The question of how many people in the United States have health insurance is a critical issue that reflects the nation's overall well-being and access to healthcare. As of recent data, approximately 91% of Americans are covered by some form of health insurance, a significant increase from previous decades due to policy changes like the Affordable Care Act (ACA). However, this still leaves millions uninsured, with disparities persisting across demographics such as income, age, and geographic location. Understanding these numbers is essential for addressing gaps in coverage and ensuring equitable access to healthcare services nationwide.

Explore related products

What You'll Learn

![]()

Employer-based coverage trends

Employer-based health insurance remains the cornerstone of coverage for millions of Americans, but its landscape is shifting. As of 2023, approximately 158 million people, or about 59% of the insured population, receive health insurance through their employer or a family member’s employer. This dominance, however, is not without challenges. Rising healthcare costs, changing workforce dynamics, and evolving employee expectations are reshaping how employers approach health benefits. For instance, the average annual premium for employer-sponsored family coverage exceeded $22,000 in 2022, with employees contributing nearly $6,000 of that amount. This financial strain has prompted employers to explore cost-sharing strategies, such as high-deductible health plans (HDHPs) paired with health savings accounts (HSAs), which now cover over 30% of workers.

To adapt to these trends, employers are increasingly focusing on value-based care and wellness programs. Companies like Google and Walmart have pioneered initiatives that integrate mental health services, telehealth, and preventive care into their benefits packages. These efforts not only improve employee health but also reduce long-term healthcare costs. For example, a study by the Integrated Benefits Institute found that every dollar invested in wellness programs yields a return of $3.27 in reduced healthcare costs and absenteeism. Small and mid-sized businesses, however, often struggle to implement such programs due to resource constraints, leading to disparities in coverage quality across company sizes.

Another notable trend is the rise of voluntary benefits, which allow employees to customize their coverage based on individual needs. Options like critical illness insurance, hospital indemnity plans, and pet insurance are becoming more common as employers seek to enhance their benefits packages without significantly increasing costs. This flexibility appeals to a diverse workforce, particularly younger employees who prioritize personalized benefits over traditional one-size-fits-all plans. However, this approach also risks creating a patchwork of coverage that may leave some workers underinsured for critical health needs.

Despite these innovations, employer-based coverage faces existential threats from broader policy debates. Proposals like Medicare for All or a public option could reduce reliance on employer-sponsored insurance, though such changes remain politically contentious. In the meantime, employers must navigate a complex environment where attracting and retaining talent hinges on the competitiveness of their health benefits. Practical steps for businesses include benchmarking against industry peers, leveraging data analytics to identify cost drivers, and engaging employees in benefit design decisions. For workers, understanding the nuances of their employer’s plan—such as network restrictions, out-of-pocket maximums, and prescription drug coverage—is essential to maximizing value.

In conclusion, employer-based coverage trends reflect a balancing act between cost containment and employee satisfaction. While the system remains robust, its future will depend on how effectively employers and policymakers address emerging challenges. For now, it remains the primary pathway to health insurance for most Americans, making its evolution a critical area to watch.

Medical Insurance Costs in Jackson, Mississippi: What's the Price?

You may want to see also

Explore related products

![]()

Medicaid enrollment statistics

As of recent data, Medicaid serves as a critical safety net for millions of Americans, covering approximately 83 million individuals as of 2023. This figure represents a significant portion of the U.S. population, particularly those with low incomes, disabilities, or specific medical needs. Understanding Medicaid enrollment statistics is essential for grasping the broader landscape of health insurance coverage in the United States. Unlike private insurance, Medicaid is jointly funded by federal and state governments, with eligibility and benefits varying widely across states. This variability makes enrollment trends both complex and highly informative.

One striking trend in Medicaid enrollment is its responsiveness to economic conditions. During the COVID-19 pandemic, for instance, enrollment surged by over 20 million people due to increased unemployment and expanded eligibility under the Families First Coronavirus Response Act. This temporary growth highlights Medicaid’s role as a countercyclical program, expanding during downturns to support vulnerable populations. However, as economic conditions improve, states face the challenge of unwinding these expansions, a process known as the "unwinding period," which began in April 2023. Early data suggests that millions of individuals are at risk of losing coverage due to procedural disenrollments, raising concerns about access to care.

Geographic disparities in Medicaid enrollment further underscore the program’s complexity. States that expanded Medicaid under the Affordable Care Act (ACA) have consistently higher enrollment rates compared to non-expansion states. For example, in 2023, expansion states like California and New York had enrollment rates above 30% of their populations, while non-expansion states like Texas and Florida lagged significantly, with rates below 20%. These differences directly impact health outcomes, as residents in expansion states have greater access to preventive care and lower uninsured rates. Policymakers and advocates often point to these disparities as evidence of the need for universal Medicaid expansion.

A closer look at demographic data reveals that children and pregnant women represent a substantial portion of Medicaid enrollees, accounting for nearly half of all beneficiaries despite making up a smaller share of the population. This focus on vulnerable populations aligns with Medicaid’s original intent to provide coverage for those most at risk. However, adults without children, particularly in non-expansion states, face significant coverage gaps. For example, in states that have not expanded Medicaid, the median income eligibility threshold for parents is just 41% of the federal poverty level, leaving many low-income adults uninsured. Addressing these gaps requires targeted policy interventions, such as raising income thresholds or adopting alternative coverage models.

Finally, Medicaid enrollment statistics also reflect the program’s cost-effectiveness and long-term benefits. Studies show that Medicaid coverage is associated with improved health outcomes, reduced mortality rates, and lower medical debt. For every dollar spent on Medicaid, states receive an average of $1.64 in federal matching funds, making it a fiscally responsible investment in public health. However, sustaining these benefits requires ongoing commitment to enrollment outreach, streamlined application processes, and adequate provider reimbursement rates. As debates over healthcare reform continue, Medicaid enrollment data remains a vital tool for assessing the program’s impact and identifying areas for improvement.

When to Call Insurance After a Minor Accident in Ohio

You may want to see also

Explore related products

![]()

Uninsured population demographics

The uninsured population in the U.S. is not evenly distributed; certain demographic groups face higher barriers to coverage. Data from the U.S. Census Bureau reveals that as of 2022, approximately 8.5% of Americans, or 28 million people, lacked health insurance. Among these, specific demographics stand out: young adults aged 19–34, low-income individuals, and racial/ethnic minorities, particularly Hispanic and American Indian/Alaska Native populations. For instance, 19.1% of American Indians/Alaska Natives and 18.3% of Hispanics were uninsured, compared to 5.4% of non-Hispanic whites.

Analyzing these disparities highlights systemic issues. Young adults often forgo insurance due to perceived good health and high premiums, while low-income individuals may fall into the "coverage gap" in states that did not expand Medicaid under the Affordable Care Act. For racial/ethnic minorities, historical and structural inequities, such as employment in low-wage jobs without benefits, contribute to higher uninsured rates. Addressing these gaps requires targeted policies, such as expanding Medicaid eligibility and subsidizing premiums for young adults.

To reduce uninsured rates among these groups, practical steps can be taken. Employers can offer affordable health plans tailored to young workers, while states can close the Medicaid coverage gap by adopting expansion. Community health centers can provide culturally competent outreach to minority populations, and federal subsidies can be increased for low-income individuals purchasing insurance on the marketplace. For example, the American Rescue Plan Act of 2021 temporarily increased subsidies, reducing premiums for millions, a model that could be made permanent.

Comparing the U.S. to countries with universal healthcare underscores the urgency of action. In Canada and the UK, uninsured rates are near zero, as coverage is guaranteed regardless of income or employment. While the U.S. system is different, lessons can be drawn from these models, such as the importance of comprehensive public options and equitable access. By focusing on the demographics most at risk, policymakers can make significant strides in reducing the uninsured population and improving health equity.

Understanding Discovery Medical Insurance Coverage and Benefits

You may want to see also

Explore related products

![]()

Affordable Care Act impact

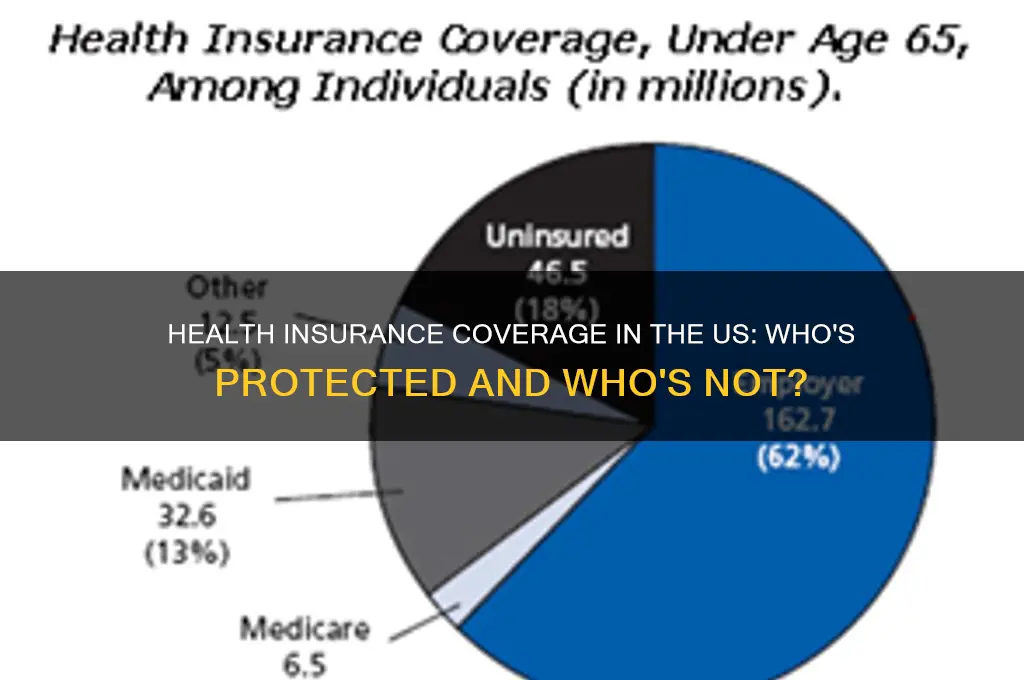

The Affordable Care Act (ACA), often referred to as Obamacare, has significantly reshaped the landscape of health insurance coverage in the United States since its enactment in 2010. One of its most notable impacts is the substantial reduction in the uninsured rate. Before the ACA, approximately 46.5 million non-elderly Americans lacked health insurance in 2010. By 2020, that number had dropped to around 29 million, marking a historic decline. This shift is largely attributed to the ACA’s expansion of Medicaid eligibility, the establishment of health insurance marketplaces, and the introduction of subsidies to make coverage more affordable for low- and middle-income individuals.

Analyzing the ACA’s impact reveals a clear divide in outcomes across states. States that expanded Medicaid under the ACA saw a more dramatic reduction in uninsured rates compared to those that did not. For example, in Kentucky, which embraced Medicaid expansion, the uninsured rate fell from 14.3% in 2013 to 5.8% in 2019. In contrast, states like Texas, which opted out of expansion, experienced slower progress, with uninsured rates remaining above the national average. This disparity underscores the importance of state-level policy decisions in maximizing the ACA’s potential to extend coverage.

From a practical standpoint, the ACA has made health insurance more accessible through its marketplaces, where individuals can compare plans and apply for premium tax credits. For instance, a family of four earning up to $104,800 annually in 2023 may qualify for subsidies, significantly reducing their monthly premiums. Additionally, the ACA’s prohibition on denying coverage due to pre-existing conditions has been a game-changer for millions. Before the ACA, individuals with conditions like diabetes or cancer often faced exorbitant premiums or outright denials, leaving them vulnerable to financial ruin in the event of illness.

However, the ACA’s impact is not without challenges. Critics argue that rising premiums and limited provider networks in some areas have undermined its effectiveness. For example, in rural counties, residents often face fewer plan options and higher out-of-pocket costs. To navigate these issues, consumers should carefully review plan details during open enrollment, paying attention to network coverage and prescription drug formularies. Utilizing resources like Healthcare.gov or state-based marketplaces can help individuals find the best fit for their needs.

In conclusion, the ACA has undeniably expanded health insurance coverage in the U.S., but its success varies by geography and demographic. While it has provided a safety net for millions, ongoing efforts are needed to address remaining gaps and ensure affordability for all. By understanding the ACA’s mechanisms and leveraging available tools, individuals can maximize its benefits and secure the coverage they need.

Medicare and Medicaid: Understanding Social Insurance Programs

You may want to see also

Explore related products

![]()

Private insurance market growth

The private health insurance market in the U.S. has seen steady growth over the past decade, driven by factors such as employer-sponsored plans, rising healthcare costs, and shifting consumer preferences. As of 2023, approximately 180 million Americans are covered by private insurance, accounting for about 55% of the insured population. This growth is not uniform, however. For instance, high-deductible health plans (HDHPs) have surged in popularity, with over 50% of employees in small firms now enrolled in such plans, compared to just 15% in 2010. This shift reflects both employer cost-cutting measures and consumer demand for lower premiums, though it often leaves individuals exposed to higher out-of-pocket expenses.

Analyzing the drivers of this growth reveals a complex interplay of economic and policy factors. The Affordable Care Act (ACA) played a pivotal role by standardizing coverage options and expanding access, but it also spurred private insurers to innovate. For example, the rise of telehealth services, accelerated during the COVID-19 pandemic, has become a key selling point for private plans. Insurers like UnitedHealth Group and Anthem have integrated telehealth into their offerings, attracting tech-savvy consumers and those in rural areas. However, this growth also highlights disparities: while 70% of urban residents have access to telehealth-enabled plans, only 40% of rural residents do, underscoring the market’s uneven expansion.

To capitalize on this growth, insurers are increasingly tailoring plans to specific demographics. For instance, plans targeting seniors often include prescription drug coverage and wellness programs, while those for young professionals emphasize mental health services and fitness incentives. Employers, too, are leveraging private insurance as a recruitment tool, with 60% of large firms now offering multiple plan options to meet diverse employee needs. Yet, this customization comes with challenges. Premiums for family plans have risen by 4% annually since 2018, outpacing wage growth and straining household budgets. Consumers must carefully evaluate plan details, such as network restrictions and covered services, to avoid unexpected costs.

A comparative look at private insurance growth in the U.S. versus other developed nations reveals both strengths and weaknesses. While the U.S. market offers unparalleled choice and innovation, it lags in affordability and universal coverage. For example, Switzerland’s private insurance model achieves near-universal coverage with strict regulations on premiums and mandated benefits, a contrast to the U.S.’s more laissez-faire approach. This comparison suggests that sustained growth in the U.S. private market will require addressing affordability and access gaps, potentially through policy reforms or expanded public-private partnerships.

In conclusion, the private insurance market’s growth is a testament to its adaptability and responsiveness to consumer needs, but it also underscores persistent challenges. As the market evolves, stakeholders must balance innovation with equity, ensuring that growth translates into better health outcomes for all Americans. Practical steps for consumers include using online comparison tools, understanding plan specifics, and advocating for policies that promote affordability and accessibility. For insurers and policymakers, the focus should be on creating a sustainable ecosystem that fosters competition while safeguarding consumer interests.

Employer Health Insurance vs. Medicaid: Can You Decline?

You may want to see also

Frequently asked questions

As of 2023, approximately 91% of the US population, or about 300 million people, have some form of health insurance coverage.

About 9% of Americans, or roughly 30 million people, are uninsured. This number has fluctuated over the years, with a slight increase in uninsured rates since 2020 due to factors like the COVID-19 pandemic and changes in policy.

Older adults aged 65 and above have the highest health insurance coverage rate, with nearly 100% insured, primarily through Medicare.