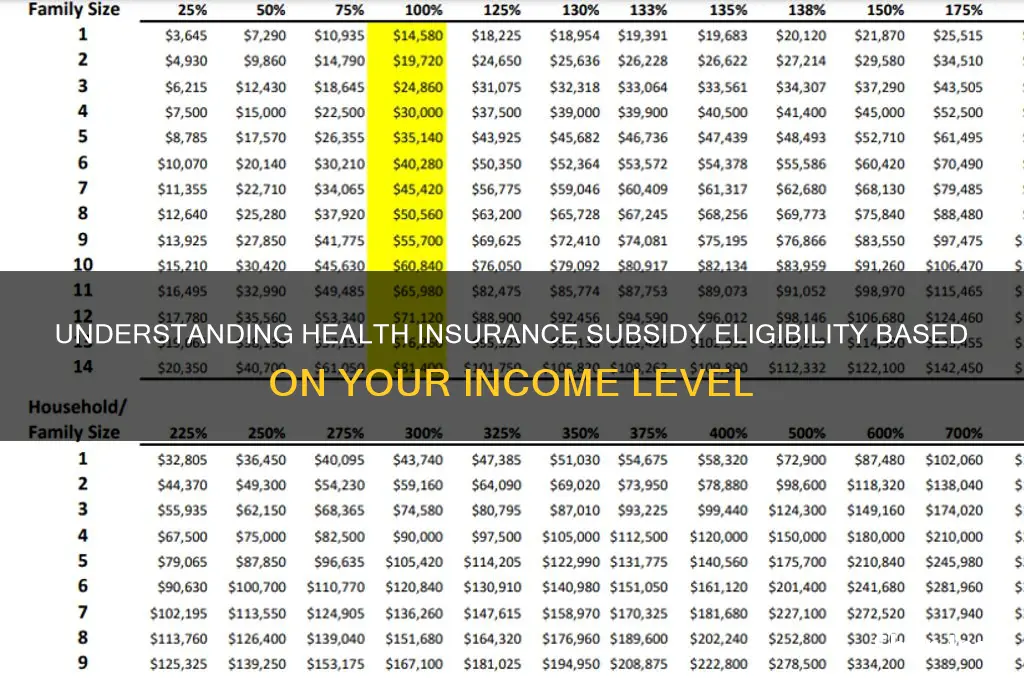

Understanding what income level qualifies for a health insurance subsidy is crucial for individuals and families seeking affordable healthcare coverage. In the United States, subsidies are primarily available through the Affordable Care Act (ACA) marketplace and are designed to reduce the cost of premiums and out-of-pocket expenses for eligible participants. Qualification is based on the Federal Poverty Level (FPL), with subsidies typically available to households earning between 100% and 400% of the FPL, though some states have expanded Medicaid to cover those below 100% FPL. For 2023, this translates to an annual income range of approximately $13,590 to $54,360 for an individual and $27,750 to $111,000 for a family of four. Additionally, the American Rescue Plan Act (ARPA) expanded subsidy eligibility, allowing more people to qualify, even those with incomes above 400% FPL, by capping premium contributions at 8.5% of their household income. It’s essential to check specific state guidelines and use the marketplace’s subsidy calculator to determine eligibility accurately.

| Characteristics | Values |

|---|---|

| Eligibility Income Level | 100% - 400% of the Federal Poverty Level (FPL) |

| 2023 FPL for a Single Individual | $14,580 (100% FPL) to $58,320 (400% FPL) |

| 2023 FPL for a Family of 4 | $30,000 (100% FPL) to $120,000 (400% FPL) |

| Subsidy Type | Premium Tax Credits (PTC) for Marketplace plans |

| Cost-Sharing Reduction (CSR) Eligibility | 100% - 250% FPL for reduced out-of-pocket costs (deductibles, copays) |

| Medicaid Expansion Eligibility | Up to 138% FPL in states that expanded Medicaid |

| No Subsidy Above | 400% FPL (must pay full premium without subsidy) |

| Special Considerations | Household size, location, and age affect FPL calculations |

| Application Platform | Health Insurance Marketplace (Healthcare.gov) |

| Annual Updates | FPL thresholds are updated annually by the federal government |

Explore related products

What You'll Learn

![]()

Federal Poverty Level (FPL) guidelines for subsidy eligibility

The Federal Poverty Level (FPL) is a critical benchmark for determining eligibility for health insurance subsidies, particularly through the Affordable Care Act (ACA) marketplace. For 2023, individuals earning between 100% and 400% of the FPL qualify for premium tax credits, which reduce monthly insurance premiums. For a single person, this translates to an annual income range of $14,580 to $58,320. Families must calculate their eligibility based on household size; for instance, a family of four falls within the subsidy range if their income is between $30,000 and $120,000. Understanding these thresholds is the first step in assessing whether you qualify for financial assistance.

While the 100% to 400% FPL range is the primary eligibility window, it’s important to note exceptions and nuances. For example, individuals earning below 100% of the FPL may qualify for Medicaid in states that expanded the program, bypassing the need for ACA subsidies. Conversely, those above 400% of the FPL are generally ineligible for subsidies but may still benefit from cost-sharing reductions if their income is below 250% of the FPL. Additionally, the FPL guidelines are adjusted annually for inflation, so it’s crucial to check the latest figures when enrolling in or renewing coverage.

A practical tip for navigating FPL guidelines is to use the ACA marketplace’s subsidy calculator, which accounts for household size, income, and location. This tool simplifies the process by automatically applying the current FPL thresholds and estimating your subsidy amount. Keep in mind that income includes wages, self-employment earnings, unemployment benefits, and other taxable sources. If your income fluctuates, consider projecting your annual earnings conservatively to avoid overestimating subsidy eligibility and facing repayment at tax time.

Comparing FPL guidelines across states highlights the impact of Medicaid expansion on subsidy eligibility. In expansion states, individuals below 138% of the FPL are directed to Medicaid, while those above this threshold seek ACA subsidies. In non-expansion states, the gap between 100% and 138% of the FPL creates a "coverage gap," where individuals earn too much for Medicaid but too little for ACA subsidies. This disparity underscores the importance of understanding both federal and state-specific policies when assessing your eligibility.

Finally, while FPL guidelines are central to subsidy eligibility, they are not the sole factor. Other considerations include citizenship status, immigration status, and access to employer-sponsored insurance. For instance, if your employer offers affordable coverage, you may not qualify for ACA subsidies, regardless of your income relative to the FPL. By carefully reviewing these criteria and staying informed about annual updates, you can maximize your chances of securing affordable health insurance.

Meet the New CEO of Shelter Insurance Company: Leadership Changes

You may want to see also

Explore related products

![]()

Income limits for Marketplace premium tax credits

The Affordable Care Act (ACA) established premium tax credits to help individuals and families with low to moderate incomes afford health insurance through the Marketplace. To qualify, your income must fall within a specific range, expressed as a percentage of the federal poverty level (FPL). For 2023, the income limits for premium tax credits are set between 100% and 400% of the FPL. However, due to temporary expansions under the American Rescue Plan, individuals with incomes above 400% of the FPL may also qualify for subsidies if their premium costs exceed a certain percentage of their income.

Consider a single individual in 2023. If the federal poverty level for one person is $13,590, then 100% of the FPL is $13,590, and 400% is $54,360. This means a single person earning between $13,590 and $54,360 annually could qualify for a premium tax credit. For a family of four, the FPL is $27,750, so the range becomes $27,750 to $111,000. These figures are crucial because they determine eligibility for subsidies that can significantly reduce monthly premiums, making health insurance more accessible.

One practical tip for applicants is to estimate their annual income as accurately as possible when enrolling. Overestimating could result in receiving a smaller subsidy than eligible for, while underestimating might lead to repaying excess credits at tax time. Tools like the Healthcare.gov subsidy calculator can help individuals gauge their eligibility based on income. Additionally, if your income fluctuates during the year, report changes to the Marketplace promptly to ensure your subsidy amount remains accurate.

A comparative analysis reveals that the income limits for premium tax credits are more generous than those for Medicaid, which typically caps eligibility at 138% of the FPL in states that expanded Medicaid. This means individuals earning above 138% but below 400% of the FPL fall into a gap where they qualify for premium tax credits but not Medicaid. For example, a single individual earning $20,000 annually (147% of the FPL) would not qualify for Medicaid in an expansion state but would be eligible for a premium tax credit.

Finally, it’s worth noting that the American Rescue Plan Act (ARPA) temporarily removed the income cap for premium tax credits, allowing individuals with incomes above 400% of the FPL to qualify if their premium costs exceed 8.5% of their income. This change, extended through 2025, has expanded access to subsidies for higher-income individuals facing steep insurance costs. For instance, a family of four earning $150,000 (above 400% of the FPL) might qualify for a subsidy if their benchmark plan premium exceeds $12,750 annually (8.5% of $150,000). This flexibility underscores the importance of checking eligibility, even if your income seems too high.

Why You Should Avoid Sharing Your Insurance Company Document

You may want to see also

Explore related products

![]()

Medicaid expansion income thresholds by state

Medicaid expansion has significantly altered the landscape of health insurance eligibility, particularly for low-income individuals and families. The income thresholds for qualifying vary by state, reflecting the flexibility afforded to states under the Affordable Care Act (ACA). As of 2023, 38 states and the District of Columbia have adopted Medicaid expansion, setting their income eligibility limits at 138% of the federal poverty level (FPL). This means a single individual earning up to $18,754 annually or a family of four with an income of up to $38,295 could qualify for Medicaid in these states. However, in non-expansion states, the criteria are often much stricter, sometimes excluding able-bodied adults without children entirely, regardless of their income level.

To illustrate the disparity, consider Texas, a non-expansion state, where the income threshold for Medicaid eligibility is approximately 17% of the FPL for parents. This translates to an annual income cap of around $4,000 for a family of three, leaving many low-income adults in a coverage gap. In contrast, California, an expansion state, offers Medicaid (known as Medi-Cal) to individuals and families earning up to 138% of the FPL, ensuring broader access to healthcare services. These differences highlight the importance of understanding state-specific thresholds when assessing eligibility for health insurance subsidies.

For those navigating Medicaid expansion income thresholds, it’s crucial to verify your state’s status and eligibility criteria. Use the Healthcare.gov tool or your state’s Medicaid website to input your household size and income for an accurate assessment. Additionally, consider annual changes to the FPL, which directly impact income thresholds. For instance, in 2023, the FPL for a single individual is $14,580, and 138% of this amount is $20,120. If your state has expanded Medicaid, this is the income cap to keep in mind.

A practical tip for maximizing eligibility is to account for all deductions allowed under Medicaid rules, such as certain work-related expenses or medical costs. These deductions can lower your countable income, potentially pushing you within the threshold. For example, if you’re self-employed, you may deduct half of your self-employment tax from your income when calculating Medicaid eligibility. Similarly, high medical expenses can be subtracted, making it easier to qualify.

In conclusion, Medicaid expansion income thresholds are not one-size-fits-all but vary dramatically by state. Expansion states offer a more inclusive approach, covering individuals and families up to 138% of the FPL, while non-expansion states maintain stricter, often exclusionary criteria. By understanding these thresholds and leveraging available tools and deductions, you can better navigate the system to secure the health insurance subsidies you may be entitled to. Always stay informed about your state’s policies, as they can change and directly impact your eligibility.

Orthognathic Surgery: Medical or Dental Insurance Coverage?

You may want to see also

Explore related products

![]()

Cost-sharing reduction (CSR) subsidy income requirements

Cost-sharing reduction (CSR) subsidies are a critical component of making health insurance more affordable for lower-income individuals and families enrolled in Marketplace plans. Unlike premium tax credits, which reduce monthly premiums, CSR subsidies lower out-of-pocket costs like deductibles, copayments, and coinsurance. To qualify, your income must fall within a specific range: between 100% and 250% of the federal poverty level (FPL). For 2023, this translates to an annual income of approximately $14,580 to $36,450 for a single individual, with higher thresholds for larger households. For example, a family of four would need to earn between $30,000 and $75,000 to be eligible.

Understanding the income thresholds is just the first step. CSR subsidies are only available to those who enroll in a Silver-level Marketplace plan. This is a strategic requirement, as Silver plans are designed to work seamlessly with CSR benefits. For instance, if your income is 200% of the FPL, your Silver plan’s deductible could be reduced from $4,000 to as low as $750, making healthcare far more accessible. It’s essential to verify your eligibility during the enrollment process, as CSR subsidies are automatically applied if you meet the income criteria and select a Silver plan.

A common misconception is that CSR subsidies are the same for everyone within the 100% to 250% FPL range. In reality, the level of cost-sharing reduction varies based on where your income falls within this spectrum. For example, individuals at 150% FPL receive more substantial reductions than those at 250% FPL. This tiered approach ensures that those with the lowest incomes receive the most significant assistance. To maximize your benefits, use the Marketplace’s subsidy calculator to estimate your eligibility and potential savings before enrolling.

Practical tips can help you navigate the CSR subsidy process effectively. First, gather accurate income documentation, such as tax returns or pay stubs, to ensure your application reflects your current financial situation. Second, if your income fluctuates during the year, report changes promptly to avoid overpaying or losing benefits. Finally, consider working with a certified navigator or broker who can guide you through the complexities of CSR subsidies and help you select the best Silver plan for your needs. By understanding and leveraging CSR subsidies, you can significantly reduce your healthcare costs and improve access to essential services.

Why Insurance Companies Advertise: Unlocking the Secrets Behind Their Marketing Strategies

You may want to see also

Explore related products

![]()

Impact of household size on subsidy qualification

Household size plays a pivotal role in determining eligibility for health insurance subsidies, as it directly influences the federal poverty level (FPL) threshold used to assess income qualifications. For instance, a single-person household in 2023 qualifies for subsidies if their income falls between 100% and 400% of the FPL, while a family of four must earn between 100% and 400% of a higher FPL threshold. This means larger households can earn more and still qualify for assistance, reflecting the increased financial burden of supporting multiple individuals.

Consider a practical example: a single individual earning $54,360 annually (400% of the 2023 FPL for one person) would be at the upper limit for subsidy eligibility. In contrast, a family of four with an income of $111,000 (400% of the FPL for four people) would also qualify, despite earning nearly double the single individual’s income. This disparity highlights how household size expands the income range for subsidy eligibility, ensuring larger families aren’t excluded from financial assistance.

However, the relationship between household size and subsidy qualification isn’t linear. Adding dependents increases the FPL threshold but also raises living expenses, which may not always be fully accounted for in subsidy calculations. For example, a family of five may face higher costs for housing, food, and childcare, yet their subsidy eligibility is based solely on income relative to the FPL. This can create gaps where families technically qualify for subsidies but still struggle to afford coverage.

To navigate this complexity, households should carefully calculate their Modified Adjusted Gross Income (MAGI) and compare it to the FPL for their size. Tools like the Healthcare.gov subsidy calculator can provide clarity. Additionally, households nearing the 400% FPL threshold should explore other cost-saving options, such as Health Savings Accounts (HSAs) or state-specific programs, to offset potential out-of-pocket costs. Understanding these nuances ensures families maximize their eligibility and financial support.

Ultimately, the impact of household size on subsidy qualification underscores the need for a tailored approach to healthcare affordability. Policymakers and consumers alike must recognize that one-size-fits-all income thresholds can fall short for larger families. By advocating for more nuanced subsidy models and leveraging available resources, households can better align their financial realities with the support they receive, ensuring access to affordable healthcare for all family members.

ACA Withdrawals: Which Insurers Left Obamacare in 2023?

You may want to see also

Frequently asked questions

To qualify for a health insurance subsidy, your household income must be between 100% and 400% of the Federal Poverty Level (FPL). For 2023, this translates to approximately $13,590 to $54,360 for an individual and $27,750 to $111,000 for a family of four.

If your income is below 100% of the FPL, you generally do not qualify for ACA subsidies. However, you may be eligible for Medicaid in states that have expanded the program under the ACA. Eligibility rules for Medicaid vary by state.

Yes, certain circumstances can impact eligibility. For example, if you have high medical expenses or other deductions, your adjusted income may be lower, potentially qualifying you for a subsidy. Additionally, cost-sharing reductions are available for those with incomes between 100% and 250% of the FPL, providing additional financial assistance.