Millions of people around the world face the daunting reality of having no health insurance, leaving them vulnerable to financial hardship and limited access to essential medical care. Without the safety net of insurance, individuals often delay or forgo necessary treatments, preventive care, and medications, which can exacerbate health issues and lead to more severe, costly complications over time. The lack of coverage disproportionately affects low-income families, the self-employed, and those in jobs without employer-provided benefits, creating a cycle of health disparities and economic instability. Addressing this issue requires systemic solutions, such as expanding public health programs, reducing healthcare costs, and increasing awareness of available resources to ensure everyone has the opportunity to lead a healthy life.

Explore related products

What You'll Learn

- Affordability Issues: High premiums and out-of-pocket costs make insurance unaffordable for many individuals and families

- Employment Gaps: Losing job-based coverage due to unemployment or part-time work leaves many uninsured

- Eligibility Barriers: Strict income or immigration status requirements exclude people from public health insurance programs

- Lack of Awareness: Many are unaware of available insurance options or enrollment processes, leading to gaps in coverage

- Pre-existing Conditions: Fear of high costs or denial due to health issues discourages some from seeking insurance

![]()

Affordability Issues: High premiums and out-of-pocket costs make insurance unaffordable for many individuals and families

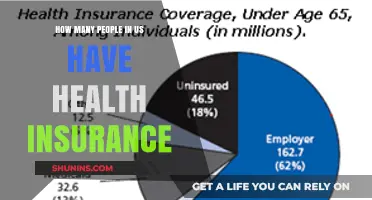

High premiums and out-of-pocket costs force millions to gamble with their health. In 2022, nearly 10% of Americans under 65 lacked health insurance, often due to costs exceeding their budgets. For a family of four, average annual premiums topped $22,000, with employers covering roughly 70%—leaving employees to pay over $6,500 before factoring in deductibles, copays, and coinsurance. For individuals earning near the federal poverty level ($14,580 annually), even subsidized plans under the Affordable Care Act can consume 20-30% of their income, making coverage feel like a luxury rather than a necessity.

Consider the math for a single parent earning $35,000 annually. After taxes, housing, and essentials, their discretionary income might hover around $800 monthly. A mid-tier health plan could cost $300–$400 per month in premiums, plus a $3,000 deductible. One unexpected ER visit or chronic condition could wipe out savings, leading many to forgo insurance entirely. This isn’t recklessness—it’s survival calculus. High-deductible plans, often the cheapest option, delay care until conditions worsen, turning minor issues into costly crises.

Employer-sponsored insurance isn’t a universal safety net. Only 56% of small businesses (under 50 employees) offer health benefits, leaving workers in gig, retail, or service industries to navigate the individual market. Here, premiums spike for older adults or those with pre-existing conditions, despite ACA protections. For example, a 55-year-old in Texas might face premiums exceeding $1,000 monthly for a plan with a $6,000 deductible—an impossible burden for someone earning $50,000. Out-of-pocket maximums, capped at $9,100 for individuals in 2023, offer little comfort when paired with rising prescription costs, like insulin averaging $300–$500 monthly without insurance.

Practical tips for those priced out of traditional insurance:

- Explore Medicaid or CHIP if your income falls below state thresholds (e.g., $18,754 for an individual in most states).

- Use cost-sharing ministries like Liberty HealthShare or Samaritan Ministries, which pool member funds for medical expenses (note: these aren’t insurance and may exclude pre-existing conditions).

- Negotiate medical bills directly with providers—many hospitals offer discounts or payment plans for uninsured patients.

- Visit community health clinics that charge on a sliding scale based on income.

- Leverage prescription discount cards (e.g., GoodRx) to cut medication costs by up to 80%.

The takeaway is clear: affordability isn’t just about lowering premiums—it’s about redesigning a system where “coverage” doesn’t equate to financial ruin. Until out-of-pocket costs align with real incomes, millions will remain uninsured, proving that health care access is still a privilege, not a right.

Top Home Insurance Companies: Protecting Your Property and Peace of Mind

You may want to see also

Explore related products

![]()

Employment Gaps: Losing job-based coverage due to unemployment or part-time work leaves many uninsured

Unemployment doesn’t just mean losing a paycheck—it often means losing health insurance, too. In the U.S., where employer-sponsored insurance covers nearly half the population, job loss can trigger a sudden and devastating gap in coverage. Part-time workers fare little better; many employers exclude them from health benefits altogether. This leaves millions vulnerable, forced to choose between paying for COBRA (which can cost upwards of $700/month for individuals) or going uninsured. For context, a 2022 study found that 40% of unemployed workers lost their insurance within three months of job separation.

Consider the case of Sarah, a 38-year-old marketing professional who was laid off during a corporate restructuring. Her COBRA premium would have consumed 30% of her severance pay, so she opted to go without insurance. Six months later, a routine checkup turned into a $5,000 bill for an unexpected procedure. Stories like Sarah’s highlight the financial peril of employment-linked coverage. Part-time workers face similar risks: a 2021 Kaiser Family Foundation report revealed that only 24% of firms offering health benefits extend them to part-time employees, leaving millions in low-hour roles uninsured.

To navigate this gap, start by exploring alternatives to COBRA. For instance, if your income falls below 400% of the federal poverty level ($54,360 for an individual in 2023), you may qualify for subsidized plans through the Affordable Care Act marketplace. State-specific programs, like California’s Covered California, offer additional discounts. If you’re under 26, consider staying on a parent’s plan. For short-term needs, short-term health plans (averaging $100–$200/month) provide temporary coverage, though they often exclude pre-existing conditions.

However, beware of pitfalls. Short-term plans may not cover essential services like maternity care or mental health treatment. Medicaid, while a lifeline for low-income individuals, has strict eligibility criteria that vary by state—12 states still haven’t expanded Medicaid under the ACA, leaving millions in the "coverage gap." If you’re over 50, factor in higher premiums: the ACA allows insurers to charge older adults up to three times more than younger enrollees. Proactively researching options during a 60-day window post-job loss can prevent lapses in coverage.

The takeaway is clear: employment-based insurance ties health security to job stability, a precarious arrangement in an economy marked by gig work and layoffs. While stopgap solutions exist, they require vigilance and financial trade-offs. Policymakers could ease this burden by decoupling insurance from employment, as seen in countries with universal healthcare systems. Until then, individuals must navigate a fragmented system, balancing cost, coverage, and risk during employment gaps.

Flu Vaccine Medical Insurance: What Code Do You Need?

You may want to see also

Explore related products

![]()

Eligibility Barriers: Strict income or immigration status requirements exclude people from public health insurance programs

In the United States, public health insurance programs like Medicaid and the Children’s Health Insurance Program (CHIP) are designed to provide coverage for low-income individuals and families. However, strict eligibility criteria often create insurmountable barriers. For instance, Medicaid’s income thresholds vary by state, with some requiring applicants to earn less than 138% of the federal poverty level (FPL) to qualify. In states that have not expanded Medicaid under the Affordable Care Act, the cutoff can be as low as 44% of the FPL, leaving millions in the "coverage gap"—earning too much for Medicaid but too little for subsidized private insurance. This disparity highlights how income requirements, though intended to target resources efficiently, exclude those who are marginally above the threshold but still unable to afford healthcare.

Immigration status further complicates access to public health insurance, even for those who meet income criteria. Non-citizens, including lawful permanent residents, often face a five-year waiting period before becoming eligible for Medicaid, regardless of their financial need. Undocumented immigrants are entirely excluded from federal programs, with only a handful of states offering limited coverage for specific services, such as emergency care or pregnancy-related treatment. This exclusion not only affects individuals but also has broader public health implications, as untreated illnesses can spread within communities. For example, a 2020 study found that states with more inclusive Medicaid policies for immigrants had lower rates of uninsured individuals and better overall health outcomes.

Consider the case of Maria, a 35-year-old undocumented worker in Texas, who earns $18,000 annually—below the federal poverty level for a single individual. Despite her low income, she is ineligible for Medicaid due to her immigration status. Private insurance is unaffordable, leaving her to forgo preventive care and rely on emergency rooms for urgent needs. This scenario illustrates how income and immigration requirements intersect to create a double bind, trapping individuals like Maria in a cycle of limited access and higher healthcare costs.

To address these barriers, advocates propose policy reforms such as eliminating the five-year waiting period for lawful permanent residents and expanding Medicaid eligibility to include undocumented immigrants. Practical steps for individuals include exploring state-specific programs, such as California’s Restricted-Scope Medicaid, which covers certain services for undocumented residents, or seeking assistance from community health centers that offer sliding-scale fees. Additionally, organizations like the National Immigration Law Center provide resources to help navigate eligibility rules and advocate for policy changes.

In conclusion, while public health insurance programs aim to reduce uninsured rates, strict income and immigration requirements perpetuate gaps in coverage. By understanding these barriers and exploring alternative solutions, individuals and policymakers can work toward a more inclusive healthcare system that ensures access for all, regardless of income or immigration status.

Battling Insurance: Strategies to Secure Your Medication Coverage

You may want to see also

Explore related products

![]()

Lack of Awareness: Many are unaware of available insurance options or enrollment processes, leading to gaps in coverage

A staggering number of individuals forgo health insurance simply because they don't know it's within reach. This isn't about affordability (though that's a separate issue); it's about a lack of awareness. Many assume insurance is only for the wealthy or employed, unaware of subsidized plans, community health centers, or short-term coverage options. This knowledge gap leaves them vulnerable to financial ruin from unexpected medical emergencies.

Imagine a single mother working two part-time jobs, ineligible for employer-sponsored insurance and unaware of Medicaid expansion in her state. A trip to the emergency room for her child could spiral into debt, all because she didn't know help was available. This scenario isn't hypothetical; it's a reality for millions.

Bridging this awareness gap requires a multi-pronged approach. First, simplify information dissemination. Government websites, often dense and confusing, need to be redesigned with clear, concise language and interactive tools. Imagine a chatbot guiding users through eligibility checks and plan comparisons, or videos explaining enrollment processes in multiple languages. Second, leverage community organizations and trusted figures. Local churches, libraries, and community centers can host workshops and information sessions, reaching populations less likely to seek information online.

Healthcare providers also play a crucial role. During routine visits, doctors and nurses can briefly discuss insurance options and provide resources, ensuring patients understand their coverage choices.

The consequences of inaction are dire. Uninsured individuals delay preventative care, leading to more severe and costly health issues down the line. They're also more likely to forgo necessary medications, exacerbating chronic conditions. This not only impacts individual well-being but also strains the healthcare system as a whole. By addressing the lack of awareness, we can empower individuals to make informed choices, improve health outcomes, and create a more equitable healthcare landscape.

Understanding Medical Insurance Benefits Verification

You may want to see also

Explore related products

![]()

Pre-existing Conditions: Fear of high costs or denial due to health issues discourages some from seeking insurance

The specter of pre-existing conditions looms large for those without health insurance, casting a shadow of fear and uncertainty. Imagine a 45-year-old with well-managed diabetes, diligently taking their 500mg metformin twice daily, yet terrified that this very condition will render them uninsurable or saddled with exorbitant premiums. This fear isn't baseless; historically, insurers could deny coverage or charge astronomical rates for conditions like diabetes, hypertension, or even past mental health struggles. While the Affordable Care Act (ACA) prohibits such discrimination, the lingering anxiety persists, a relic of a bygone era that still deters many from seeking the very protection they need.

This fear manifests in a dangerous cycle. Individuals forgo insurance, avoiding potential denial or high costs, but this leaves them vulnerable to catastrophic expenses should their condition worsen. A routine checkup for a pre-existing heart condition, for instance, could escalate into a costly emergency without preventive care. The irony is stark: the very fear of high costs due to pre-existing conditions leads to behaviors that guarantee those costs will materialize.

Breaking this cycle requires a two-pronged approach. Firstly, education is key. Dispelling myths about pre-existing conditions under the ACA is crucial. Individuals need to understand that insurers cannot deny them coverage or charge more based on their health history. Secondly, exploring options like ACA marketplace plans or state-specific programs can provide affordable coverage tailored to individual needs. For example, a 30-year-old with asthma might qualify for a subsidized plan with a low monthly premium and a deductible that doesn't break the bank.

Ultimately, the fear of pre-existing conditions shouldn't be a barrier to accessing healthcare. By understanding their rights and exploring available options, individuals can break free from this cycle of fear and vulnerability, ensuring they have the protection they need to manage their health effectively.

Double Medical Insurance: Is It Worth the Cost?

You may want to see also

Frequently asked questions

Without health insurance, you face high out-of-pocket costs for medical care, limited access to preventive services, and potential financial hardship in case of emergencies or chronic conditions.

Yes, but you’ll be responsible for the full cost of the visit, which can be significantly higher than insured rates. Some clinics offer sliding-scale fees or payment plans for uninsured patients.

Yes, alternatives include community health centers, government programs like Medicaid (if eligible), prescription assistance programs, and short-term health plans, though these may have limitations.