Homeowners insurance premiums have been rising sharply in recent years, and this is a growing concern for many. While historically, homeowners insurance bills have risen by about 5% annually, in 2023, homeowners saw an average premium jump of 12%, followed by an additional 6.9% in the first half of 2024. Several factors contribute to these increases, including inflation, rising labor and construction costs, severe weather events, supply chain issues, and individual circumstances. As a result, many homeowners are seeking ways to reduce their premiums or considering switching insurance providers.

| Characteristics | Values |

|---|---|

| Homeowners insurance rates increase every year | Yes |

| Average increase in premiums | 0-7% |

| Factors causing the increase | Inflation, increase in property value, claims, severe weather events, rising cost of building materials, supply chain issues, unfilled jobs, reinsurance, weak regulatory oversight, credit history, location |

| Ways to save on premiums | Bundling insurance policies, going paperless, installing impact-rated roofs or smart home security systems, comparison shopping |

Explore related products

What You'll Learn

![]()

Inflation and rising costs of materials and labour

The construction industry has experienced significant increases in the cost of materials and labour. Between June 2019 and June 2024, construction trade services labour costs rose by 40%, while the cost of construction materials also increased by a similar amount. This has a direct impact on insurance rates, as higher construction costs mean higher premiums. Additionally, severe weather events, such as hurricanes, floods, droughts, and wildfires, have become more frequent and destructive, leading to costly insurance claims and further driving up insurance rates.

The impact of inflation and rising costs is evident in the experience of homeowners. Many people have reported annual increases in their insurance premiums, with some seeing surges of up to $700. The average increase in homeowners insurance premiums was 12% in 2023, followed by an additional 6.9% in the first half of 2024, according to S&P Global Market Intelligence. These increases are significantly higher than the historical average of 5% per year.

To manage the rising costs of homeowners' insurance, some individuals choose to shop around and switch insurance carriers to find more competitive rates. Bundling insurance policies, such as home and auto insurance, can also help reduce overall costs. However, it is important to note that insurance companies have a significant influence on the market, and their aggressive tactics can impact the availability of coverage if regulators limit price hikes too aggressively.

Ikon Pass Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

Claims and claim history

When it comes to claims and claim history, there are several factors that can influence how your homeowners insurance premium changes over time. Firstly, the number of claims you file matters. Multiple claims, especially within a short period, can lead to higher premiums. Insurance companies may view you as a higher-risk customer if you have a history of frequent claims. This indicates to them that you are more likely to file additional claims in the future, resulting in increased premiums.

The type of claim is another crucial factor. Certain types of claims, such as liability claims, tend to result in higher premium increases compared to dwelling or personal property claims. Claims that are easily preventable, like fire damage in the kitchen or water damage, can also cause premiums to jump. On the other hand, catastrophes or events beyond your control, such as natural disasters or a tree falling on your house during a storm, typically do not result in the same level of increase since they are less likely to recur.

The severity and cost of the claim also play a role in premium adjustments. Generally, the higher the claim amount, the more likely your insurance company will raise your premium. Additionally, your personal claims history can impact your rates. If you have an extensive claims history, insurers may consider you a higher-risk client and charge you higher rates.

It's important to note that claims typically remain on your record for a period of time, usually between five to seven years. During this time, your insurance rates may be affected. After this period, your rates should start to stabilise. To access your home's claim history, you can request a Comprehensive Loss Underwriting Exchange (CLUE) report, which details previous claims filed for your property and is used by insurance companies to set rates.

While filing a claim can sometimes lead to higher premiums, it is not always the case. Certain situations and consumer protection laws may prevent insurance companies from raising rates after a claim. These laws vary by state, and some states even prohibit price increases for small claims or weather-related incidents. Therefore, it is beneficial to familiarise yourself with the regulations in your specific state.

Homeowners Insurance: Does It Cover House Leveling?

You may want to see also

Explore related products

![]()

Property value and size

The value and size of a property are key factors in determining the cost of homeowners insurance. The square footage of a home is a significant consideration when calculating insurance quotes. Adding new rooms or extensions, such as a deck, can increase the value of a property and, consequently, the insurance premium.

The cost of repairing or rebuilding a home in the event of damage or loss is a crucial aspect of homeowners insurance pricing. As the size of a property increases, so does the cost of rebuilding or repairing it. This is reflected in the insurance rates, which rise in tandem with the value of the property.

Inflation also plays a role in the increasing cost of homeowners insurance. As inflation rises, insurance companies raise their rates to match the increased cost of replacing a home and its contents. This means that even without any changes or additions to a property, the insurance premium may still increase annually due to inflationary pressures.

Additionally, the cost of construction materials and labour can impact insurance rates. In recent years, there has been a shortage of skilled labour in the construction industry, driving up wages and contributing to higher insurance premiums. The rising cost of building materials, supply chain issues, and severe weather events have also led to increased insurance rates.

It is important for homeowners to regularly review their insurance policies and compare rates from different companies to ensure they are getting the best value for their property insurance.

Assessing Home Value for Insurance

You may want to see also

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

![]()

Natural disasters and severe weather events

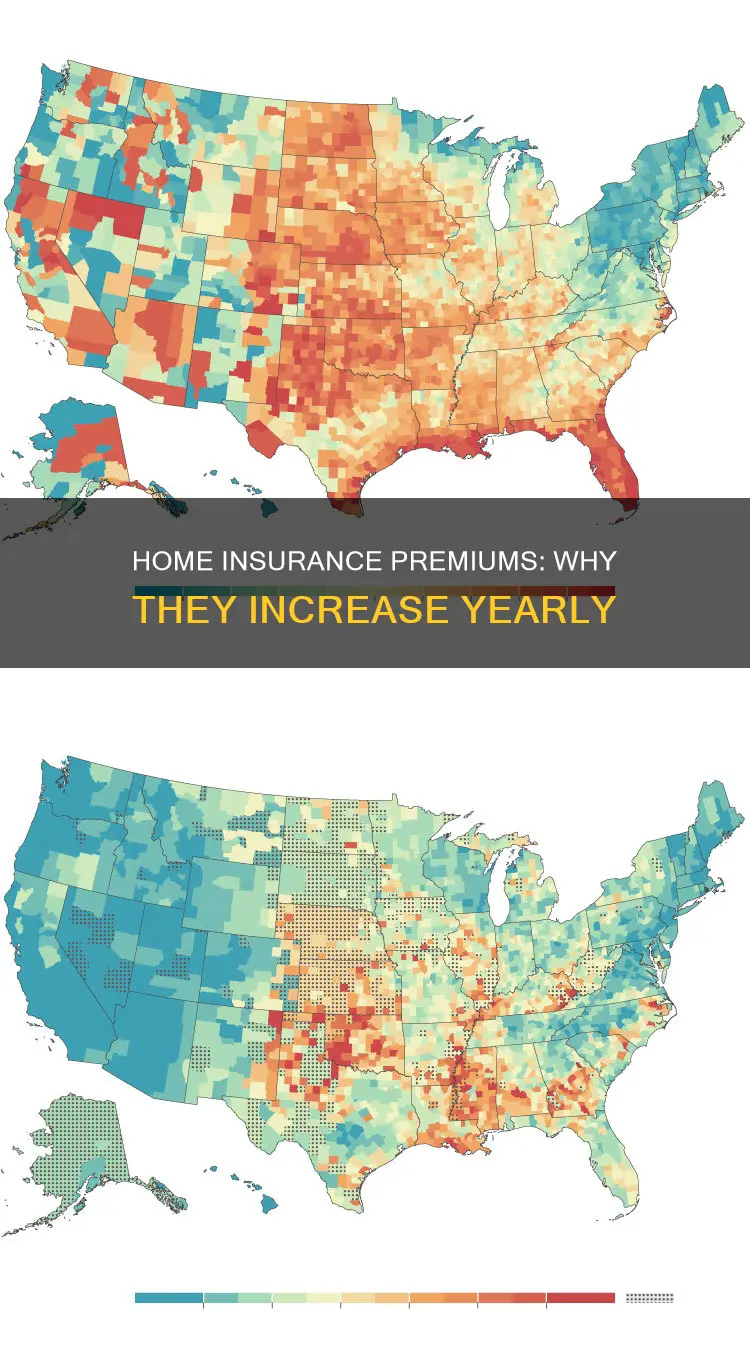

Home insurance premiums are intended to be lower than the cost of rebuilding a home after a disaster. However, as the risk of disasters increases, premiums rise to compensate for the higher likelihood of payouts. Between 2020 and 2023, average home insurance costs in the US rose by 13%, but in areas with the highest disaster risk, the increase was much larger. This trend is expected to continue as the frequency and severity of natural disasters grow.

The type of natural disasters covered by homeowners' insurance varies. Most policies cover damage from wind, hail, lightning strikes, ice, snowstorms, and extreme cold. However, rain damage, flooding, and landslides are generally not covered. Additionally, in locations prone to severe windstorms or hail, additional coverage may be required. Separate coverage may also be needed for disasters such as earthquakes and wildfires.

The impact of natural disasters on insurance rates can vary depending on the location. Homeowners in high-risk areas may pay more than those in lower-risk regions, even within the same state. The migration of the US population towards riskier areas has contributed to rising reinsurance rates, which, in turn, has influenced higher premiums for homeowners.

To mitigate the financial burden of natural disasters, homeowners can consider implementing resilient home features. Storm shutters, reinforced roofing, and flood barriers can help lower the risk of damage and reduce premiums. Additionally, elevating water heaters and electrical panels and installing fortified roofing can provide protection against flooding and fires.

VSP Eye Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![Life Insurance Lottery [DVD]](https://m.media-amazon.com/images/I/717EhWE0rqL._AC_UL320_.jpg)

![]()

Credit history and financial performance

Homeowners insurance rates are influenced by a variety of factors, one of which is credit history and financial performance. Insurance companies use credit-based insurance (CBI) scores to evaluate an individual's credit history and calculate premiums. While similar to a FICO credit score, CBI scores are calculated differently by each insurer, and they are only one part of how homeowners insurance rates are determined.

The two biggest factors in determining a CBI score are previous credit performance and the amount and type of outstanding debt. For example, a $200,000 mortgage is weighed differently from $200,000 in credit card debt. Insurers use CBI scores to predict the likelihood of an individual filing a claim, with those who have higher scores seen as less likely to file a claim.

A person with poor credit may be viewed as a higher risk by insurance companies and may face higher premiums. In some cases, individuals with poor credit may pay more than double the home insurance rates of those with good credit. Additionally, those with poor credit may find it challenging to secure a home insurance policy, as insurers may consider them a significant risk.

However, it is important to note that credit history is not the only factor influencing homeowners insurance rates. Other factors, such as location, the type of home, and claims history, also play a role in determining premiums. Furthermore, individuals with poor credit can take steps to improve their credit score, such as paying bills on time, reducing debt, and disputing errors on their credit report. By improving their credit score, individuals may be able to obtain more affordable homeowners insurance rates.

In summary, while credit history and financial performance can impact homeowners insurance rates, it is just one of several factors considered by insurance companies. Individuals with poor credit may face higher premiums, but they can also take steps to improve their credit score and potentially reduce their insurance costs.

Geico: Home Insurance Options in North Carolina

You may want to see also

Frequently asked questions

There are several reasons why homeowner's insurance may increase annually. Firstly, insurance companies raise rates in response to inflation, as your home and belongings become more expensive to replace. Secondly, severe weather events, such as hurricanes, floods, droughts, and wildfires, have become more frequent and destructive, leading to costly insurance claims and subsequent rate adjustments. Finally, individual factors, such as filing a claim, increasing your property's value, or changes to your credit history, can also contribute to higher premiums.

Typically, homeowner's insurance premiums should increase slightly each year, ranging from 0% to 7%. However, in recent years, homeowners have experienced more significant jumps, with average increases of 12% in 2023 and an additional 6.9% in the first half of 2024. These increases have outpaced inflation in several U.S. states.

To manage rising insurance costs, consider the following strategies:

- Shop around and compare rates from different insurance companies.

- Bundle your insurance policies (e.g., home and auto) with the same provider to take advantage of potential discounts.

- Opt for paperless billing and pay your premium in full to save on fees.

- Install impact-rated roofs or smart home security systems, which may help reduce your premium.

- Consult an insurance specialist or broker to find the best offer without compromising your coverage needs.