Health insurance rates are determined through a complex process that considers multiple factors, including an individual's age, location, lifestyle, medical history, and the type of coverage selected. Insurance companies use actuarial data to assess risk, predicting the likelihood and cost of future medical claims, which directly influences premium pricing. Additionally, state and federal regulations, such as the Affordable Care Act, play a significant role in setting minimum coverage standards and capping certain costs. Market competition, administrative expenses, and the overall health of the insured population also contribute to rate calculations, making premiums vary widely across individuals and regions. Understanding these factors can help consumers make informed decisions when choosing a health insurance plan.

Explore related products

What You'll Learn

- Age and Health Status: Premiums increase with age and pre-existing conditions

- Location and Provider Network: Regional costs and available providers impact rates

- Coverage Level: Higher benefits and lower deductibles mean higher premiums

- Lifestyle Factors: Smoking, occupation, and BMI can affect insurance costs

- Policy Type: Individual, family, or group plans have different rate structures

![]()

Age and Health Status: Premiums increase with age and pre-existing conditions

Health insurance premiums are not arbitrary; they are meticulously calculated based on factors that predict future healthcare costs. Among these, age and health status stand out as primary determinants. As individuals age, their risk of developing chronic conditions and requiring medical interventions increases, prompting insurers to adjust premiums accordingly. For instance, a 60-year-old may pay two to three times more than a 25-year-old for the same coverage, reflecting the higher likelihood of hospitalizations, prescriptions, and specialist visits.

Pre-existing conditions further complicate this equation, often leading to higher premiums or even policy exclusions. Insurers assess conditions like diabetes, hypertension, or heart disease as indicators of future claims. For example, a 45-year-old with uncontrolled diabetes might face premiums 50% higher than a peer without such a condition. This pricing strategy, while controversial, is rooted in actuarial science, aiming to balance risk across the insured pool. However, it underscores the importance of early health management to mitigate long-term financial impacts.

The interplay between age and pre-existing conditions creates a double-edged sword for older individuals. A 55-year-old with arthritis and high cholesterol will likely face steeper premiums than a younger person with the same conditions. This is because age amplifies the severity and cost of managing chronic illnesses. To navigate this, individuals should prioritize preventive care, such as annual check-ups and lifestyle modifications, to delay or avoid the onset of costly conditions.

Practical steps can help manage these escalating costs. For older adults, exploring Medicare options or employer-sponsored retiree plans can provide more affordable coverage. Those with pre-existing conditions should compare policies carefully, focusing on out-of-pocket maximums and prescription drug coverage. Additionally, leveraging health savings accounts (HSAs) or flexible spending accounts (FSAs) can offset expenses. Ultimately, understanding the age-health premium link empowers individuals to make informed decisions and advocate for their financial and physical well-being.

Moving? Here’s How to Seamlessly Switch Your Health Insurance Plan

You may want to see also

Explore related products

![]()

Location and Provider Network: Regional costs and available providers impact rates

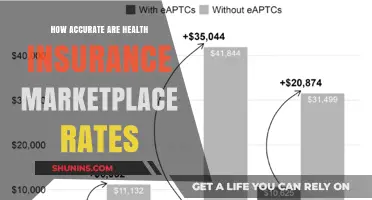

Health insurance rates are not uniform across the country; they fluctuate significantly based on where you live. Regional costs of living, healthcare utilization patterns, and the prevalence of certain medical conditions all play a role in determining premiums. For instance, urban areas with higher living expenses and greater demand for medical services often see steeper insurance rates compared to rural regions. In states like California or New York, where healthcare costs are among the highest in the nation, residents can expect to pay more for coverage than those in states like Mississippi or Alabama. This geographic disparity highlights the importance of understanding how location directly influences the price of health insurance.

Consider the provider network available in your area—it’s a critical factor in rate determination. Insurance companies negotiate contracts with healthcare providers to form networks, and the size, quality, and accessibility of these networks vary widely by region. In areas with a limited number of providers, insurers may face higher costs to secure contracts, which are then passed on to policyholders in the form of higher premiums. Conversely, regions with a competitive healthcare market often benefit from lower rates as insurers vie for customers by offering more affordable plans. For example, a metropolitan area with multiple hospitals and specialists may have lower rates compared to a rural area with only one healthcare facility.

To illustrate, imagine two individuals of the same age and health status, one living in Miami and the other in Des Moines. The Miami resident might face premiums 30-50% higher due to the region’s elevated healthcare costs and higher utilization rates. Additionally, if the Miami resident’s plan has a narrow provider network, they may have fewer options for care, potentially leading to out-of-network expenses. In contrast, the Des Moines resident could benefit from a broader network and lower overall costs, even if the plan’s coverage is comparable. This example underscores how location and provider networks are intertwined in shaping insurance rates.

When selecting a health insurance plan, it’s essential to evaluate both the regional cost environment and the provider network’s adequacy. Start by researching the average healthcare costs in your area and comparing them to national benchmarks. Next, scrutinize the provider network of each plan you’re considering. Ensure it includes hospitals, specialists, and primary care physicians that are conveniently located and meet your specific needs. For those with chronic conditions, confirming that preferred providers are in-network can prevent unexpected out-of-pocket expenses. Finally, consider using tools like Healthcare.gov or state-based exchanges to filter plans by provider network and cost, making it easier to find a balance between affordability and accessibility.

In conclusion, location and provider networks are pivotal in determining health insurance rates, with regional costs and available providers creating significant variations. By understanding these dynamics, individuals can make informed decisions that align with their healthcare needs and financial constraints. Whether you’re in a high-cost urban area or a more affordable rural region, taking the time to analyze these factors can lead to substantial savings and better access to care.

Sacramento's Uninsured: Understanding the Scope of Health Coverage Gaps

You may want to see also

Explore related products

![]()

Coverage Level: Higher benefits and lower deductibles mean higher premiums

Health insurance premiums are a direct reflection of the coverage level you choose, with a simple trade-off at play: more comprehensive benefits and lower out-of-pocket costs typically result in higher monthly payments. This relationship is a fundamental aspect of insurance pricing, allowing individuals to tailor their plans to their healthcare needs and financial capabilities. For instance, consider a scenario where two individuals, both aged 30, opt for different health insurance policies. Person A selects a plan with a $500 deductible, 80% coinsurance, and a $5,000 out-of-pocket maximum, while Person B chooses a more basic plan with a $2,000 deductible, 70% coinsurance, and a $7,000 out-of-pocket limit. The former will likely face a significantly higher premium due to the insurer's increased financial risk and the policy's richer benefits.

Understanding the Trade-Off: Benefits vs. Premiums

The correlation between coverage level and premiums can be understood through the lens of risk distribution. Insurance companies assess the potential costs of covering an individual's healthcare expenses and spread this risk across their policyholders. When you opt for higher benefits, such as lower deductibles and copayments, the insurer anticipates more frequent and substantial payouts. To compensate for this increased financial exposure, they charge higher premiums. Conversely, plans with higher deductibles and out-of-pocket costs shift more financial risk to the policyholder, resulting in lower monthly premiums. This dynamic is particularly evident in high-deductible health plans (HDHPs), which often have lower premiums but require individuals to pay more before insurance coverage kicks in.

Customizing Your Coverage: A Practical Approach

To navigate this trade-off effectively, consider your healthcare utilization patterns and financial situation. If you have a chronic condition requiring regular specialist visits and prescriptions, a plan with lower deductibles and copayments might be more cost-effective in the long run, despite higher premiums. For instance, a diabetic individual may benefit from a plan that covers insulin and frequent doctor visits with minimal out-of-pocket costs. On the other hand, if you're generally healthy and rarely visit the doctor, a high-deductible plan paired with a Health Savings Account (HSA) could provide substantial savings on premiums while still offering protection against catastrophic events.

The Impact of Age and Health Status

It's worth noting that age and health status can further influence the relationship between coverage level and premiums. Older individuals or those with pre-existing conditions may find that the additional benefits of a more comprehensive plan outweigh the higher premiums, as they are more likely to utilize healthcare services. For example, a 55-year-old with arthritis might prioritize a plan with low specialist visit copays and comprehensive prescription drug coverage. In contrast, a young, healthy adult may opt for a more basic plan, accepting higher deductibles in exchange for lower monthly costs.

In summary, the coverage level you select is a critical factor in determining your health insurance rates. By understanding the direct relationship between benefits, deductibles, and premiums, individuals can make informed choices that balance their healthcare needs and financial constraints. This tailored approach ensures that your insurance plan provides the necessary protection without unnecessary costs, demonstrating the importance of a nuanced understanding of health insurance pricing.

Health Insurance Fines: Are They Still Enforced?

You may want to see also

Explore related products

![]()

Lifestyle Factors: Smoking, occupation, and BMI can affect insurance costs

Smoking is one of the most significant lifestyle factors influencing health insurance rates, and for good reason. Insurers view smokers as high-risk individuals due to the well-documented link between smoking and chronic illnesses such as cancer, heart disease, and respiratory disorders. Studies show that smokers pay, on average, 20% to 50% more for health insurance premiums than non-smokers. For example, a 40-year-old smoker might pay $400 monthly for a mid-tier plan, while a non-smoker of the same age and location could pay $280. Quitting smoking not only improves health but can also lead to lower premiums after a tobacco-free period, typically 12 months, is verified.

Occupation plays a less obvious but equally critical role in determining insurance costs. Jobs with higher physical risk, such as construction workers or firefighters, often result in higher premiums due to increased likelihood of injury or illness. Conversely, desk-bound professionals may face higher rates due to sedentary lifestyles contributing to obesity, diabetes, or cardiovascular issues. Some insurers offer discounts for occupations perceived as low-risk, like accountants or librarians. Understanding how your job is categorized by insurers can help you anticipate costs and explore workplace wellness programs that might offset these risks.

Body Mass Index (BMI) is another lifestyle factor insurers scrutinize, as it correlates with conditions like hypertension, type 2 diabetes, and joint disorders. A BMI above 30, classified as obese, can increase premiums by 15% to 25%. For instance, a 35-year-old with a BMI of 32 might pay $350 monthly, while someone with a BMI of 24 could pay $300. However, BMI isn’t the sole metric; some insurers consider waist circumference or body fat percentage for a more accurate health assessment. Maintaining a healthy weight through diet and exercise isn’t just beneficial for overall well-being—it’s a practical strategy to reduce insurance costs.

The interplay of these factors—smoking, occupation, and BMI—highlights the importance of proactive lifestyle management. For instance, a 45-year-old construction worker who smokes and has a BMI of 35 could face premiums exceeding $600 monthly. Conversely, a non-smoking librarian with a BMI of 22 might pay less than $250. Insurers often reward positive changes, such as smoking cessation or weight loss, with premium reductions after a qualifying period. By addressing these modifiable factors, individuals can take control of their health and insurance expenses, turning lifestyle choices into financial opportunities.

Contracting with Medical Insurers: A Guide for Businesses

You may want to see also

Explore related products

![]()

Policy Type: Individual, family, or group plans have different rate structures

Health insurance rates are not one-size-fits-all; they vary significantly based on the type of policy you choose. Individual, family, and group plans each have distinct rate structures, influenced by factors like risk pooling, administrative costs, and coverage scope. Understanding these differences is crucial for selecting a plan that aligns with your needs and budget.

Consider the mechanics of risk pooling in group plans, for example. Employers or organizations negotiate rates with insurers based on the collective health profile of their members. A group of 50 employees, where 80% are under 40 and have minimal health issues, will likely secure lower premiums than a smaller group with a higher proportion of older or chronically ill individuals. This economies-of-scale effect often makes group plans more affordable per person than individual plans. However, if you’re self-employed or your employer doesn’t offer coverage, you’ll face individual plan rates, which reflect your personal health risks and demographics.

Family plans introduce another layer of complexity. Insurers typically calculate rates based on the number of family members covered and their ages. For instance, adding a child under 18 to a family plan might increase the premium by 30–50%, while adding a spouse could double it. Some insurers cap family plan rates, ensuring that covering additional dependents beyond a certain number doesn’t further increase costs. This structure can be cost-effective for families but requires careful comparison with individual plans for each member.

When evaluating policy types, consider your life stage and health needs. A 25-year-old single professional might find an individual high-deductible plan with a monthly premium of $200 sufficient, while a family of four may opt for a comprehensive family plan at $1,200 per month to cover frequent pediatric visits and prescriptions. Group plans, often subsidized by employers, can reduce out-of-pocket costs significantly—sometimes by 50% or more—but may limit provider networks or coverage options.

To navigate these differences, start by assessing your health care usage and financial flexibility. If you’re healthy and rarely visit the doctor, an individual plan with a higher deductible might save you money. Families with children or chronic conditions may benefit from a family plan with lower copays and broader coverage. Group plans are ideal if available, but verify the network and benefits to ensure they meet your needs. Always compare premiums, deductibles, and out-of-pocket maximums across policy types to make an informed decision.

Granger Medical: Understanding Insurance Coverage and Your Options

You may want to see also

Frequently asked questions

Health insurance rates are determined by factors such as age, location, medical history, lifestyle (e.g., smoking), coverage level, and the type of plan chosen. Insurers also consider the overall health and claims history of the population they cover.

Yes, age significantly impacts health insurance rates. Older individuals typically pay higher premiums because they are statistically more likely to require medical care due to age-related health issues.

Under the Affordable Care Act (ACA), insurers cannot charge higher rates based on pre-existing conditions. However, in states without ACA protections or for certain plans, pre-existing conditions may still affect eligibility or costs.

Location affects rates due to differences in healthcare costs, state regulations, and the availability of medical providers. Urban areas with higher living costs often have higher premiums compared to rural areas.