Navigating the cost of health insurance can feel overwhelming, especially when premiums, deductibles, and out-of-pocket expenses seem to climb higher each year. For many, the question of affordability isn’t just about balancing the budget—it’s about ensuring access to essential care without sacrificing financial stability. With rising healthcare costs, limited employer-sponsored plans, and complex marketplace options, understanding how to secure coverage that fits your needs and wallet requires careful consideration of available resources, subsidies, and alternative solutions. Whether you’re self-employed, between jobs, or simply struggling to make ends meet, exploring strategies like government assistance, short-term plans, or health-sharing ministries could provide a pathway to affordable care.

Explore related products

What You'll Learn

- Understanding Insurance Costs: Break down premiums, deductibles, and out-of-pocket expenses to assess affordability

- Government Assistance Programs: Explore Medicaid, ACA subsidies, and other public health insurance options

- Employer-Sponsored Plans: Check if your job offers health insurance and compare coverage options

- Short-Term Health Plans: Consider temporary, low-cost plans for immediate coverage needs

- Health Savings Accounts (HSAs): Use tax-advantaged accounts to save for medical expenses

![]()

Understanding Insurance Costs: Break down premiums, deductibles, and out-of-pocket expenses to assess affordability

Health insurance costs can feel like a labyrinth, but understanding the key components—premiums, deductibles, and out-of-pocket expenses—transforms confusion into clarity. Premiums are your monthly payments to maintain coverage, regardless of whether you use medical services. Deductibles are the amount you pay out of pocket before insurance kicks in, while out-of-pocket expenses include copays, coinsurance, and any costs beyond your deductible. By dissecting these elements, you can evaluate whether a plan aligns with your budget and healthcare needs.

Consider this scenario: Plan A has a $300 monthly premium, a $1,500 deductible, and 20% coinsurance. Plan B costs $450 monthly, has a $500 deductible, and 10% coinsurance. If you’re generally healthy and rarely visit the doctor, Plan A’s lower premium might save you money annually. However, if you anticipate frequent medical care, Plan B’s higher premium but lower deductible and coinsurance could reduce overall costs. This comparative analysis highlights how understanding these components helps tailor your choice to your lifestyle.

For those under 30 or with limited income, high-deductible health plans (HDHPs) paired with Health Savings Accounts (HSAs) offer a strategic option. HDHPs typically have lower premiums but higher deductibles, making them affordable for young, healthy individuals. Contributing to an HSA allows you to save pre-tax dollars for medical expenses, effectively reducing your taxable income. For example, if you’re 25 and healthy, a $200 monthly premium HDHP with a $2,000 deductible could save you $3,000 annually compared to a traditional plan, especially if you rarely exceed the deductible.

A cautionary note: don’t fixate solely on premiums. A low premium plan with a high deductible and coinsurance can lead to staggering costs during emergencies. For instance, a $5,000 deductible with 30% coinsurance for a $10,000 surgery means you pay $8,000 out of pocket. Conversely, a plan with a $600 premium and $2,000 deductible might cap your out-of-pocket maximum at $5,000, offering better financial protection. Always calculate potential worst-case scenarios to ensure affordability.

Finally, leverage available resources to reduce costs. Government subsidies through the Affordable Care Act can lower premiums for individuals earning up to 400% of the federal poverty level. For example, a single person earning $54,360 annually might qualify for a subsidy reducing their premium by $200 monthly. Additionally, employer-sponsored plans often share premium costs, making them more affordable. By combining this knowledge with a clear understanding of insurance components, you can navigate the system confidently and find a plan that fits your financial reality.

Top Companies Providing Health Insurance Benefits for Part-Time Workers

You may want to see also

Explore related products

![]()

Government Assistance Programs: Explore Medicaid, ACA subsidies, and other public health insurance options

If you're struggling to afford health insurance, government assistance programs can provide a lifeline. Medicaid, for instance, is a joint federal and state program designed to help low-income individuals and families. Eligibility varies by state, but generally, if your income is below 138% of the federal poverty level (FPL), you may qualify. For a single individual in 2023, this equates to an annual income of approximately $18,754. Families of four with an income below $38,295 may also be eligible. To apply, visit your state’s Medicaid website or use the HealthCare.gov portal. Keep in mind that some states have expanded Medicaid under the Affordable Care Act (ACA), broadening eligibility criteria.

ACA subsidies, formally known as premium tax credits, are another critical resource. These subsidies reduce the cost of health insurance plans purchased through the Health Insurance Marketplace. Eligibility is based on income and household size. For example, a family of three earning between 100% and 400% of the FPL (roughly $22,000 to $88,000 annually) may qualify. The subsidy amount is calculated to ensure you don’t pay more than a certain percentage of your income on premiums, typically capped at 8.5%. To apply, complete the Marketplace application, which will automatically determine your eligibility for subsidies. Be sure to update your income information annually to maintain accurate subsidy amounts.

Beyond Medicaid and ACA subsidies, other public health insurance options exist. The Children’s Health Insurance Program (CHIP) provides low-cost coverage for children in families who earn too much for Medicaid but still struggle to afford private insurance. Income limits vary by state but generally cover families earning up to 200% of the FPL. For pregnant women, the Special Supplemental Nutrition Program for Women, Infants, and Children (WIC) offers healthcare referrals and nutritional support. Additionally, some states offer specific programs for groups like veterans, disabled individuals, or those with chronic conditions. Research your state’s offerings or consult a local healthcare navigator for personalized guidance.

When exploring these options, it’s essential to understand the application process and required documentation. Gather proof of income, citizenship or immigration status, and household size before applying. Be prepared for potential wait times, as processing applications can take several weeks. If you’re denied coverage, don’t hesitate to appeal the decision—many denials are overturned upon review. Finally, stay informed about policy changes, as eligibility criteria and benefits can shift with legislative updates. By leveraging these government assistance programs, you can secure affordable health insurance tailored to your needs.

Understanding Medical Insurance Back Payments: Your Questions Answered

You may want to see also

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UY218_.jpg)

![]()

Employer-Sponsored Plans: Check if your job offers health insurance and compare coverage options

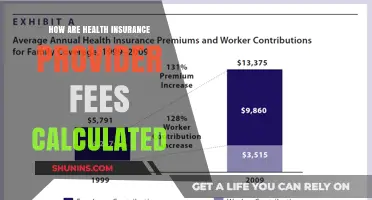

One of the most accessible pathways to affordable health insurance is through employer-sponsored plans. If you’re currently employed, your first step should be to verify whether your job offers health insurance as part of its benefits package. Many employers subsidize a portion of the premium, significantly reducing your out-of-pocket costs. For example, the average annual premium for employer-sponsored family coverage in 2023 was $22,463, but employees only paid $6,106, with the employer covering the remainder. This makes employer-sponsored plans one of the most cost-effective options available.

Once you confirm that your employer offers health insurance, the next critical step is to compare coverage options. Most employers provide multiple plans, such as Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), or High-Deductible Health Plans (HDHPs). Each plan has different costs, networks, and coverage levels. For instance, an HMO typically has lower premiums but requires you to stay within a specific network of providers, while a PPO offers more flexibility but at a higher cost. If you’re under 30 and generally healthy, an HDHP paired with a Health Savings Account (HSA) might be a smart choice, as it allows you to save pre-tax dollars for medical expenses.

When comparing plans, pay close attention to key details like deductibles, copayments, and out-of-pocket maximums. A plan with a low monthly premium might seem appealing, but if it has a high deductible or limited coverage for prescriptions, it could end up costing you more in the long run. Use your employer’s benefits portal or consult with a Human Resources representative to access plan summaries and cost estimators. For example, if you take regular medications, ensure the plan covers them at a reasonable copay. Similarly, if you have a chronic condition, prioritize plans with lower specialist visit costs.

A practical tip is to evaluate your healthcare usage over the past year to predict future needs. If you rarely visit the doctor, a plan with a higher deductible and lower premiums might suit you. Conversely, if you have frequent medical needs, a plan with higher premiums but lower out-of-pocket costs could save you money. Additionally, consider whether the plan includes preventive care services at no cost, as required by the Affordable Care Act. This can help you avoid unexpected expenses for routine check-ups or screenings.

Finally, don’t overlook the value of additional benefits often bundled with employer-sponsored plans, such as dental, vision, or mental health coverage. These can provide comprehensive protection without the need for separate policies. Some employers also offer wellness programs or discounts on gym memberships, which can indirectly reduce healthcare costs by promoting better health. By thoroughly examining your employer’s offerings and aligning them with your needs, you can secure affordable health insurance that fits your budget and lifestyle.

Direct Billing: How Medical Insurance Claims Work

You may want to see also

Explore related products

![]()

Short-Term Health Plans: Consider temporary, low-cost plans for immediate coverage needs

Short-term health plans are a lifeline for those in transitional phases of life, offering immediate coverage at a fraction of the cost of traditional insurance. Designed to bridge gaps in coverage—such as during job changes, waiting periods for employer-sponsored plans, or post-graduation—these plans typically last 1–12 months, with some states allowing extensions up to 36 months. For instance, a 30-year-old in Texas might pay $100–$200 monthly for a short-term plan, compared to $300–$500 for a comprehensive ACA plan. This affordability makes them an attractive option for healthy individuals who need temporary protection against unexpected medical expenses.

However, short-term plans are not without limitations. They often exclude pre-existing conditions, preventive care, prescription drugs, and maternity care. For example, a plan might cover emergency room visits but deny coverage for a chronic condition like asthma. Additionally, they do not meet ACA requirements, meaning enrollees may face tax penalties in states with individual mandates. Before signing up, carefully review the policy’s exclusions and ensure it aligns with your immediate health needs. Pro tip: Use online comparison tools like eHealth or HealthPocket to evaluate premiums, deductibles, and coverage limits across providers.

To maximize the value of a short-term plan, pair it with supplementary coverage options. Health savings accounts (HSAs) can offset out-of-pocket costs, while critical illness or accident insurance can provide lump-sum payouts for specific events. For instance, a $5,000 deductible on a short-term plan might feel less daunting if you have an HSA balance or accident policy to draw from. Additionally, maintain a healthy lifestyle to minimize the risk of needing care not covered by the plan. Regular exercise, balanced nutrition, and preventive screenings can reduce the likelihood of unexpected medical issues.

Despite their limitations, short-term plans serve a critical role in the insurance landscape. They are particularly useful for young adults, early retirees, or gig workers who need flexibility and affordability. For example, a 25-year-old freelancer might opt for a $150/month short-term plan with a $10,000 deductible, knowing they’re unlikely to require extensive medical care. The key is to treat these plans as a stopgap, not a long-term solution. Once your circumstances stabilize, transition to a comprehensive plan that offers broader protection. Short-term plans are a tool—use them strategically to stay covered without breaking the bank.

Medical Malpractice: Insurance and Your Right to Redress

You may want to see also

Explore related products

$8

![]()

Health Savings Accounts (HSAs): Use tax-advantaged accounts to save for medical expenses

Health Savings Accounts (HSAs) offer a triple tax advantage: contributions are tax-deductible, funds grow tax-free, and withdrawals for qualified medical expenses are also tax-free. This unique structure makes HSAs a powerful tool for managing healthcare costs, especially for those with high-deductible health plans (HDHPs). Unlike Flexible Spending Accounts (FSAs), HSAs are not "use-it-or-lose-it"; unused funds roll over indefinitely, allowing you to build a substantial savings cushion for future medical needs.

To maximize an HSA’s benefits, start by contributing the annual maximum allowed by the IRS ($3,850 for individuals and $7,750 for families in 2023, with an additional $1,000 catch-up contribution for those over 55). Treat your HSA as an investment account, not just a savings account. Many providers offer investment options like mutual funds or ETFs, enabling long-term growth. For example, if you contribute $3,850 annually and achieve a 7% annual return, your account could grow to over $100,000 in 20 years, even without additional contributions.

While HSAs are designed for medical expenses, they can also serve as a retirement savings vehicle. After age 65, you can withdraw funds for non-medical expenses without penalty, though you’ll pay income tax on those withdrawals. This flexibility makes HSAs a versatile tool for both healthcare and retirement planning. However, be cautious about using HSA funds for non-qualified expenses before age 65, as you’ll face a 20% penalty plus income tax.

To make the most of your HSA, pair it with a high-deductible health plan (HDHP), which typically has lower monthly premiums than traditional plans. For instance, if you save $200 monthly on premiums by choosing an HDHP, redirect that money into your HSA. Over time, this strategy can offset out-of-pocket costs while building a tax-advantaged safety net. Additionally, keep detailed records of medical expenses to ensure you only withdraw HSA funds for qualified expenses, preserving the tax benefits.

Finally, consider using your HSA to pay for preventive care, such as vaccinations or annual check-ups, which are often covered by HDHPs without meeting the deductible. By paying out of pocket and saving receipts, you can reimburse yourself later, allowing your HSA funds to continue growing tax-free. This approach not only maximizes the account’s potential but also ensures you’re prepared for unexpected medical costs down the line. With strategic planning, an HSA can transform the way you afford and manage health insurance.

Who Really Controls Insurance Companies: Owners, Regulators, or Shareholders?

You may want to see also

Frequently asked questions

Many low-income individuals qualify for government programs like Medicaid or subsidies through the Affordable Care Act (ACA) marketplace. Check your eligibility for these programs to reduce or eliminate costs.

You can explore plans on the ACA marketplace, where you may qualify for premium tax credits based on your income. Alternatively, consider short-term health plans or health-sharing ministries as temporary options.

Yes, you can lower premiums by choosing a higher deductible plan, comparing plans during open enrollment, or qualifying for subsidies through the ACA marketplace. Additionally, maintaining a healthy lifestyle may reduce long-term costs.