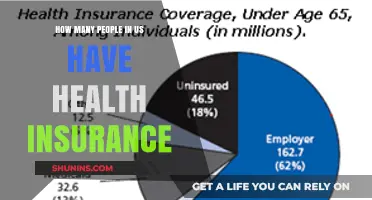

Health insurance is often perceived as complicated due to its intricate interplay of factors such as varying state and federal regulations, a multitude of plan options, complex medical terminology, and the involvement of multiple stakeholders like insurers, providers, and employers. Policyholders must navigate deductibles, copays, premiums, and out-of-pocket maximums, while also understanding network restrictions and coverage limitations. Additionally, the ever-changing landscape of healthcare policies, rising costs, and the need for pre-authorization for certain treatments further contribute to the confusion. This complexity often leaves individuals feeling overwhelmed and uncertain about how to choose the best plan for their needs, highlighting the need for greater transparency and simplification in the system.

| Characteristics | Values |

|---|---|

| Multiple Stakeholders | Involvement of insurers, providers, employers, government, and consumers, each with conflicting interests. |

| Regulatory Complexity | Federal and state regulations (e.g., ACA, Medicare, Medicaid) create overlapping and often contradictory rules. |

| Varied Plan Types | HMOs, PPOs, HDHPs, EPOs, and more, each with different coverage, costs, and provider networks. |

| Opaque Pricing | Lack of transparency in pricing for services, making it difficult for consumers to compare costs. |

| Provider Networks | Limited networks restrict patient choice and increase out-of-pocket costs for out-of-network care. |

| High Administrative Costs | Insurers and providers spend significant resources on billing, claims processing, and compliance. |

| Fragmented System | Lack of a unified healthcare system leads to inefficiencies and inconsistencies in coverage. |

| Pre-existing Conditions | Rules and restrictions around pre-existing conditions add complexity to enrollment and coverage. |

| Deductibles & Copays | Varying cost-sharing mechanisms make it hard for consumers to predict out-of-pocket expenses. |

| Pharmacy Benefits | Separate management of prescription drug coverage adds another layer of complexity. |

| Technological Barriers | Outdated systems and lack of interoperability hinder seamless data sharing and coordination. |

| Market Concentration | Consolidation among insurers and providers reduces competition and increases costs. |

| Consumer Confusion | Complex terminology and plan structures make it difficult for individuals to understand their coverage. |

| Political Influence | Constant legislative changes and partisan debates create uncertainty and instability in the system. |

| Rising Healthcare Costs | Increasing costs of care drive up premiums, deductibles, and out-of-pocket expenses. |

Explore related products

What You'll Learn

- Varying Plan Types: HMOs, PPOs, EPOs, and POS plans differ in coverage and provider access

- High Deductibles: Out-of-pocket costs before coverage begins often confuse policyholders

- Network Restrictions: In-network vs. out-of-network providers impact costs and coverage significantly

- Policy Jargon: Complex terms like copays, premiums, and coinsurance make understanding difficult

- Regulatory Differences: State and federal laws create inconsistencies in coverage and pricing

![]()

Varying Plan Types: HMOs, PPOs, EPOs, and POS plans differ in coverage and provider access

Health insurance complexity often stems from the sheer variety of plan types, each with its own rules, restrictions, and trade-offs. HMOs, PPOs, EPOs, and POS plans aren’t just acronyms—they represent fundamentally different approaches to managing healthcare costs and access. Understanding these differences is crucial for anyone trying to navigate the system effectively.

Analytical Breakdown:

HMOs (Health Maintenance Organizations) prioritize cost control through a strict network of providers. You’ll typically need a primary care physician (PCP) to coordinate all care, and referrals are required for specialists. Out-of-network services are rarely covered, except in emergencies. PPOs (Preferred Provider Organizations) offer more flexibility, allowing you to see any provider, though staying in-network reduces costs significantly. EPOs (Exclusive Provider Organizations) combine HMO and PPO traits—no referrals needed, but out-of-network care isn’t covered, even in emergencies. POS (Point of Service) plans are hybrids, requiring a PCP but allowing out-of-network care at a higher cost. Each plan type reflects a balance between cost, convenience, and control, making the choice deeply personal.

Instructive Guide:

To choose the right plan, start by assessing your healthcare needs. If you value low premiums and don’t mind limited provider choice, an HMO might suit you. For those who prioritize flexibility and are willing to pay more, a PPO is ideal. EPOs are a middle ground, offering no-referral convenience but strict network adherence. POS plans are best for those who want a PCP’s oversight but occasionally need out-of-network care. Pro tip: Always check if your preferred doctors are in-network before enrolling, as this can save you hundreds or even thousands of dollars annually.

Comparative Insight:

Consider a 35-year-old with a chronic condition. An HMO’s low premiums might appeal, but the need for specialist referrals could delay treatment. A PPO offers direct specialist access but at a higher monthly cost. An EPO eliminates referral hassle but restricts provider choice. A POS plan provides a PCP’s guidance while allowing out-of-network care in emergencies. The “best” plan depends on individual priorities—cost, convenience, or control.

Persuasive Argument:

The complexity of these plan types isn’t just an inconvenience; it’s a barrier to informed decision-making. Without clear, standardized explanations, consumers often default to the cheapest option, only to face unexpected costs later. Insurers should simplify plan descriptions and highlight key differences in coverage and provider access. Until then, educating yourself on these distinctions is the best defense against costly surprises.

Descriptive Example:

Imagine Sarah, a 40-year-old with two kids, who needs regular pediatric visits and occasional specialist care. She opts for a PPO because it allows her to see any provider, though she pays more monthly. Her neighbor, John, a healthy 28-year-old, chooses an HMO for its lower premiums and doesn’t mind using a PCP for all care. Both make informed choices based on their needs, but only after hours of research. This illustrates how plan types cater to diverse lifestyles—if you understand them.

By dissecting HMOs, PPOs, EPOs, and POS plans, you can cut through the complexity and select a plan that aligns with your health needs and budget. The key is to focus on provider access and coverage rules, not just the price tag.

Where to Find Username Guard Insurance Company: A Comprehensive Guide

You may want to see also

Explore related products

![]()

High Deductibles: Out-of-pocket costs before coverage begins often confuse policyholders

High deductibles are a double-edged sword in health insurance. On one hand, they lower monthly premiums, making plans more affordable for those who rarely visit the doctor. On the other hand, they create a financial barrier to care, as policyholders must pay out-of-pocket for services until the deductible is met. This system, while designed to reduce overall healthcare costs, often leaves individuals confused and vulnerable, especially when unexpected medical needs arise.

Consider a 35-year-old with a high-deductible health plan (HDHP) and a $3,000 deductible. A routine doctor’s visit costing $200 or even a minor emergency room trip for a sprained ankle ($1,500) would be paid entirely out-of-pocket. Only after reaching the $3,000 threshold does insurance coverage kick in. This structure incentivizes cost-consciousness but can deter necessary care, as individuals may delay or skip treatment to avoid upfront expenses. For chronic conditions requiring frequent visits or prescriptions, the financial burden becomes unsustainable, defeating the purpose of having insurance.

The confusion deepens when policyholders encounter variations in deductible rules. Some plans apply separate deductibles for individuals and families, while others have embedded deductibles, where family members’ expenses count toward both individual and family thresholds. Additionally, not all services require meeting the deductible—preventive care like vaccinations or screenings is often covered at no cost. However, distinguishing between preventive and diagnostic care can be tricky. For instance, a mammogram is preventive, but if an abnormality is found and further tests are needed, those costs may apply to the deductible. This lack of clarity leaves policyholders guessing about their financial responsibility.

To navigate high deductibles effectively, policyholders should adopt a proactive approach. First, understand your plan’s specifics: What counts toward the deductible? Are there separate deductibles for prescriptions or specialist visits? Second, build a health savings account (HSA) if eligible—these accounts allow tax-free savings for medical expenses and can offset out-of-pocket costs. Third, compare prices for services like lab tests or imaging, as costs vary widely between providers. Finally, don’t delay essential care—discuss payment plans with providers if upfront costs are prohibitive. While high deductibles complicate insurance, informed strategies can mitigate their impact.

Best Medical Insurance in the USA: Top Picks

You may want to see also

Explore related products

![]()

Network Restrictions: In-network vs. out-of-network providers impact costs and coverage significantly

Health insurance networks are a labyrinthine system that can significantly impact your out-of-pocket costs and access to care. Understanding the difference between in-network and out-of-network providers is crucial for navigating this complexity.

The Network Divide: Imagine two doctors with identical qualifications practicing across the street from each other. One is in your insurance network, the other isn't. Choosing the in-network doctor means your insurance company has a pre-negotiated rate for services, resulting in lower costs for you. Opting for the out-of-network doctor often leads to higher bills, as your insurance may cover a smaller portion or even deny coverage altogether.

Cost Implications: Let's say you need an MRI. An in-network facility might charge $500, with your insurance covering 80%, leaving you with a $100 copay. The same MRI at an out-of-network facility could cost $1,200, with your insurance covering only 50%, leaving you with a $600 bill. This stark difference highlights the financial consequences of network restrictions.

Coverage Limitations: Network restrictions don't just affect costs; they can also limit your access to specialists or specific treatments. Some plans may require pre-authorization for out-of-network care, adding another layer of bureaucracy. In urgent situations, this delay can be detrimental.

Navigating the Maze: To avoid unexpected expenses, meticulously review your insurance plan's provider directory. If you need to see a specialist not in-network, inquire about exceptions or negotiate rates directly with the provider. Consider using online tools or contacting your insurance company for assistance in finding in-network alternatives.

Remember, understanding network restrictions empowers you to make informed decisions about your healthcare, ensuring you receive the care you need without facing financial hardship.

Berkeley Students: Missed Insurance Deadline? Here's What to Do

You may want to see also

Explore related products

![]()

Policy Jargon: Complex terms like copays, premiums, and coinsurance make understanding difficult

Health insurance policies are riddled with jargon that can leave even the most educated consumers scratching their heads. Terms like *copay*, *premium*, and *coinsurance* are not just confusing; they are often used interchangeably or explained inadequately, creating a barrier to understanding. For instance, a *copay* is a fixed amount you pay for a specific service (e.g., $20 for a doctor’s visit), while *coinsurance* is a percentage of the cost (e.g., 20% of a hospital stay). Without clear definitions, policyholders may unknowingly choose plans that cost them more in the long run.

Consider this scenario: A 35-year-old selects a plan with a $150 monthly *premium* because it’s the cheapest option. However, they later discover the plan has a $5,000 deductible and 30% *coinsurance* for specialist visits. If they need surgery, their out-of-pocket costs could skyrocket, making the low premium a costly trade-off. This example highlights how jargon obscures the true financial implications of a policy, leaving consumers underprepared for expenses.

To navigate this complexity, start by creating a glossary of terms. For example, *deductible* refers to the amount you pay before insurance kicks in, while *out-of-pocket maximum* caps your total yearly expenses. Use online tools or consult a broker to clarify terms in your policy. For instance, if you’re prescribed a $200 medication, knowing your *copay* versus *coinsurance* could save you hundreds. Pro tip: Ask your insurer for a “Summary of Benefits and Coverage” (SBC), a standardized document that explains key terms in plain language.

The problem isn’t just the terms themselves but how they interact. For example, a plan with a low *premium* might have high *coinsurance* or a restrictive provider network. This trade-off is rarely explained transparently, leaving consumers to decipher it themselves. Imagine a 50-year-old with chronic conditions choosing a plan based on a $100 *premium* difference, only to face thousands in *coinsurance* for frequent specialist visits. Such oversights underscore the need for clearer communication.

Ultimately, policy jargon isn’t just an annoyance—it’s a systemic issue that undermines informed decision-making. Until insurers adopt simpler language and standardized explanations, consumers must take proactive steps. Break down your policy into actionable parts: Calculate potential costs for common services, compare plans using real-life scenarios, and don’t hesitate to ask questions. Understanding jargon isn’t just about decoding words—it’s about empowering yourself to choose the best coverage for your health and wallet.

Free Medical Insurance in Washington: Who Qualifies and How?

You may want to see also

Explore related products

![]()

Regulatory Differences: State and federal laws create inconsistencies in coverage and pricing

Health insurance complexity often stems from the patchwork of state and federal regulations that dictate coverage and pricing. Each state has its own insurance commissioner and set of laws, leading to 50 different marketplaces with unique rules. For instance, while federal law mandates coverage for pre-existing conditions under the Affordable Care Act (ACA), states like Texas and Florida have historically resisted expanding Medicaid, leaving gaps in coverage for low-income residents. This disparity means a policy in California might cover acupuncture and telehealth, while a similar plan in Alabama may not, even if both comply with federal minimums.

Consider the example of prescription drug coverage. Federal law requires Medicare Part D plans to cover "at least two drugs per category," but states can mandate additional drugs or impose stricter cost-sharing limits. In New York, state law requires coverage for all FDA-approved contraceptives with no out-of-pocket costs, whereas in Missouri, such mandates are absent. These variations force consumers to navigate a maze of state-specific benefits, often requiring them to choose between affordability and comprehensive coverage. For someone moving across state lines, this means their previous plan might not meet their new state’s requirements, necessitating a complete overhaul of their insurance strategy.

To illustrate further, let’s examine maternity coverage. Federal law under the ACA mandates that all individual and small group plans include maternity care, but states can define the scope of this coverage. In Massachusetts, for example, fertility treatments like IVF are covered under state law, while in most other states, such treatments are optional add-ons. This creates pricing inconsistencies: a 30-year-old woman in Boston might pay $400 monthly for a plan with fertility coverage, while her counterpart in Georgia pays $350 for a plan without it. Such differences highlight how regulatory fragmentation directly impacts consumer costs and access to care.

Navigating these inconsistencies requires proactive steps. First, research your state’s mandated benefits by visiting its insurance department website. For instance, if you’re in Colorado, you’ll find that state law requires coverage for mental health parity and 12-month contraceptive dispensing. Second, use tools like Healthcare.gov’s plan comparison feature, filtering by state to see how federal and state laws interact. Third, consider consulting a licensed broker who specializes in your state’s market—they can decode nuances like whether your state allows short-term health plans (which often skirt ACA regulations) or if it caps out-of-pocket maximums below federal limits.

The takeaway is clear: regulatory differences are not just bureaucratic hurdles—they are practical barriers that affect what you pay and what you get. While federal laws set a baseline, state laws often determine the fine print. Understanding this interplay empowers consumers to make informed choices, whether advocating for policy changes or selecting a plan that aligns with their specific health needs. Until there’s greater standardization, knowing your state’s rules remains the first step in demystifying health insurance complexity.

Life Insurance and Medicaid: What You Need to Know

You may want to see also

Frequently asked questions

Health insurance is complicated due to the interplay of multiple factors, including varying state and federal regulations, complex medical coding systems, diverse plan structures, and the involvement of numerous stakeholders like insurers, providers, and employers.

Health insurance policies use technical jargon and legal language to define coverage, exclusions, and limitations. Additionally, plans often have specific terms like deductibles, copays, and out-of-pocket maximums, which can be confusing without clear explanations.

Costs vary due to differences in coverage levels, network sizes, geographic location, and individual health needs. Insurers also factor in administrative expenses, profit margins, and the overall risk pool when setting premiums, leading to significant price differences.

![It's Complicated / Mamma Mia! The Movie / One True Thing / Prime 4-Movie Collection [DVD]](https://m.media-amazon.com/images/I/71OjqiaNsZL._AC_UY218_.jpg)

![It's Complicated [Blu-ray]](https://m.media-amazon.com/images/I/71aCexnjUCL._AC_UY218_.jpg)