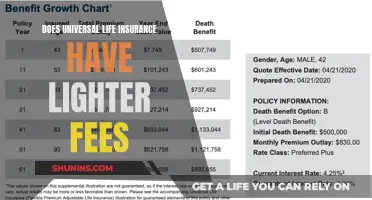

Ulcerative colitis is a chronic inflammatory bowel disease that affects many people. It can cause abdominal pain, diarrhoea, and fatigue, but it does not lead to early death. However, people with this condition often face an increased risk of long-term disability and an inability to work. This can make it challenging to find affordable life insurance coverage, but it is not impossible. The evaluation process for life insurance applications typically involves insurance underwriters reviewing several factors related to the applicant's health and the specifics of their condition. These factors include the current health status, the extent of colon involvement, the time since diagnosis, prescribed treatments, and any complications. The underwriters also take into account other risk factors such as age, gender, and lifestyle habits. Based on their assessment, they determine the applicant's risk class, which, in turn, determines the cost of the insurance policy.

Explore related products

What You'll Learn

- How does ulcerative colitis affect life insurance premiums?

- What happens when you apply for life insurance with ulcerative colitis?

- What are the best life insurance companies for people with ulcerative colitis?

- Can people with ulcerative colitis qualify for disability benefits?

- What are the symptoms of ulcerative colitis?

![]()

How does ulcerative colitis affect life insurance premiums?

Having ulcerative colitis can make it more challenging to get life insurance, but it is not impossible. The condition will likely affect the cost of your insurance premiums, and the extent to which it does will depend on a variety of factors.

Insurance underwriters will review your application closely and take into account several factors related to your ulcerative colitis and overall health. These include:

- Current Health Status: How well is your condition managed?

- Extent of Colon Involvement: Which areas of your colon are affected?

- Time Since Diagnosis: How long have you had ulcerative colitis?

- Prescribed Treatments: What medications or therapies are you on?

- Complications: Have you experienced any issues like bleeding or inflammation?

- Colonoscopy Results: What did your latest colonoscopy reveal?

In addition to your medical history, underwriters also consider other risk factors such as age, gender, lifestyle habits, and tobacco or alcohol use.

Based on their assessment, the underwriter will determine what type of coverage you can get and how much you will pay for it. You will be placed into a "risk class" that determines the cost of your insurance policy. The healthier you are, the lower your premiums are likely to be.

For example, if you have had ulcerative colitis for a prolonged period but have not required treatment for several years, and your recent colonoscopy results are normal, you may qualify for a lower premium. On the other hand, if you have frequent flare-ups, are on multiple medications, or have had recent surgeries or hospitalizations due to ulcerative colitis, your premiums are likely to be higher.

It is important to note that different insurance companies have different underwriting guidelines and processes for setting rates. Therefore, it is advisable to compare quotes from multiple insurers to find the best coverage options and rates for your specific situation.

Life Insurance and Pregnancy Loss: What Coverage is Offered?

You may want to see also

Explore related products

$14.89 $19.99

$23.95

![]()

What happens when you apply for life insurance with ulcerative colitis?

When applying for life insurance with ulcerative colitis, the insurance company will assess your overall risk. Ulcerative colitis is a pre-existing condition, and while it is not life-threatening, it does increase your risk of developing other medical conditions.

The insurance company will consider many factors during the application process, including your age, height, weight, date of diagnosis, family history, and lifestyle habits such as tobacco or alcohol use. They will also want to know about the specifics of your condition, such as:

- The type of ulcerative colitis you have (ulcerative proctitis or proctosigmoiditis)

- The severity and frequency of your symptoms

- Any medications you are taking

- Any complications or treatments you have had, such as surgery or hospitalisation

- The results of any diagnostic tests, such as blood tests, stool samples, or colonoscopies

Based on this information, the insurance company will determine your risk class, which will affect the cost of your insurance policy. You may be placed in a preferred class if your condition is well-controlled and you are in good overall health. However, if you have more severe ulcerative colitis or other risk factors, you may be placed in a sub-standard class and pay higher premiums.

It is important to be honest during the application process and to shop around for the best rates, as costs can vary significantly between insurance companies. While ulcerative colitis may make it more challenging to obtain life insurance, it is not impossible, and there are steps you can take to improve your chances of obtaining coverage.

Life Insurance: Personal Property Protection or Separate Policy?

You may want to see also

Explore related products

![]()

What are the best life insurance companies for people with ulcerative colitis?

While it is challenging to find life insurance coverage with ulcerative colitis, it is not impossible. The cost of coverage for those with ulcerative colitis may be higher than average, and the options available may be more limited. However, there are still several insurance companies that offer coverage for people with this condition.

AIG (American General)

AIG is one of the carriers that offer life insurance for people with ulcerative colitis. They will assess your application based on various factors, including your age, height, weight, date of diagnosis, family history, and tobacco use.

Prudential Life Insurance

Prudential Life Insurance is another option for people with ulcerative colitis. They will also consider multiple factors during the underwriting process, and their rates may differ from those offered by other carriers.

Quotacy

Quotacy is an independent broker that has access to the policy and pricing of many different top-rated insurance companies. They can help you find the insurer that will treat you most favourably and offer you the best coverage options.

Cura Insurance

Cura Insurance is a specialist high-risk insurance adviser dedicated to helping everyone get the insurance they need. They can assist you in finding life insurance, critical illness cover, income protection, and travel insurance.

EffortlessInsurance.com

EffortlessInsurance.com provides a free life insurance comparison tool that allows you to compare quotes from top companies and find the best coverage for your budget and personal needs.

PinnacleQuote

PinnacleQuote is an independent agent that can guide you through the process of obtaining life insurance with ulcerative colitis. They emphasise the importance of obtaining coverage while your condition is under control and being honest on your application.

New York Life Insurance: Converting Term Policies

You may want to see also

Explore related products

$4.99 $19.99

![]()

Can people with ulcerative colitis qualify for disability benefits?

Ulcerative colitis is a type of inflammatory bowel disease (IBD) that affects the colon (large intestine) and rectum. Common symptoms include diarrhoea (sometimes with blood), loss of bowel control, an urgency to defecate, rectal bleeding, abdominal cramping and pain, and involuntary weight loss.

Yes, people with ulcerative colitis can qualify for disability benefits. The Social Security Administration (SSA) considers ulcerative colitis a disability that qualifies for benefits if it interferes with a person's ability to work. To qualify, applicants must meet one or both of the following criteria:

- Obstruction of the small intestine or colon requiring hospitalisation for intestinal decompression or surgery. This must have occurred at least twice, with each occurrence taking place at least 60 days apart within a consecutive six-month period.

- Experience at least two of the following within a consecutive six-month period, despite receiving treatment:

- Low serum albumin (hypoalbuminemia)

- Clinically documented abdominal mass causing pain or cramping that does not respond to prescribed medication

- Perineal disease with a draining abscess or fistula

- Involuntary weight loss of at least 10% of baseline weight

- Need for supplemental nutrition through a gastrostomy or central venous catheter

Additionally, people with ulcerative colitis may be eligible for other disability benefits, such as parking permits, tax credits, and Medicaid or Medicare to help pay healthcare bills.

Life Insurance and Long-Term Disability: What's the Deal?

You may want to see also

Explore related products

![]()

What are the symptoms of ulcerative colitis?

Ulcerative colitis is an inflammatory bowel disease that affects the colon and rectum. The symptoms of this condition can vary in severity and may flare up and go away at different times.

The main symptoms of ulcerative colitis are:

- Recurring diarrhoea, which may contain blood, mucus, or pus

- Needing to defecate frequently

- Extreme tiredness (fatigue)

- Loss of appetite

- Weight loss

Some people with ulcerative colitis also experience symptoms elsewhere in their bodies, known as extra-intestinal symptoms. These can include:

- Painful and swollen joints (arthritis)

- Swollen fat under the skin, causing bumps and patches (erythema nodosum)

- Irritated and red eyes

- Problems with bones, such as osteoporosis

In addition, ulcerative colitis can cause eye inflammations (episcleritis, anterior uveitis), inflammation of the bile ducts (primary sclerosing cholangitis), inflammation of the rectum (proctitis), leg rash (erythema nodosum), mouth ulcers (aphthous ulcers), and painful joints (acute arthropathy).

The severity of symptoms depends on how much of the rectum and colon are inflamed and how severe the inflammation is. For some people, ulcerative colitis significantly impacts their everyday lives.

Does Guaranteed Issue Life Insurance Offer Cash Value?

You may want to see also

Frequently asked questions

Yes, it is possible to get life insurance if you have ulcerative colitis. However, it may be more expensive and you may have to pay substandard or higher-than-average rates.

Many insurers accept applications from people with ulcerative colitis. However, it depends on the severity of your symptoms and the medication/treatment you are using. If you have regular symptoms and are using stronger medication, your cover may be accepted at non-standard terms (premium increase).

Insurers will typically want to know when you were diagnosed, how regular your flare-ups are, what medication you are taking, whether you are able to work, and if you have had or are due to have surgery.

The coverage options available to you may be influenced by your ulcerative colitis diagnosis. Some insurance companies may offer standard policies with no exclusions, while others may impose exclusions related to the condition or charge higher premiums.

To improve your chances, provide accurate and detailed information about your condition and treatment history, maintain regular medical check-ups and follow your treatment plan, and shop around and compare quotes from different insurance providers.