Health insurance is a critical component of financial and personal well-being, yet its necessity remains a topic of debate. Proponents argue that it provides essential protection against high medical costs, ensuring access to quality healthcare without the risk of financial ruin. In contrast, critics question its affordability and whether the benefits outweigh the premiums, especially for those who rarely require medical services. The necessity of health insurance ultimately depends on individual circumstances, such as age, health status, and financial stability, as well as broader factors like the availability of public healthcare options. Understanding its role in safeguarding both health and finances is key to making an informed decision.

| Characteristics | Values |

|---|---|

| Financial Protection | Covers high medical costs, preventing out-of-pocket expenses and potential bankruptcy. |

| Access to Preventive Care | Encourages regular check-ups, screenings, and vaccinations, reducing long-term health risks. |

| Emergency Coverage | Provides immediate financial support for accidents, sudden illnesses, or critical conditions. |

| Chronic Disease Management | Helps manage ongoing conditions like diabetes, heart disease, or cancer with affordable treatments. |

| Mental Health Support | Includes therapy, counseling, and mental health treatments, addressing holistic well-being. |

| Prescription Drug Coverage | Reduces costs of essential medications, making them more accessible. |

| Legal Requirement | Mandatory in some countries (e.g., U.S. Affordable Care Act penalties for not having insurance). |

| Employer-Sponsored Benefits | Often provided as part of employment packages, reducing individual costs. |

| Peace of Mind | Reduces stress related to unexpected medical expenses. |

| Network Access | Provides access to a network of healthcare providers, ensuring quality care. |

| Cost-Effectiveness | Long-term savings compared to paying full medical costs without insurance. |

| Global Coverage | Some plans offer international coverage for travel or relocation. |

| Maternity and Childcare | Covers prenatal care, childbirth, and pediatric services. |

| Aging Population Needs | Essential for seniors due to increased health risks and medical needs. |

| Inflation Hedge | Protects against rising healthcare costs over time. |

| Alternative Options | Alternatives like Health Savings Accounts (HSAs) or government programs exist but may not offer comprehensive coverage. |

Explore related products

What You'll Learn

![]()

Cost vs. Benefit Analysis

Health insurance premiums can consume a significant portion of your monthly budget, often leaving individuals and families questioning their necessity. A cost-benefit analysis is crucial to determine if the financial burden of health insurance justifies the potential advantages. This analysis involves weighing the immediate and long-term costs against the value of coverage, considering factors like age, health status, and lifestyle.

Understanding the Costs: Health insurance costs vary widely based on plan type, coverage level, and provider. For instance, a healthy 30-year-old might pay around $200-$400 monthly for a mid-tier plan, while a family plan could exceed $1,000. Deductibles, copays, and coinsurance further complicate the expense structure. High-deductible plans may offer lower premiums but require substantial out-of-pocket spending before coverage kicks in. For example, a plan with a $5,000 deductible means you pay the first $5,000 of medical expenses annually before insurance covers costs.

Evaluating the Benefits: The primary benefit of health insurance is financial protection against high medical costs. Without insurance, a single hospital visit can lead to bills ranging from $10,000 for a minor procedure to over $50,000 for major surgeries. Insurance also provides access to preventive care, such as annual check-ups, vaccinations, and screenings, which can detect health issues early. For instance, a mammogram, costing around $200-$300 without insurance, is typically covered under preventive care, potentially saving thousands in treatment costs if breast cancer is detected early.

Practical Tips for Analysis: To perform a cost-benefit analysis, start by assessing your health needs and financial situation. If you’re young and healthy, a high-deductible plan with a health savings account (HSA) might be cost-effective, allowing you to save pre-tax dollars for medical expenses. For those with chronic conditions, a comprehensive plan with lower out-of-pocket costs is more beneficial. Consider the frequency of doctor visits, prescription needs, and potential risks based on family medical history. For example, if diabetes runs in your family, a plan covering regular blood tests and medications could prevent long-term complications.

Long-Term Considerations: While health insurance may seem expensive, the long-term benefits often outweigh the costs. Chronic conditions like heart disease or diabetes can lead to lifelong expenses, and insurance ensures manageable payments. Additionally, accidents or unexpected illnesses can occur at any age, making coverage a safeguard against financial ruin. For instance, a 40-year-old with no insurance who suffers a heart attack could face bills exceeding $100,000, whereas insurance would cap out-of-pocket costs at a fraction of that amount.

Accident Insurance: Statutory Regulation of Occupation Coverage

You may want to see also

Explore related products

$196.36 $245.95

![]()

Emergency Coverage Importance

Unforeseen medical emergencies can strike anyone, regardless of age or health status. A sudden accident, a severe illness, or a critical health event can lead to exorbitant medical bills, often reaching tens or even hundreds of thousands of dollars. Without adequate emergency coverage, individuals and families may face financial ruin, forced to deplete savings, incur debt, or even declare bankruptcy. This harsh reality underscores the critical importance of health insurance that includes robust emergency coverage.

Consider the scenario of a 35-year-old individual involved in a car accident, requiring immediate surgery, intensive care, and rehabilitation. The average cost of a three-day hospital stay in the U.S. exceeds $30,000, with emergency room visits alone averaging $1,389. For those without insurance, these costs are entirely out-of-pocket. Even a seemingly minor emergency, like a broken limb, can result in bills upwards of $2,500. Health insurance with emergency coverage acts as a financial safety net, ensuring access to necessary care without the burden of overwhelming expenses.

Emergency coverage is not just about cost mitigation; it’s about timely access to care. Insured individuals are more likely to seek immediate treatment during emergencies, reducing the risk of complications. For instance, a heart attack patient covered by insurance can afford the $20,000–$50,000 cost of emergency angioplasty, a procedure that significantly improves survival rates. Conversely, uninsured individuals often delay care, leading to worse health outcomes and higher long-term costs. This highlights the dual benefit of emergency coverage: financial protection and improved health.

When evaluating health insurance plans, scrutinize the emergency coverage details. Ensure the policy covers ambulance services, emergency room visits, urgent care, and follow-up treatments. Be wary of plans with high deductibles or out-of-network penalties, as these can still leave you with substantial costs. For example, a plan with a $5,000 deductible may require you to pay that amount before coverage kicks in, even in an emergency. Opt for comprehensive plans that prioritize emergency care without hidden limitations.

Practical tip: Review your policy’s definition of an emergency, as insurers may have specific criteria. For instance, some plans cover emergencies only if treatment is sought within 24 hours of symptom onset. Keep your insurer’s emergency contact information readily available, and understand the process for pre-authorization if required. Additionally, consider supplemental insurance options like accident or critical illness policies for added protection. Emergency coverage is not a luxury—it’s a necessity for safeguarding both your health and financial future.

Does Health Insurance Cover Cataract Surgery? What You Need to Know

You may want to see also

Explore related products

$80.56 $92.95

$87.96 $92.95

![]()

Preventive Care Access

Consider the case of a 45-year-old uninsured individual with a family history of diabetes. Without insurance, they might delay a $100 blood glucose test, increasing the risk of undiagnosed prediabetes progressing to full-blown diabetes. With insurance, this test is typically covered, enabling early intervention through lifestyle changes or medications like metformin (500–1000 mg daily). This example underscores how insurance acts as a gatekeeper to preventive care, turning potential health crises into manageable conditions.

From a comparative standpoint, countries with universal healthcare systems, such as Canada and the UK, demonstrate higher preventive care utilization rates. In these systems, access is not tied to insurance status, resulting in better population health outcomes. For example, colorectal cancer screening rates in Canada (68%) surpass those in the U.S. (65%), where insurance gaps persist. This disparity highlights the role of insurance in shaping access, suggesting that necessity extends beyond individual benefit to broader public health implications.

To maximize preventive care access with insurance, policyholders should familiarize themselves with covered services, often listed in plan summaries. Scheduling annual wellness visits, staying current on age-specific screenings (e.g., colonoscopy at 45, HPV vaccine by age 26), and leveraging telehealth for consultations can optimize benefits. For the uninsured, community health clinics and state-funded programs offer low-cost alternatives, though availability varies by region. Ultimately, insurance remains a critical tool for bridging the gap between preventive care availability and actual utilization.

Understanding Primerica: A Comprehensive Guide to Their Life Insurance Services

You may want to see also

Explore related products

$9.97 $19.99

$8

![]()

Financial Risk Protection

Unforeseen medical expenses are the leading cause of bankruptcy in the United States, accounting for roughly 66.5% of all bankruptcies, according to a study published in the *American Journal of Public Health*. This stark statistic underscores the critical role of financial risk protection in safeguarding individuals and families from the devastating economic consequences of unexpected health issues. Health insurance serves as a buffer against these risks, ensuring that a sudden illness or injury doesn’t spiral into long-term financial hardship. Without it, even routine medical care can become a prohibitive expense, let alone catastrophic events like surgeries or chronic disease management.

Consider the hypothetical case of a 35-year-old individual who experiences a sudden heart attack. The average cost of hospitalization for such an event exceeds $20,000, not including follow-up care, medications, or rehabilitation. For someone without insurance, this expense could be insurmountable, leading to debt, loss of assets, or even bankruptcy. Health insurance, however, caps out-of-pocket costs through deductibles, copays, and coinsurance, making these expenses manageable. For instance, a typical plan might limit annual out-of-pocket spending to $8,000, shielding the individual from the full financial burden.

From a practical standpoint, selecting a health insurance plan with robust financial risk protection involves evaluating several key factors. First, assess the plan’s deductible—the amount you pay before insurance kicks in. A lower deductible reduces upfront costs but often comes with higher premiums. Second, examine the out-of-pocket maximum, which caps your total annual expenses. Plans with lower out-of-pocket maximums offer stronger protection but may have higher monthly costs. Third, consider the network of providers; staying in-network can significantly reduce costs. For example, a plan with a $1,500 deductible and a $5,000 out-of-pocket maximum provides more predictable financial exposure compared to a high-deductible plan with a $7,000 out-of-pocket limit.

Critics argue that health insurance premiums themselves can be a financial burden, particularly for low-income individuals. However, this perspective overlooks the long-term benefits of risk mitigation. For instance, a 2020 Kaiser Family Foundation analysis found that uninsured individuals pay, on average, 80% more for medical services than those with insurance due to a lack of negotiated rates. Moreover, government subsidies and employer contributions often offset premium costs, making insurance more affordable than paying out-of-pocket for care. In this light, health insurance is not just an expense but an investment in financial stability.

Ultimately, financial risk protection is a cornerstone of health insurance’s necessity. It transforms unpredictable, potentially ruinous medical costs into manageable expenses, preserving both health and wealth. By carefully selecting a plan tailored to individual needs and budget, one can achieve peace of mind knowing that unexpected health events won’t derail financial security. In a world where medical debt remains a pervasive threat, health insurance isn’t just a safety net—it’s a strategic tool for long-term financial resilience.

Understanding CMFG Life Insurance: History, Services, and Customer Benefits

You may want to see also

Explore related products

![]()

Legal and Policy Requirements

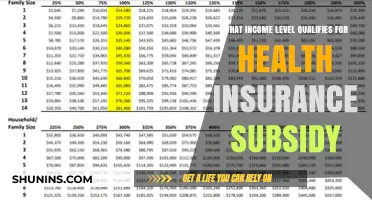

In the United States, the Affordable Care Act (ACA) mandates that most individuals maintain minimum essential health coverage, with penalties for non-compliance phased out since 2019. However, certain states like New Jersey, California, and Massachusetts have reinstated their own insurance mandates, imposing state-level tax penalties for uninsured residents. For instance, California’s penalty for 2023 is calculated as either 2.5% of household income above the tax filing threshold or a flat fee of $800 per adult and $400 per child, whichever is higher. Understanding these state-specific requirements is critical, as they directly impact tax liabilities and compliance obligations.

Globally, countries like Germany and Japan enforce compulsory health insurance through employer-based systems or government-run schemes, leaving no room for opting out. In Germany, employees contribute approximately 7.3% of their gross income (up to a cap of €58,050 annually) to statutory health insurance, while employers match this contribution. Japan’s system requires enrollment in either employee-based or national health insurance, with premiums tied to income and household size. These models highlight how legal frameworks abroad prioritize universal coverage, contrasting with the optional nature of insurance in some U.S. states.

For employers, the ACA’s employer mandate requires businesses with 50 or more full-time equivalent employees to offer affordable, minimum-value health plans or face penalties. "Affordable" is defined as employee contributions not exceeding 9.12% of household income for the lowest-cost plan in 2023. Non-compliance triggers penalties of $2,000 per full-time employee (after the first 30), while failure to provide minimum essential coverage incurs $3,850 per uninsured employee. Small businesses, however, can leverage the Small Business Health Care Tax Credit, covering up to 50% of premium costs if they contribute at least 50% of employee premiums and have fewer than 25 full-time equivalent employees with average wages below $56,000.

Medicare and Medicaid enrollment is legally required for eligible populations, with automatic Medicare Part A enrollment for individuals aged 65+ receiving Social Security benefits. Failure to enroll in Part B during the Initial Enrollment Period (three months before/after the 65th birthday) results in late penalties of 10% for each 12-month period of delay. Medicaid eligibility varies by state but generally covers individuals under 65 with incomes up to 138% of the federal poverty level ($18,754 for a single adult in 2023). States expanding Medicaid under the ACA have seen reduced uninsured rates, emphasizing the role of policy in shaping access.

Navigating legal requirements demands proactive steps: annually reviewing state-specific mandates, ensuring employer plans meet ACA standards, and enrolling in Medicare/Medicaud during designated periods. For instance, using the Health Insurance Marketplace during Open Enrollment (November 1–January 15) allows individuals to avoid coverage gaps. Employers should conduct annual audits to confirm compliance with the employer mandate, while individuals nearing 65 should enroll in Medicare three months before their birthday to prevent penalties. These actions transform abstract policies into actionable safeguards, ensuring both legal adherence and financial protection.

Switching Back to Medicare from Humana Insurance: A Guide

You may want to see also

Frequently asked questions

Yes, health insurance is still necessary even if you’re young and healthy. Unexpected accidents, illnesses, or emergencies can happen to anyone, and medical costs can be extremely high without coverage. Health insurance provides financial protection and ensures access to preventive care, which can help maintain your health in the long run.

Yes, health insurance is necessary even if you rarely visit the doctor. It’s not just about routine check-ups; it’s about being prepared for unforeseen medical expenses. Without insurance, a single major health event could lead to significant debt. Additionally, many plans cover preventive services, which can help catch potential issues early.

While you may be able to afford some medical expenses, health insurance is still necessary to protect against catastrophic costs. Major surgeries, hospitalizations, or chronic conditions can result in bills that far exceed your budget. Insurance spreads the risk, ensuring you’re not financially devastated by unexpected health issues.

Yes, health insurance is still necessary even if you have access to free or low-cost clinics. These clinics often have limited services and may not cover specialized care, emergency treatments, or prescription medications. Health insurance provides comprehensive coverage, ensuring you have access to a wider range of healthcare services when needed.