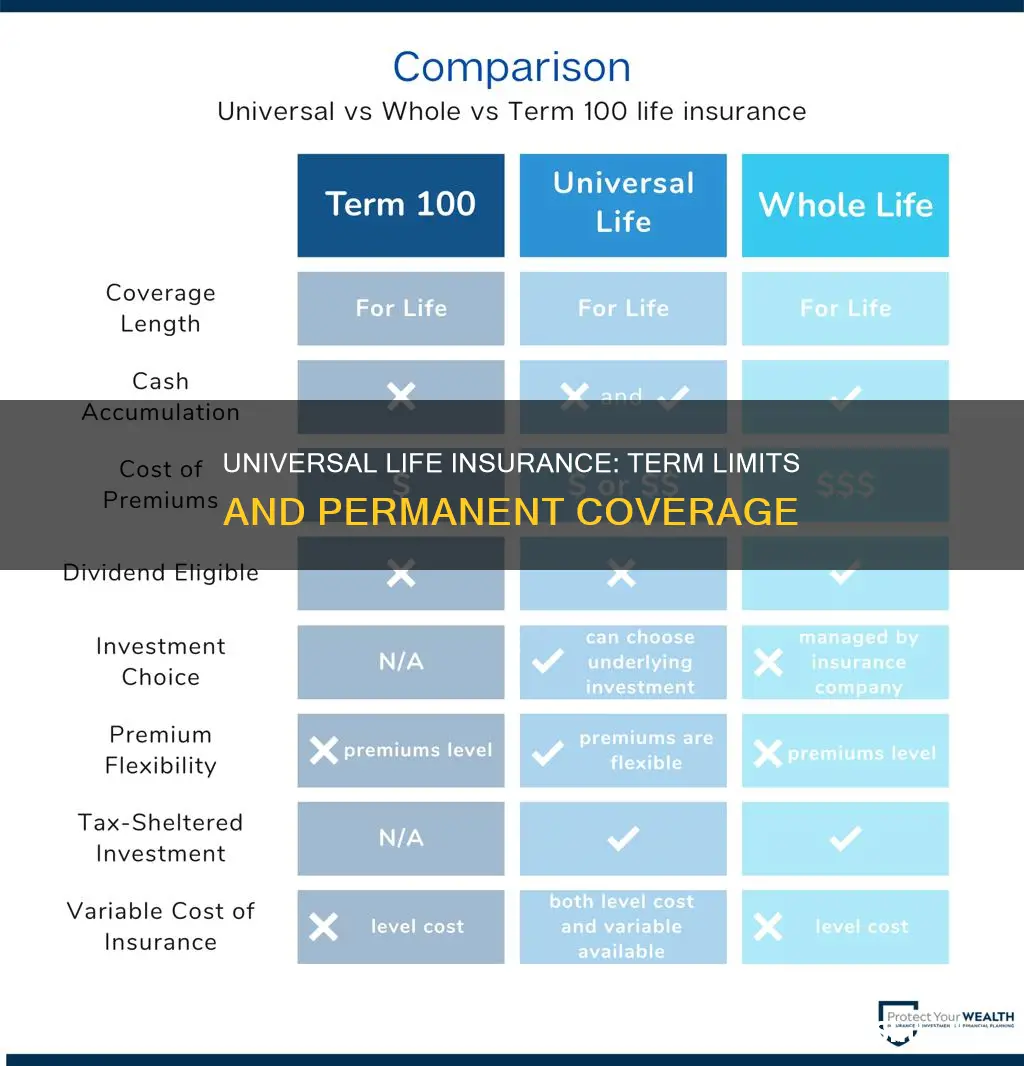

Universal life insurance is a type of permanent life insurance that can provide lifetime protection and build cash value with tax advantages. It is a long-term insurance option that offers flexible coverage and premiums. On the other hand, term life insurance is a more basic type of life insurance that provides coverage for a specific period, such as 10 or 20 years. It is more affordable but lacks the cash value component and has a set end date.

| Characteristics | Values |

|---|---|

| Type of coverage | Permanent, lifelong coverage |

| Term | No set end date |

| Premium payments | More expensive |

| Cash value | Yes |

| Premium flexibility | Yes |

| Premium adjustments | Yes |

| Premium payment frequency | Monthly or annually |

| Premium payment amounts | Adjustable |

| Death benefit | Yes |

| Death benefit flexibility | Yes |

Explore related products

What You'll Learn

- Universal life insurance is a type of permanent coverage that lasts for the policyholder's lifetime

- Universal life insurance has a savings component, or cash value, that can be accessed for other purposes

- Universal life insurance offers flexible premiums and death benefits

- Universal life insurance policies are designed to last until the policyholder's death

- Universal life insurance is more expensive than term life insurance

![]()

Universal life insurance is a type of permanent coverage that lasts for the policyholder's lifetime

Universal life insurance is a type of permanent coverage that lasts for the policyholder's entire lifetime. It is designed to provide lifelong protection and is one of the most common types of life insurance.

Universal life insurance is distinguished by its flexibility. It allows the policyholder to adjust the amount and frequency of premium payments (within limits) and even increase or decrease the policy's coverage. This flexibility means that universal life insurance can be tailored to meet an individual's changing financial goals and circumstances.

Universal life insurance also has a savings component, often referred to as its cash value. This cash value accumulates over time on a tax-deferred basis and can be accessed by the policyholder during their lifetime. This feature makes universal life insurance a useful tool for building wealth and meeting complex financial needs. The cash value can be used to cover emergency expenses, supplement retirement income, or pay for other expenses.

Universal life insurance is a good option for those seeking long-term coverage and the ability to customise their coverage. It is also well-suited to those with complex financial needs who want to take advantage of the policy's cash value for wealth accumulation.

Compared to term life insurance, universal life insurance premiums are significantly more expensive. However, this higher cost is offset by the fact that universal life insurance provides permanent coverage and includes a cash value component.

Life Insurance: Exploring Unique Characteristics and Features

You may want to see also

Explore related products

![]()

Universal life insurance has a savings component, or cash value, that can be accessed for other purposes

Universal life insurance is a type of permanent life insurance that offers flexible coverage and lifelong protection. It is designed to provide coverage for the entire life of the policyholder and can be a good option for those seeking long-term coverage. One key feature that sets universal life insurance apart from other types of life insurance is its savings component, often referred to as the cash value. This savings component offers several benefits and provides policyholders with additional financial flexibility.

The cash value of universal life insurance policies grows over time, and this growth occurs on a tax-deferred basis. This means that policyholders can accumulate substantial savings without having to pay taxes on the growth until they withdraw the money. The cash value can be accessed by the policyholder during their lifetime, providing a source of funds for various purposes. For example, it can be used to cover emergency expenses, supplement retirement income, or even pay for unexpected costs.

The ability to access the cash value gives policyholders more control over their finances and can provide peace of mind in the event of unforeseen circumstances. It is important to note that accessing the cash value will typically reduce the death benefit of the policy. However, this reduction is usually proportionate to the amount withdrawn, ensuring that the policy remains in force as long as sufficient cash value is maintained.

Universal life insurance policies offer flexibility in terms of premium payments and death benefits. Policyholders can choose to increase their death benefit by paying higher premiums or reduce their premiums by agreeing to a smaller death benefit. This flexibility allows individuals to adjust their coverage according to their changing financial circumstances and goals.

In summary, universal life insurance provides not only lifelong protection but also a valuable savings component. The cash value of these policies can be accessed by the policyholder for a variety of purposes, offering financial flexibility and security. However, it is important for individuals to carefully consider their needs and seek professional advice when deciding between different types of life insurance, as each type has its own unique advantages and disadvantages.

Life Insurance and Stillbirth: What Coverage is Offered?

You may want to see also

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UL320_.jpg)

![]()

Universal life insurance offers flexible premiums and death benefits

Universal life insurance is a type of permanent life insurance that offers flexible premiums and death benefits. It provides coverage for the policyholder's lifetime and has a savings component, called the cash value, which the policyholder can access for other purposes. The cash value grows over time on a tax-deferred basis, and the policyholder can borrow against it without tax implications, although some withdrawals may be taxed. The interest rate on the cash value is set by the insurer and can change frequently, but there is usually a minimum guaranteed rate.

The main advantage of universal life insurance is its flexibility. Policyholders can adjust their premiums and death benefits to some extent. The premiums can be increased or decreased within certain limits, which may be helpful for those with fluctuating incomes. The death benefit can also be adjusted, although this may require a medical exam. Universal life insurance also offers long-term coverage for a lower premium than other permanent life insurance policies.

However, there are some disadvantages to universal life insurance. It requires the policyholder to actively monitor the policy to ensure it remains properly funded. If the cash value becomes too low, the policy may lapse, and the policyholder may have to make large payments to keep the coverage. Additionally, the returns on the cash value are not guaranteed and can be affected by interest rates. While there is a minimum guaranteed interest rate, policyholders may not see the growth they had hoped for if interest rates drop.

Overall, universal life insurance can be a good option for those seeking permanent coverage, flexible premiums, and the potential for cash value growth. However, it is important to carefully consider the pros and cons before purchasing this type of insurance.

Personal Life Insurance: Protecting Your Family's Future

You may want to see also

Explore related products

![]()

Universal life insurance policies are designed to last until the policyholder's death

Universal life insurance is a type of permanent life insurance, which means it is designed to last for the lifetime of the policyholder. Unlike term life insurance, which provides coverage for a fixed period, such as 10, 20, or 30 years, universal life insurance offers lifelong protection. This type of insurance is ideal for those seeking long-term coverage and peace of mind, knowing that their loved ones will be financially protected in the event of their death.

Universal life insurance policies offer flexible coverage, allowing policyholders to adjust their premiums and death benefits to a certain extent. This flexibility is particularly useful for those with varying income levels or changing financial needs over time. The policy accumulates a cash value that can be accessed by the policyholder during their lifetime to cover emergency expenses or supplement retirement income. This cash value grows over time on a tax-deferred basis, providing an additional savings component to the policy.

It is important to note that universal life insurance premiums are typically more expensive than term life insurance premiums. However, the higher cost is due to the lifelong coverage and the cash value component of the policy. Universal life insurance is suitable for those who require lifelong coverage and prefer the added benefit of a flexible premium and death benefit.

When deciding between term and universal life insurance, it is essential to consider your financial goals, premium affordability, and the duration of coverage needed. Term life insurance is generally more affordable and provides coverage for a specified period, making it ideal for those with limited budgets or specific coverage needs. On the other hand, universal life insurance offers lifelong coverage, a savings component, and flexible premiums, making it a good choice for those with complex financial needs and a preference for long-term protection.

Insurers' Investment Risk: Whole Life Insurance Explained

You may want to see also

Explore related products

![]()

Universal life insurance is more expensive than term life insurance

On the other hand, universal life insurance is a type of permanent life insurance, or cash value insurance. It provides coverage for the lifetime of the policyholder. Universal life insurance also has a savings component, or cash value, that builds up over time on a tax-deferred basis. This cash value can often be accessed and used towards other expenses. Due to its permanent nature and the inclusion of a savings component, universal life insurance premiums are significantly more expensive than term life insurance.

The main advantage of term life insurance is its affordability. It is a good option for those who only need coverage for a specified time period and want it to be as cost-effective as possible. Term life insurance is also suitable for those who want the most affordable coverage, especially if they are young and healthy. Additionally, term life insurance can be converted into permanent coverage if needed.

Universal life insurance, on the other hand, offers flexible coverage and premiums. It is suitable for those who want permanent life insurance that can last for their lifetime and provide a way to accumulate cash value with a flexible premium. Universal life insurance is ideal for those who want long-term coverage and are willing to monitor their policy periodically with their agent or financial professional. It is also a good choice for older individuals looking to convert their term insurance policy to longer-term coverage.

In summary, while universal life insurance offers permanent coverage, a savings component, and flexible premiums, it comes at a significantly higher cost compared to term life insurance. Term life insurance, with its affordability, fixed coverage period, and guaranteed death benefit, is a more suitable option for those seeking cost-effective coverage for a specific period.

Life Insurance and Taxes: What's the Government's Cut?

You may want to see also

Frequently asked questions

Universal life insurance is a type of permanent life insurance that offers flexible coverage and lifelong protection. It also has a cash value component that grows over time, which policyholders can access for other purposes.

Term life insurance is the most basic type of life insurance. It provides coverage for a specific period, such as 10 or 20 years, and is more affordable than universal life insurance. Term life insurance policies do not accrue a cash value.

Universal life insurance premiums are flexible and remain the same throughout the policy, while term life insurance premiums are not flexible and typically increase as the policyholder ages. Additionally, universal life insurance provides lifelong coverage, whereas term life insurance has a predefined duration.

The choice between universal and term life insurance depends on individual needs and preferences. If you require lifelong coverage, have complex financial needs, or want to enhance your estate planning, universal life insurance may be more suitable. On the other hand, if you have a smaller budget, need coverage for a specific period, or prefer simplicity, term life insurance could be a better option.