by factors such as age, vehicle type, driving history, claims history, and location. Summerville's proximity to the coast and its high population density contribute to higher-than-average car insurance rates compared to the national average. On the other hand, homeowners in Summerville face higher insurance rates due to the increased risk of hurricanes, storms, and flooding in the area. Golf cart insurance rates in Summerville can also vary depending on the type of golf cart and its intended use, with street-legal and off-road golf carts typically commanding higher insurance rates. Overall, insurance rates in Summerville are influenced by a combination of local factors and individual circumstances.

| Characteristics | Values |

|---|---|

| Car insurance rates | $185.25 per month compared to the national average of $167.23 per month |

| Car insurance rates for teens and young adults | $420.66 per month |

| Car insurance rates for drivers in their 30s | $147.76 per month |

| Car insurance rates for drivers in their 40s | $149.82 per month |

| Car insurance rates for female drivers | Slightly less than male drivers |

| Car insurance rates for drivers with one accident | $164 per month |

| Car insurance rates for drivers with one ticket | $166 per month |

| Car insurance rates for trucks and vans | $114 per month |

| Car insurance rates for cars | $133 per month |

| Car insurance rates for SUVs | $118 per month |

| Homeowner's insurance rates | $2,901 for a $200,000 house and $4,693 for a $350,000 house |

| Flood insurance rates | A few hundred dollars per year |

Explore related products

What You'll Learn

![]()

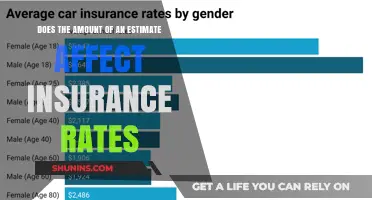

Car insurance rates for different demographics

Car insurance rates vary across different demographics, with age and gender being two key factors. In Summerville, South Carolina, car insurance rates are higher than the state and national averages, with drivers paying around $185.25 per month compared to the national average of $167.23. Summerville's high population density and accident frequency are believed to contribute to these higher rates.

Age

Age is a significant factor in determining car insurance costs, with younger drivers typically paying more. Sixteen-year-olds face the highest monthly premiums, with rates of $436 for females and $478 for males. The difference in rates between genders is most pronounced during the teenage years, with sixteen-year-old males paying approximately $495 more annually than females due to higher accident rates. As drivers age, the gender gap narrows, and by age 25, the difference in rates between genders becomes minimal. For instance, at age 60, both males and females pay an average of $94 per month.

Gender

In most states, gender is considered when determining car insurance premiums. While men are generally perceived to engage in riskier driving behaviour, this does not necessarily result in higher premiums. On average, men pay more annually than women across all ages due to higher teen and senior premiums. However, in six states, including California, Hawaii, and Massachusetts, gender is not permitted to influence insurance rates.

Other Factors

In addition to age and gender, several other factors can impact car insurance rates. These include driving history, claims history, location, vehicle type, credit history, and the types of coverage purchased. Maintaining a clean driving record, bundling insurance policies, and leveraging life changes, such as marriage and improved credit scores, can help reduce insurance costs.

Clark Howard's Guide to Auto Insurance Coverage

You may want to see also

Explore related products

![]()

Home insurance rates and their determinants

Home insurance rates are determined by a variety of factors, some relating to the homeowner and some relating to the home itself.

The location of the home is a significant factor in determining insurance rates. Homes in areas prone to natural disasters such as hurricanes, wildfires, or flooding will typically have higher insurance rates. For example, Summerville, South Carolina, has higher insurance rates than the state average due to its proximity to the coast and the increased risk of hurricanes. Similarly, homes in cities tend to be more expensive to insure than those in suburban or rural areas, as they are generally more expensive to build. The specific neighbourhood and proximity to emergency services, such as fire stations, can also influence rates.

The age and physical structure of the home are also important considerations. The cost of rebuilding or repairing a home is a significant factor in insurance rates. Insurers will consider the age of the home, the condition of major systems (HVAC, plumbing, electrical), the roof age and condition, the building materials used, and the square footage. The presence of certain features, such as a pool or a trampoline, can also increase rates due to the increased risk of injury.

The homeowner's credit score and claims history can also impact insurance rates. A higher credit score typically results in lower premiums, as it indicates a lower likelihood of filing a claim. Conversely, a lower credit score can lead to higher rates. Additionally, filing multiple claims can cause insurance premiums to increase, as it demonstrates a higher risk of future claims. Marital status can also influence rates, with married couples often receiving lower rates due to a lower probability of filing claims.

Other factors that can influence home insurance rates include the home's proximity to water sources or flood zones, local building costs and inflation, and the presence of certain dog breeds or exotic animals. Overall, home insurance rates are a calculation of risk, and insurers will assess various factors to determine the likelihood of a claim being filed.

Medical Payments and Subrogation: Unraveling the Complexities

You may want to see also

Explore related products

![]()

Golf cart insurance and its influencing factors

Summerville, South Carolina, has a higher insurance rate than the state and national averages. The average cost of car insurance in Summerville is $240 per month, compared to the state average of $218 and the national average of $150. The city's high population density and accident frequency are believed to be the main factors contributing to this. Summerville is the seventh-largest city in South Carolina and recorded 1,535 collisions in 2021, the most recent data available, which equates to 4.2 collisions per day.

Golf cart insurance is a type of coverage that provides liability protection for injuries and damage caused while driving a golf cart, as well as damage to the cart itself. The cost of golf cart insurance varies depending on several factors, including the insurer, the type of cart, and how it is used. Here are some key influencing factors:

Type of Golf Cart

The type of golf cart being insured can impact the cost of insurance. For example, if the golf cart is speed-modified, the insurance cost may be higher, with estimates ranging from $60 to $120 per month. Additionally, if the golf cart is classified as a low-speed vehicle (LSV), it may be subject to different regulations and requirements, such as mandatory equipment like lamps, reflectors, and seat belts.

Usage of Golf Cart

The way a golf cart is used can also affect insurance costs. If the golf cart is used exclusively off-road, the insurance cost may be lower, and it may be covered under ATV insurance. On the other hand, if the golf cart is driven on public roads, it may be considered a second car by the state's DMV, resulting in higher insurance costs, similar to those of a regular vehicle.

Location and Regulations

The location where the golf cart is used and the local regulations can influence insurance requirements and costs. Some states and homeowners' associations (HOAs) may require golf cart insurance or low-speed vehicle insurance. Additionally, golf courses or communities with many golf cart drivers may have specific rules and requirements for insurance coverage.

Insurer and Coverage Options

Different insurance providers will offer varying rates for golf cart insurance. The cost can depend on the specific coverage options selected, similar to those in an auto insurance policy. These can include bodily injury, property damage, comprehensive, collision, uninsured motorist, and medical payments coverage.

Safety Features and Driving Record

Similar to car insurance, the safety features of the golf cart and the driving record of the owner can impact insurance costs. Golf carts with better safety features may be eligible for discounts on insurance premiums. Additionally, a clean driving record can result in lower insurance rates, while a history of claims or accidents may increase the cost of insurance.

In summary, golf cart insurance costs can vary based on a combination of factors related to the cart itself, the location and usage, the insurance provider, and the individual owner. It is important to consider the specific circumstances and research the applicable regulations and coverage options to make an informed decision about golf cart insurance.

Spouse Insurance: Auto Exclusion in Georgia

You may want to see also

Explore related products

![]()

State laws and their impact on insurance rates

State laws have a significant impact on insurance rates, and this is reflected in the wide variation of insurance premiums across different states. While each state has its own unique set of laws and requirements, certain factors stand out as having a more pronounced effect on insurance rates.

One notable example is the impact of severe weather conditions in certain states. For instance, Florida experiences severe weather, heavy traffic, congested roadways, and a high number of uninsured motorists, resulting in higher insurance rates. Similarly, Summerville, South Carolina, is prone to hurricanes due to its proximity to the coast, which contributes to higher homeowners insurance rates in the area.

State laws regarding the factors that insurance companies can consider when setting rates also play a crucial role. Some states, like California, Hawaii, Michigan, and Massachusetts, are more restrictive and prohibit insurers from using certain personal characteristics or economic factors to determine rates. For instance, California has banned the use of gender in setting car insurance rates. In contrast, other states may allow insurers to consider factors such as gender, age, credit history, and education level, which can result in higher rates for certain individuals.

Additionally, state regulations can influence the frequency and magnitude of rate increases by insurance companies. For example, in Iowa, the state insurance division regulates insurance rates and premiums, ensuring they are fair and compliant with state laws. Consumers in Iowa are protected from unfair practices related to the use of credit scores by insurance companies, as insurers are required to disclose their use of credit information and allow customers to request a review if they believe their credit score has been unfairly affected.

The level of coverage required by state law also impacts insurance rates. For instance, states that mandate full coverage car insurance policies tend to have higher average insurance rates. On the other hand, states with lower minimum coverage requirements may have more affordable insurance options.

Finally, state laws can influence the competitiveness of the insurance market, impacting the availability of discounts and the variation in rates between different insurance providers. States with more stringent regulations may have a more standardized range of rates, while states with fewer restrictions may experience wider discrepancies in pricing between companies.

Understanding Auto Insurance Deductibles: The Standard or the Exception?

You may want to see also

![]()

Car insurance quotes from various companies

Car insurance rates are determined by a variety of factors, including the driver's age, gender, location, driving history, claims history, and the type of car they drive. Quotes can vary significantly between different insurance providers, so it is important to compare rates from multiple companies to ensure you get the best deal.

There are several companies that allow you to compare car insurance quotes from various providers, such as The Zebra and Insurify. These companies partner with numerous insurers to provide you with real-time quotes based on your personal information and vehicle details. By using these services, you can easily find the most affordable and suitable policy for your needs.

For example, The Zebra partners with over 100 companies and allows you to compare quotes side by side, helping you find the best value for your money. Similarly, Insurify partners with 120+ insurers and provides impartial information and accurate quotes to assist you in choosing the best insurance company for your specific requirements. Insurify has the highest rating on Trustpilot and the Better Business Bureau, ensuring a reliable and trustworthy experience.

In addition to comparison platforms, you can also obtain quotes directly from insurance companies' websites or apps. For instance, Liberty Mutual offers a mobile app that simplifies the process of obtaining a car insurance quote. By providing your information and vehicle details, you can receive a customized quote tailored to your specific circumstances.

It is worth noting that car insurance rates in Summerville, SC, tend to be higher than the state and national averages. The average monthly cost of car insurance in Summerville is $240, compared to the state average of $218 and the national average of $150. This may be influenced by factors such as the city's high population density and frequent accidents. Therefore, it is especially important for residents of Summerville to compare quotes from multiple insurers to find the most affordable coverage.

Aetna Insurance Plans: Auto-Renewal and What to Expect

You may want to see also

Frequently asked questions

Car insurance rates in Summerville, South Carolina, depend on various factors, including the driver's age, the vehicle's value, safety features, and overall safety rating, driving history, and claims history.

The average cost of car insurance in Summerville is $240 per month, higher than the state average of $218 and the national average of $150. However, rates can vary significantly depending on individual circumstances.

Yes, Summerville's proximity to the coast and its exposure to hurricanes, storms, and flooding contribute to higher homeowners insurance rates compared to the state average. The average cost of homeowners insurance in Summerville is about $2,901 for a $200,000 house and $4,693 for a $350,000 house.