Washington state residents have seen insurance rates climb steeply over the past few years. While the state's insurance rates are still lower than the national average, there are concerns about affordability. There are several factors contributing to the rise in insurance costs, including the increased frequency and severity of auto accidents, the soaring cost of cars, and the impact of climate-related disasters such as wildfires. Additionally, factors such as age, gender, driving record, and credit score can also influence insurance rates for individuals in Washington.

| Characteristics | Values |

|---|---|

| Car insurance rates in Washington | Rising |

| Home insurance rates in Washington | Rising |

| Factors for rising car insurance rates | Increase in car accidents, increase in serious crashes, rise in cost of cars, inflation, increase in cost of vehicle repairs, increase in cost of living, increase in cost of home rebuilding, increase in cost of claims |

| Average cost of car insurance in Washington | $1,285 per year |

| Average cost of car insurance for young drivers in Washington | $2,481 per year |

| Average cost of car insurance for senior drivers in Washington | $1,693 per year |

| Average cost of full coverage car insurance in Washington | $1,347 per year |

| Average cost of minimum coverage car insurance in Washington | $688 per year |

| Average cost of car insurance for 17-year-old drivers in Washington | PEMCO Mutual has rates below the statewide average |

| Average cost of car insurance for young adult drivers in Washington | USAA has the lowest rates |

| Companies that offer cheap car insurance in Washington | PEMCO Mutual, USAA, Geico, State Farm, Travelers |

| Companies that offer cheap car insurance for teen drivers in Washington | State Farm, Travelers, Geico, USAA, American Family |

| Ways to get cheaper car insurance in Washington | Compare quotes from different companies, choose a higher deductible, improve your credit score, drive safely, use apps that measure your driving habits and provide discounts for safe driving |

Explore related products

What You'll Learn

- Car insurance rates in Washington are higher than the national average

- Repair costs, crime, traffic, and weather influence insurance rates

- Age, gender, and driving record impact insurance costs

- Vehicle repairs, safety equipment, and technology increase insurance prices

- Wildfires and climate-related disasters are causing insurers to rethink underwriting

![]()

Car insurance rates in Washington are higher than the national average

Car insurance rates in Washington have been rising and are higher than the national average. While the national average annual cost of full coverage car insurance is $2,680, the average cost in Washington is $1,347, about 4% higher than the national average. The state's minimum coverage costs $688 per year, which is also higher than the national average of $595.

There are several factors contributing to the increase in car insurance rates in Washington. One of the main reasons is the rising cost of vehicle repairs. As safety equipment and technology in cars become more advanced and sophisticated, the cost of fixing them increases. Additionally, there has been a marked increase in the severity of auto accidents, resulting in higher damage to vehicles and more injuries. This has led to higher claims costs for insurance companies, which is reflected in the premiums charged to customers.

Another factor influencing the rise in insurance rates is the cost of cars themselves. The average price of both new and used cars has increased significantly in recent years, which means that insurance companies are facing larger payouts for total losses. Washington's population density and frequent bad weather, which can lead to more accidents, also contribute to higher insurance rates in the state.

Age is another critical factor affecting car insurance premiums in Washington. Younger drivers, particularly those between 17 and 25, are considered higher-risk due to their inexperience and higher accident rates. As a result, they often pay significantly more for car insurance than older drivers.

While Washington's car insurance rates are higher than the national average, they are still more affordable than in some other states. According to industry representatives, Washington is in a "pretty good position" compared to states like California, Florida, and Louisiana, where affordable policies have become increasingly hard to find.

Best Auto Insurance Company in New Jersey: Who's Top?

You may want to see also

Explore related products

![]()

Repair costs, crime, traffic, and weather influence insurance rates

Several factors, such as repair costs, crime, traffic, and weather, influence insurance rates. Washington drivers pay lower average rates than the national average, with $1,901 per year for full coverage and $573 per year for minimum coverage, while the national average annual cost of full coverage car insurance is $2,680.

Repair Costs

The features of a car have a direct influence on the insurance rate. For example, classic cars are generally more expensive to repair and have higher insurance rates. Similarly, hybrid vehicles have higher repair costs due to expensive parts, and advanced safety features in modern cars are complex and costly to repair.

Crime

Crime creates a demand for insurance, and insurers shape the risk and returns to certain crimes. Insurers have been prime supporters of the security industry, creating a demand for burglar alarms and security systems. Insurers can influence the cost of carrying out crimes and the probability of being punished, thereby reducing criminal activity.

Traffic

Traffic violations, such as speeding tickets, can increase insurance premiums, especially if the driver has a history of moving violations. However, some states allow drivers to keep minor infractions off their record by attending traffic school or a driver safety class.

Weather

Weather is a significant factor influencing insurance rates, with climate change leading to more frequent and severe storms, resulting in more costly claims and repairs. Extreme weather events can cause direct damage to vehicles and increase the incidence of accidents, leading to higher insurance premiums.

Understanding Residual Liability Insurance in Auto Policies

You may want to see also

Explore related products

![]()

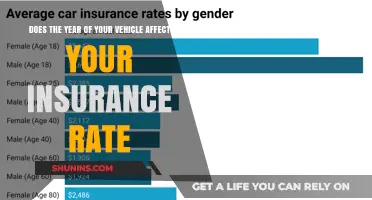

Age, gender, and driving record impact insurance costs

While Washington's insurance rates are lower than the national average, they have been climbing steeply. The primary reasons for this are the increased costs of repairing vehicles and rebuilding homes, with safety equipment and other technology in cars becoming more sophisticated and expensive. Climate-related disasters, such as wildfires, are also causing insurers to rethink underwriting in some regions.

Age, gender, and driving record all impact insurance costs in Washington. Younger drivers, especially those between 16 and 19, tend to pay more for car insurance due to their lack of experience and higher likelihood of engaging in risky behaviour. The high insurance rates for young drivers start to decrease at age 25, with the best rates offered to those in their 50s and early 60s, assuming they have a good driving record. After this, rates begin to increase again from around age 65.

In Washington, a driving mistake can increase insurance rates by 8.8% above the yearly average. At-fault accidents, speeding tickets, and DUIs all contribute to higher insurance costs. A spotless driving record helps to secure lower insurance rates, as insurers perceive these individuals as low-risk drivers.

Gender is also a factor in determining insurance rates, with women often paying less than men. However, as drivers age and gain more experience, the gender gap narrows, and rates become more similar. In some age groups, women even pay slightly more than men, but this difference is negligible compared to the rates paid by younger drivers.

Auto Liability Insurance: A Must-Have for Many Jobs

You may want to see also

Explore related products

![]()

Vehicle repairs, safety equipment, and technology increase insurance prices

Car insurance rates in Washington have been rising. While the state's insurance rates are still lower than the national average, consumers are feeling the pressure from rising insurance prices.

There are several factors contributing to the increase in insurance prices. One of the main reasons is the rising cost of vehicle repairs, which is driven by the increasing sophistication of safety equipment and technology in modern cars. This includes advanced safety systems, such as adaptive headlights, sensors that help detect pedestrians, and automatic emergency braking. While these features help prevent accidents and improve road safety, they also make repairs more expensive. The sensors, computers, and high-tech equipment required for these safety features can significantly increase the cost of repairing or replacing damaged parts.

In addition to the cost of the parts themselves, the specialized knowledge and training needed to repair and calibrate these advanced systems can also drive up repair costs. As a result, insurance companies may pass on these increased costs to consumers in the form of higher premiums.

Another factor contributing to rising insurance prices is the overall increase in the cost of cars. The average price for both new and used cars has climbed significantly in recent years, which in turn affects the cost of insurance. Additionally, the frequency and severity of auto accidents can impact insurance rates. As the number of serious crashes and injuries increases, the cost of claims that insurance companies have to pay out also rises, leading to higher premiums for consumers.

While safety features and technology can lead to higher insurance rates due to repair costs, it's important to note that insurance companies may offer discounts for certain safety features that help prevent accidents or reduce damage. However, the impact of these discounts may not be significant enough to offset the higher sticker price of cars with advanced safety features. Ultimately, the decision to invest in a car with the latest safety equipment and technology should be based on prioritizing safety, rather than solely on potential insurance savings.

Insisting on OEM Parts for Insurance Claims

You may want to see also

Explore related products

![]()

Wildfires and climate-related disasters are causing insurers to rethink underwriting

Insurers are facing challenges due to the increasing costs of disasters, with climate change intensifying the impact of hurricanes, wildfires, and floods. The California Department of Insurance reported a 10% increase in insurers refusing to renew policies in areas affected by wildfires in recent years. Additionally, major insurers like Allstate and State Farm have scaled back their home insurance businesses in California or halted sales of new policies to avoid paying for wildfire damage.

The rising costs of vehicle repairs and home rebuilding, driven by inflation and technological advancements, are also contributing to the increase in insurance rates. Insurers are reassessing their risk tolerance to maintain financial stability and profitability, which is affecting the availability and affordability of insurance policies.

In Washington state, residents have experienced steep increases in home and auto insurance rates. While the state is in a better position compared to others, such as California and Florida, consumers are feeling the pressure from rising insurance prices. Homeowner rates among the top 20 companies in Washington increased by 21.7% year-over-year as of December 1, while auto rates climbed by 17.5%. These hikes are attributed to factors such as the increasing cost of cars and a rise in the number of severe accidents.

To address these challenges, insurers are turning to new tools and technologies. For example, US tech company ClimaCell now offers a wildfire prediction product that analyzes temperature, humidity, and wind in real time. Additionally, Allianz Re is working on adding wildfires to an interactive hazard map that already includes floods, tornadoes, and storms. These tools will help underwriters assess risks more accurately and set appropriate premiums.

How F Endorsement Impacts Your Insurance Rates

You may want to see also

Frequently asked questions

Yes, insurance rates in Washington have been climbing. While the national average annual cost of full coverage car insurance is $2,680, Washington's average is $1,347, about 4% higher than the national average.

There are several factors that contribute to higher insurance rates in Washington. Firstly, the cost of repairing vehicles has increased due to the rising sophistication of safety equipment and technology. Secondly, the frequency of accidents and the severity of damage have increased, resulting in higher claims for insurance companies. Additionally, the cost of cars in Washington has increased, with the average price of new cars rising by 28% between 2019 and 2023.

Age is a significant factor affecting car insurance premiums in Washington. Younger drivers are considered riskier due to their inexperience and higher accident rates, resulting in higher premiums. On average, 17 to 25-year-olds pay significantly more for insurance than older age groups.

Yes, there are a few strategies to obtain cheaper car insurance in Washington. Firstly, consider comparing quotes from multiple insurance companies and choosing a plan with the appropriate level of coverage for your needs. Secondly, some companies offer programs that tailor rates based on driving habits, providing discounts for safe driving measured through apps. Additionally, married drivers often receive lower rates, so informing your insurer of your marital status may reduce your premium.