Car insurance rates typically increase after an accident, but the extent of the increase depends on several factors, including the type of accident, the driver's state, their insurance company, and their driving record. Accidents that are not the driver's fault may still increase insurance rates, as insurers believe that drivers involved in not-at-fault accidents are more likely to be involved in future accidents. To mitigate the impact of an accident on insurance rates, drivers can consider investing in accident forgiveness, taking a defensive driving course, or shopping for a new insurance provider.

| Characteristics | Values |

|---|---|

| Whether insurance goes up after an accident | Yes, but the amount varies depending on the company and state |

| Average increase in insurance rates | 48% to 60% |

| Highest increase in insurance rates | 61% (Geico, Nationwide, and AAA) |

| Lowest increase in insurance rates | 15% (State Farm) |

| Factors that affect the increase in insurance rates | Type and severity of the claim, driving record, insurance company, location, age, claims history, car make and model |

| Accident forgiveness | Offered by some companies for minor accidents or the first accident |

| Loss of discounts | Yes, loss of claim-free discount and other associated discounts |

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

What You'll Learn

![]()

At-fault accidents

An accident will almost always raise your insurance rate, especially if you are at fault. The amount your insurance goes up depends on several factors, including your insurance company, the state you live in, the car you drive, the severity of the collision, and whether the accident was your fault.

In some states, insurance companies are prohibited from raising rates after a not-at-fault accident. However, even if you are not at fault, your costs could go up, as insurers may see this as an indication that you are more likely to be in future accidents.

The impact of an at-fault accident on your insurance rate can vary. NerdWallet's analysis found that full coverage car insurance rates can go up by an average of 48% a year if you cause an accident. The average cost of car insurance increases by $872 per year after an at-fault accident. However, some companies may offer lower rates, and shopping around and comparing quotes can help you find the lowest rate.

The length of time an accident remains on your record also varies by state and insurer. Typically, a claim will remain on your record for three to five years. After a certain number of years, your insurance company will stop charging you for the accident.

Some insurance companies offer accident forgiveness, which means your insurance rate won't go up after your first at-fault accident. This can be included in a standard policy or purchased as a separate rider.

Pizza Insurance: Delivery Protection

You may want to see also

Explore related products

![]()

Accident forgiveness

The exact nature of accident forgiveness varies. Some companies may forgive your first accident for free, while others may not raise your premium for an accident if the damage is under a certain dollar amount. Some companies also offer different tiers of accident forgiveness, such as small and large accident forgiveness, which may depend on the size of your claim.

It is important to note that accident forgiveness may not be available in all states, and eligibility can vary by insurer. Additionally, not everyone is eligible for accident forgiveness, as it is usually only available to drivers with a spotless driving history.

Winter Storage: Insuring Your Vehicle

You may want to see also

Explore related products

![]()

Driving record

A driver's insurance rate is influenced by their driving record. A history of accidents and traffic violations can lead to an increase in insurance rates, as insurers consider such incidents as indicators of higher risk. The more violations a driver has, the higher the likelihood of filing a claim, resulting in a rate increase. Even a minor moving violation ticket can contribute to a higher insurance rate.

At-fault accidents almost always result in higher insurance rates. In certain states, insurers may not increase premiums if the damage is below a certain monetary value. Accidents that are not the driver's fault may still cause insurance rates to rise, depending on the state and insurer. Not-at-fault accidents can indicate a higher likelihood of future accidents, and insurers may use data showing a propensity for such incidents to justify rate increases.

The impact of accidents on insurance rates can vary depending on the state and insurance provider. An accident may remain on a driving record for several years, influencing insurance rates during that time. After a certain period, typically at least three years, an accident will no longer affect insurance premiums, provided the driver maintains a clean record.

Accident forgiveness programs offered by some insurers can help prevent rate increases after certain types of accidents, such as minor incidents or a driver's first accident. These programs may be included as loyalty perks or purchased as optional add-ons. However, accident forgiveness is usually only available to drivers with a spotless driving history.

In addition to accident history, other factors that can influence insurance rates include age, location, claims history, car make and model, and changes in the driver's address or vehicle. Insurance rates typically increase when a policy is renewed rather than immediately after a change in rating factors.

Accounting Firms: Insured or Not?

You may want to see also

Explore related products

![]()

Insurance company policies

Accidents that are not your fault may still increase your insurance rate, depending on your state and insurer, as insurers have data showing that some drivers have a propensity for not-at-fault accidents. In general, insurance companies look back at several years of your driving history when determining your car insurance rate. The amount of time an accident remains on your driving record, which can be used to determine your car insurance rate, may vary by your state and insurer.

Some insurance companies offer accident forgiveness programs, so your rates won't increase after certain types of accidents, like your first accident or smaller accidents. For example, Progressive offers accident forgiveness for claims totalling less than $500. Accident forgiveness is sometimes included in your rates as a loyalty perk, but with most companies, you can include it in your policy for a small surcharge. However, accident forgiveness is usually only available to drivers with a spotless driving history.

After an accident, your insurance rates may increase at the time of policy renewal, rather than immediately. It's worth shopping around for new insurance coverage to see if you can get the same coverage for a lower price.

USLI: An Insurance Carrier?

You may want to see also

Explore related products

![]()

Location and age

The cost of car insurance is influenced by a variety of factors, including age and location.

Location

The location of the insured individual is a significant factor in determining car insurance rates. Insurers consider factors such as crime rates, accident history, and population density in specific locations. For example, urban areas with higher crime rates and crowded roads tend to have higher insurance premiums compared to rural areas with lower crime rates and less congested roads. Additionally, changes in address or ZIP code can lead to fluctuations in insurance rates, as certain locations may experience increases in claims or repair costs over time.

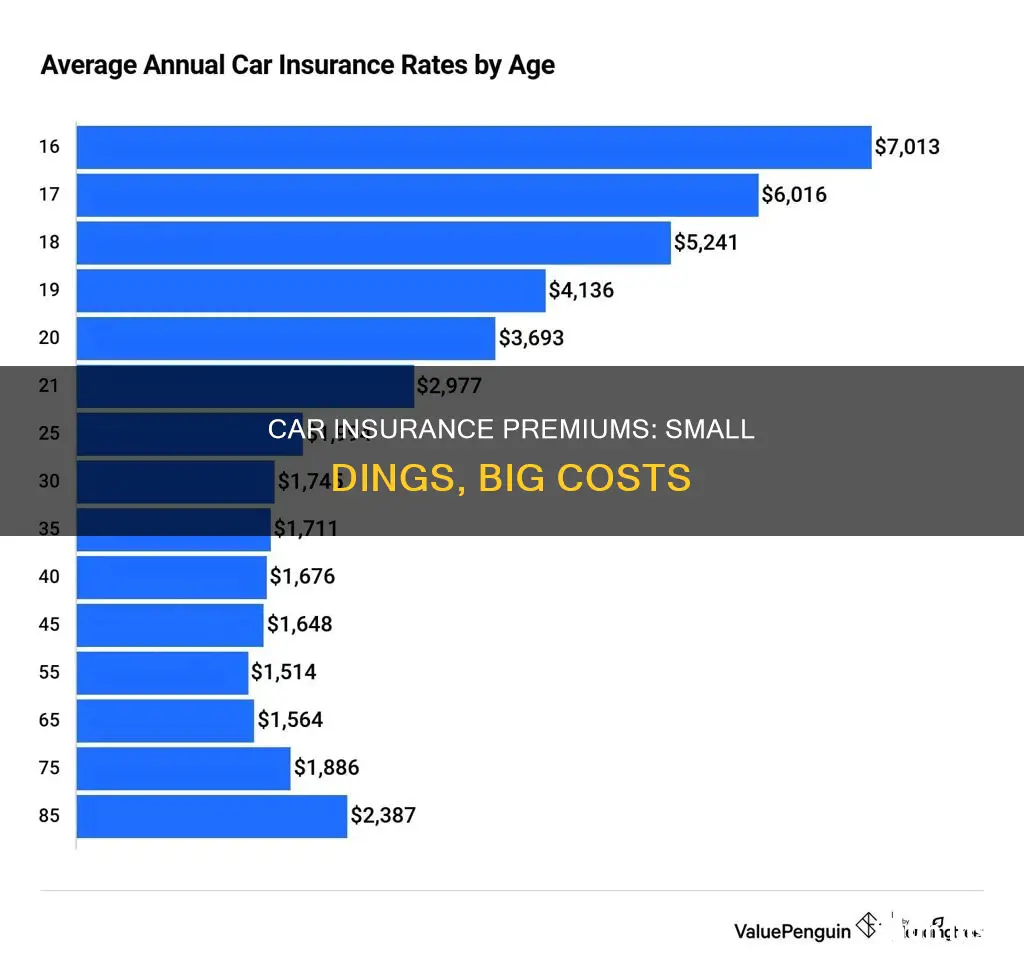

Age

Age also plays a crucial role in determining car insurance premiums. Younger drivers, especially teenagers, often face higher insurance rates due to their higher risk of car crashes and fatal accidents. This risk perception results in higher premiums for younger drivers compared to older age groups. On the other hand, drivers in their mid-70s and beyond may also experience an increase in insurance rates, as insurers may consider them riskier than middle-aged adults. However, age-based discounts may be available from certain insurers or states to mitigate these increases.

Mobile Device Insurance: Worth the Cost?

You may want to see also

Frequently asked questions

Yes, insurance rates typically increase after an accident, especially if you were at fault. The exact amount by which your rates will increase is difficult to predict, and will depend on the severity of the accident, your driving history, and the state you live in.

One way to prevent your rates from increasing is to invest in accident forgiveness. This is an optional policy add-on offered by most major car insurance companies. Accident forgiveness is a guarantee that your rates won't go up after your first at-fault accident. However, not everyone is eligible for accident forgiveness, as it is usually only available to drivers with a spotless driving history.

There are several factors that can cause insurance rates to increase, including your location, age, claims history, driving record, car make and model, and changes to your address or vehicle. Additionally, insurance rates may increase due to factors beyond your control, such as an increase in claims in your ZIP code or an increase in car repair/replacement costs.