Navigating the complexities of motor insurance can be daunting, leaving many drivers unsure whether they are adequately covered. The question, Have I got motor insurance? is more than just a query—it’s a critical check to ensure legal compliance, financial protection, and peace of mind on the road. Understanding your policy details, coverage limits, and renewal dates is essential, as gaps in insurance can lead to severe penalties, out-of-pocket expenses, or even legal consequences. Whether you’re a seasoned driver or a new policyholder, verifying your motor insurance status is a proactive step toward responsible vehicle ownership.

| Characteristics | Values |

|---|---|

| Service Name | Have I Got Motor Insurance (UK) |

| Purpose | Allows users to check if a vehicle is insured |

| Provider | Motor Insurers' Bureau (MIB) |

| Website | askMID.com |

| Accessibility | Free to use for UK residents |

| Information Required | Vehicle registration number (VRN) |

| Data Source | Motor Insurance Database (MID) |

| Coverage | All insured vehicles in the UK |

| Update Frequency | Real-time (reflects current insurance status) |

| Limitations | Does not provide policy details (e.g., coverage type, insurer name) |

| Legal Use | Helps verify insurance compliance for law enforcement and individuals |

| Mobile App | Not available (web-based only) |

| Privacy | Compliant with UK data protection laws |

| Launch Date | 2005 (as part of MID initiatives) |

| Related Services | Continuous Insurance Enforcement (CIE) scheme |

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

What You'll Learn

- Coverage Types: Liability, comprehensive, collision, and personal injury protection explained

- Policy Limits: Understanding maximum payouts for damages and injuries

- Premiums & Costs: Factors affecting insurance rates and payment options

- Claims Process: Steps to file a claim and required documentation

- Legal Requirements: Minimum insurance mandates by state or country

![]()

Coverage Types: Liability, comprehensive, collision, and personal injury protection explained

When it comes to motor insurance, understanding the different coverage types is essential to ensure you have the right protection for your vehicle and yourself. The four primary coverage types are liability, comprehensive, collision, and personal injury protection (PIP), each serving a distinct purpose. Liability insurance is typically the minimum requirement by law in most states and covers costs associated with injuries or damages you cause to others in an accident. This includes medical expenses, property damage, and legal fees if you’re sued. It does not, however, cover your own injuries or vehicle repairs, making it crucial to pair it with other coverage types for complete protection.

Comprehensive insurance steps in for damages to your vehicle that occur outside of collisions, such as theft, vandalism, natural disasters, or hitting an animal. This coverage is particularly valuable if you live in an area prone to severe weather or high crime rates. While it’s not legally required, it’s often recommended for drivers who want to safeguard their investment in their vehicle, especially if it’s newer or financed. Keep in mind that comprehensive coverage typically comes with a deductible, which is the amount you pay out of pocket before the insurance kicks in.

Collision insurance specifically covers repairs to your vehicle after an accident, regardless of who is at fault. This includes collisions with other vehicles, objects like fences or trees, or even rollovers. Like comprehensive coverage, collision insurance usually requires a deductible. It’s particularly important for drivers with newer or more expensive cars, as repair costs can be substantial. However, if your vehicle is older and its value is low, you may want to weigh the cost of the premium against the potential benefits.

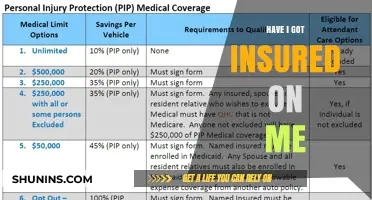

Personal injury protection (PIP) is designed to cover medical expenses for you and your passengers after an accident, regardless of fault. This can include hospital bills, rehabilitation costs, and even lost wages due to injuries. PIP is mandatory in some states, known as "no-fault" states, where it ensures quick payment of medical expenses without the need to determine who caused the accident. Even in states where it’s optional, PIP can be a valuable addition to your policy, especially if you lack comprehensive health insurance.

Understanding these coverage types allows you to tailor your motor insurance policy to your specific needs. For instance, a driver with an older car might opt for liability and PIP but skip comprehensive and collision to save on premiums. Conversely, a driver with a new, financed vehicle would benefit from a full suite of coverages to protect their asset. Always review your policy carefully and consult with an insurance agent to ensure you’re adequately protected without overpaying for unnecessary coverage.

Life Insurance CLU: What to Check and How

You may want to see also

Explore related products

![]()

Policy Limits: Understanding maximum payouts for damages and injuries

When you purchase motor insurance, one of the most critical aspects to understand is your policy limits. These limits define the maximum amount your insurance company will pay out for damages and injuries resulting from an accident. Policy limits are typically divided into two main categories: liability coverage and comprehensive/collision coverage. Liability coverage is further split into bodily injury liability and property damage liability. Bodily injury liability covers the medical expenses, lost wages, and other costs associated with injuries to others involved in an accident that you are found responsible for. Property damage liability, on the other hand, covers the repair or replacement costs of the other party’s vehicle or property. Understanding these limits is essential because if the costs exceed your policy limits, you may be personally responsible for the difference.

For example, if your bodily injury liability limit is $50,000 per person and $100,000 per accident, and you cause an accident where one person incurs $75,000 in medical bills, your insurance will only cover up to $50,000. The remaining $25,000 would be your financial responsibility. Similarly, if the property damage liability limit is $25,000 and you cause $35,000 worth of damage to someone else’s vehicle, you would need to pay the additional $10,000 out of pocket. This is why it’s crucial to choose policy limits that adequately protect your financial assets, considering factors like your net worth and the potential risks you face on the road.

Comprehensive and collision coverage also have policy limits, but they work differently. Comprehensive coverage pays for damages to your vehicle caused by events other than collisions, such as theft, vandalism, or natural disasters. Collision coverage, as the name suggests, covers damages to your vehicle resulting from a collision, regardless of who is at fault. The limits for these coverages are typically based on the actual cash value (ACV) of your vehicle, which is its current market value minus depreciation. If your car is totaled, the insurance company will pay out up to the ACV, not the original purchase price or replacement cost. This means that if your car is older or has depreciated significantly, the payout may not be enough to replace it with a similar vehicle.

It’s also important to consider additional coverage options that can provide extra protection beyond your standard policy limits. For instance, uninsured/underinsured motorist coverage can help if you’re involved in an accident with a driver who has insufficient or no insurance. Personal injury protection (PIP) or medical payments coverage can help cover your own medical expenses, regardless of who is at fault. Umbrella insurance is another option that provides additional liability coverage above your standard policy limits, offering greater financial protection in case of a severe accident.

Finally, when reviewing your motor insurance policy, take the time to carefully assess your policy limits and ensure they align with your needs. If you’re unsure about the appropriate limits, consult with your insurance agent or broker. They can help you evaluate factors like your driving habits, the value of your assets, and the potential risks you face to determine the right level of coverage. Remember, while higher policy limits generally mean higher premiums, they also provide greater peace of mind and financial security in the event of a serious accident. Understanding and choosing the right policy limits is a key step in ensuring you have adequate motor insurance protection.

Life Insurance: Your Ultimate Financial Safety Net

You may want to see also

Explore related products

![]()

Premiums & Costs: Factors affecting insurance rates and payment options

Understanding the factors that influence your motor insurance premiums is crucial for managing costs effectively. Insurance rates are not one-size-fits-all; they are calculated based on a variety of risk factors that insurers use to determine the likelihood of you making a claim. One of the primary factors is your driving history. If you have a record of accidents, traffic violations, or claims, your premiums are likely to be higher because insurers perceive you as a higher risk. Conversely, a clean driving record can lead to lower rates and even discounts. Additionally, the type of vehicle you drive plays a significant role. High-performance cars, luxury vehicles, and models with a high theft rate generally cost more to insure due to increased repair costs or higher risk of loss.

Another critical factor affecting premiums is your personal profile. Insurers consider your age, gender, and location when calculating rates. Younger, less experienced drivers, particularly those under 25, often face higher premiums due to statistically higher accident rates. Similarly, living in an area with high crime rates or heavy traffic can increase your insurance costs. Your annual mileage is also taken into account; the more you drive, the greater the risk of an accident, which can lead to higher premiums. Some insurers offer discounts for low mileage or usage-based policies that track your driving habits to provide more personalized rates.

The level of coverage you choose directly impacts your premiums. Comprehensive insurance, which covers a wide range of incidents including theft, vandalism, and natural disasters, is more expensive than third-party-only or third-party, fire, and theft policies. Additionally, your excess amount—the sum you agree to pay toward a claim—affects your premium. Opting for a higher excess can lower your premium, but it’s important to ensure you can afford the excess in case of a claim. Payment options also play a role in overall costs. Many insurers offer monthly payment plans, but these often include interest or fees, making the total cost higher than paying annually upfront.

Discounts and savings opportunities can help reduce your premiums. Insurers frequently offer discounts for safe driving, completing advanced driving courses, or installing security features like alarms or immobilizers in your vehicle. Bundling policies, such as combining your motor insurance with home or life insurance from the same provider, can also lead to significant savings. Some insurers provide discounts for loyal customers or for paying premiums annually rather than monthly. It’s worth reviewing these options to maximize your savings.

Finally, it’s essential to regularly review and compare insurance policies to ensure you’re getting the best value. Premiums can vary widely between insurers, and your circumstances may change over time, affecting your rates. Shopping around during renewal periods or after significant life changes, such as moving to a new area or purchasing a different vehicle, can help you find more affordable coverage. Understanding these factors and actively managing them can make motor insurance more cost-effective and tailored to your needs.

Life Insurance: Deny, Not a Luxury but a Necessity

You may want to see also

Explore related products

![]()

Claims Process: Steps to file a claim and required documentation

When filing a motor insurance claim, understanding the process and having the necessary documentation ready can significantly streamline the experience. The first step is to notify your insurance provider as soon as possible after the incident. Most insurers have a dedicated claims hotline or online portal for this purpose. Provide them with your policy number, details of the accident (including date, time, location, and a brief description), and information about any third parties involved, such as their names, contact details, and vehicle registration numbers. Prompt notification ensures the insurer can begin processing your claim without delay and helps prevent potential complications.

The second step involves gathering and submitting the required documentation. This typically includes a completed claim form, which your insurer will provide. You’ll also need a copy of your driver’s license, vehicle registration, and proof of insurance. If the claim involves an accident, a police report is often mandatory, especially if there are injuries or significant property damage. Additionally, photographs of the accident scene, vehicle damage, and any visible injuries can provide valuable evidence to support your claim. If there are witnesses, their statements or contact information should also be included.

Once your insurer receives your claim and supporting documents, they will assess the details to determine coverage and liability. This may involve an investigation, which could include inspecting your vehicle, reviewing medical records (if applicable), and contacting third parties or witnesses. During this stage, it’s important to cooperate fully with your insurer and provide any additional information they request. If your claim is approved, the insurer will outline the next steps, which may include arranging repairs, providing a rental vehicle, or processing compensation for damages or injuries.

The final step is resolution and settlement. If your vehicle requires repairs, your insurer may work directly with an approved repair shop, or they may reimburse you for the costs. For total loss claims, the insurer will typically pay the agreed-upon value of the vehicle. If the claim involves medical expenses or personal injury, the insurer will handle these according to your policy’s terms. Throughout the process, keep detailed records of all communications, expenses, and documentation related to your claim. This ensures transparency and helps resolve any potential disputes efficiently.

In some cases, you may need to pay a deductible before the insurer covers the remaining costs, as outlined in your policy. Understanding your policy’s terms, including coverage limits and exclusions, is crucial to managing expectations during the claims process. If you encounter difficulties or have questions at any stage, don’t hesitate to contact your insurer’s claims department for clarification. Being proactive, organized, and informed will help ensure a smoother claims experience and a quicker resolution.

Brightway Insurance: Life Insurance Options and Offerings

You may want to see also

Explore related products

![]()

Legal Requirements: Minimum insurance mandates by state or country

When it comes to motor insurance, understanding the legal requirements is crucial to ensure compliance with the law and avoid penalties. Legal Requirements: Minimum insurance mandates by state or country vary significantly, as each jurisdiction sets its own rules to protect drivers, passengers, and pedestrians. In the United States, for example, every state has its own minimum liability insurance requirements. These typically cover bodily injury and property damage liability, ensuring that if you are at fault in an accident, the injured party’s medical expenses and property repairs are covered up to the policy limits. For instance, California requires drivers to carry at least $15,000 for injury or death to one person, $30,000 for injury or death to multiple people, and $5,000 for property damage. It’s essential to verify your state’s specific requirements, as failing to meet these mandates can result in fines, license suspension, or even legal action.

Outside the United States, Legal Requirements: Minimum insurance mandates by state or country also differ widely. In the United Kingdom, for example, it is illegal to drive a vehicle without at least third-party insurance, which covers damages to others and their property but not the driver’s own vehicle. This is a strict requirement, and driving without it can lead to severe penalties, including hefty fines, license points, or vehicle seizure. Similarly, in Canada, each province and territory has its own minimum insurance standards, often including liability coverage and accident benefits. For instance, Ontario requires $200,000 in third-party liability coverage, while Quebec mandates a minimum of $50,000. Understanding these regional differences is vital for drivers who travel across borders or relocate.

In Europe, the European Union has standardized certain aspects of motor insurance to facilitate cross-border travel. The Legal Requirements: Minimum insurance mandates by state or country within the EU include compulsory third-party liability insurance, which covers damage caused to others in the event of an accident. This is enforced through the EU’s Motor Insurance Directive, ensuring that all member states adhere to a baseline level of protection. However, individual countries may impose additional requirements. For example, Germany requires drivers to carry a minimum of €100 million in liability coverage, while France mandates €1 million. Non-EU countries like Switzerland and Norway also have their own strict insurance laws, emphasizing the importance of researching local regulations.

In Asia, Legal Requirements: Minimum insurance mandates by state or country vary even more dramatically. In India, for instance, the Motor Vehicles Act requires all vehicles to have at least third-party insurance, which covers liability for death, injury, or property damage to third parties. This is a legal necessity, and driving without it can result in fines and imprisonment. In contrast, Japan requires both compulsory liability insurance and a separate policy called Jidosha Baishou Sekinin Hoken, which covers personal injury and death. Meanwhile, countries like Singapore have a unique system called the Certificate of Insurance, which is mandatory for all vehicles and covers third-party liabilities. These regional variations highlight the need for drivers to familiarize themselves with local laws.

Finally, in Australia, Legal Requirements: Minimum insurance mandates by state or country are determined at the state and territory level, though all jurisdictions require Compulsory Third Party (CTP) insurance, also known as a Green Slip in New South Wales. CTP covers personal injury claims from third parties involved in an accident, but it does not cover property damage or the driver’s own injuries. Some states, like Victoria, include CTP insurance as part of the vehicle’s registration fee, while others require drivers to purchase it separately. Additionally, while not mandatory, many drivers opt for comprehensive or third-party property insurance for broader coverage. Failing to meet these requirements can result in registration cancellation or legal consequences, underscoring the importance of staying informed about local insurance laws.

Insurance Proceeds: Income or Not?

You may want to see also

Frequently asked questions

You can check your motor insurance status by reviewing your policy documents, contacting your insurance provider directly, or using online tools like the Motor Insurance Database (MID) in the UK.

Driving without motor insurance is illegal in most countries and can result in fines, penalty points on your license, vehicle seizure, or even a driving ban.

It depends on your policy. Some policies include third-party coverage for other drivers, while others may require you to add specific drivers to your policy. Always check your policy details.

Check the expiration date on your policy documents or contact your insurer. You can also verify its validity through the Motor Insurance Database (MID) if available in your region.