Michigan's auto insurance rates are determined by a multitude of factors, including the state's no-fault insurance laws, which mandate personal injury protection (PIP) coverage, and high collision and auto theft rates. Additionally, Michigan has a file and use system, allowing insurance companies to set rates without regulation. The type of coverage selected, such as coordinated or uncoordinated policies, also impacts rates. Other factors include age, gender, driving record, credit score, vehicle type, and location.

Explore related products

![Life Insurance Policyholders Pocket Index 1902 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

What You'll Learn

![]()

Michigan's no-fault insurance laws

Michigan's No-Fault Insurance law was designed to help people injured in car accidents. It is a unique system that ensures car accident victims get the help they need promptly and without regard to fault.

The law was created by state lawmakers and came into effect on 1 October 1973. Before this, Michigan had been a tort liability state, but the system was hurting car accident victims rather than helping them. Seriously injured victims were being denied compensation or were systematically under-compensated. Lengthy delays forced victims to bear devastating financial burdens.

Under the No-Fault Insurance law, if you are injured in a car accident, your auto insurance company pays for your medical bills and lost wages, regardless of who was at fault for causing the crash. The benefits can include your reasonable and necessary medical expenses, up to three years of lost wages, $20 a day for services you cannot perform, benefits for your dependents if you are killed, and benefits for funeral and burial expenses.

The law also limits lawsuits so that benefits can be paid quickly.

In 2019, the Legislature made historic changes to the auto insurance law that affect every driver, including allowing PIP Choice for the first time. After 1 July 2020, drivers had to select whether to continue with "unlimited" coverage or cap their coverage at $50,000 (if enrolled in Medicaid), $250,000 or $500,000.

Michigan's No-Fault Insurance law provides unlimited lifetime coverage for medical expenses resulting from auto accidents. To ensure the financial stability of companies providing auto insurance in Michigan, the state Legislature created the Michigan Catastrophic Claims Association (MCCA) in 1978. The MCCA reimburses auto no-fault insurance companies for each Personal Injury Protection (PIP) claim paid over $580,000.

Auto Insurance Policy: Whose Name Matters?

You may want to see also

Explore related products

![]()

The type of coverage selected

For PIP, Michigan's No-Fault Law previously required unlimited coverage. However, as of July 2020, drivers can choose between different coverage levels: $50,000 for Medicaid recipients, $250,000, $500,000, or opting out entirely if on Medicare. While selecting a lower coverage amount may seem tempting to reduce costs, it is essential to consider the potential risks. Unlimited coverage is the only option that provides catastrophic injury coverage, ensuring access to the best medical treatment and specialists.

For BI, the minimum coverage requirements have increased over time. Before July 2, 2020, the law mandated a minimum of $20,000 per person and $40,000 per accident. Currently, drivers must carry a minimum of $250,000 per person and $500,000 per accident. However, attorneys recommend higher coverage of $500,000 per person and $1,000,000 per accident for added protection.

PPI in Michigan auto policies is mandatory and provides a minimum of $1,000,000 in coverage for damage caused to parked cars or other property within the state.

For PD, the minimum coverage required by law is $10,000. However, it is recommended to opt for higher coverage of at least $100,000, especially when travelling to other states with different insurance requirements.

In addition to the mandatory coverage types, Michigan offers several optional coverage types. These include collision coverage, comprehensive coverage, uninsured/underinsured motorist coverage, mini tort coverage, gap coverage, accidental death coverage, and more.

When selecting coverage types and amounts, it is crucial to consider your personal needs, budget, and potential risks. Consulting with an auto insurance agent can help you make informed decisions and choose the right coverage options.

Allstate Auto Insurance: Charging Options

You may want to see also

Explore related products

![]()

Age and gender

Age as a Factor

In Michigan, age significantly influences car insurance costs. Drivers aged 22 to 29 tend to pay the highest rates, with costs decreasing as drivers get older. Younger drivers in this age group face the highest average annual premium at $2,203. As drivers mature, rates typically decrease, with those aged 30 to 59 paying less, at an average of $1,924. Seniors aged 60 and above benefit from the lowest average premiums, at $1,763 annually. This trend reflects the notion that experience on the road leads to lower premiums.

Gender as a Factor

Although gender is not a determining factor in Michigan, it is worth noting that, in general, men are statistically more likely to engage in risky driving behaviour and are, therefore, riskier to insure. As a result, men often face higher insurance rates than women. However, this is not always the case, as other factors, such as credit score and driving record, also come into play. For example, a female driver with a poor credit score or a history of accidents may pay a higher rate than a male driver with a clean record and good credit.

U.S.A.A. Auto Insurance: Covering Family

You may want to see also

Explore related products

![]()

Driving record

A driver's record is a significant factor in determining the cost of car insurance in Michigan. A clean driving record can result in lower insurance rates, while accidents, tickets, and violations will suggest a higher risk and lead to increased costs.

Drivers with an at-fault accident on their record pay about 51% more than the state average for full coverage car insurance. A speeding ticket on a driving record can also have a significant impact on insurance rates, with premiums increasing by an average of 52% following a speeding ticket in Michigan. This is a substantial increase compared to other states.

Other traffic violations that can add points to a driving record and increase insurance costs in Michigan include disobeying a school crossing guard, traffic signal, or stop sign; failing to stop and provide identification at the scene of a crash (hit-and-run); failure to stop at a railroad crossing or school bus; failure to yield or show caution for emergency vehicles; fleeing or eluding a police officer; driving under the influence (DUI); and various other moving violations.

The severity and duration of the impact of driving violations on insurance rates depend on the specific violation. For example, a speeding ticket will stay on a driving record for two years in Michigan, while more serious violations, such as a DUI, will result in longer-lasting effects on insurance premiums.

Lenders Require Gap Insurance to Protect Borrowers

You may want to see also

Explore related products

![]()

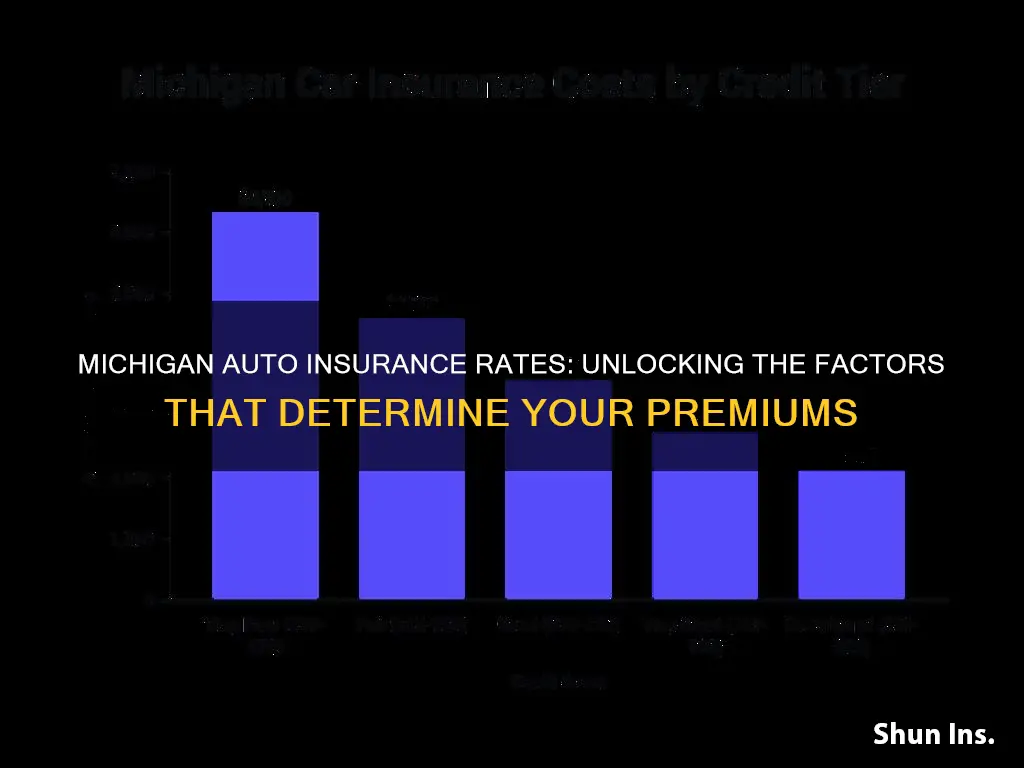

Credit score

Impact of Credit Scores on Auto Insurance Rates:

In most states, auto insurance companies use credit scores to assess an individual's risk of filing an insurance claim. This is known as "credit-based insurance scoring." The higher the credit score, the lower the insurance rate tends to be. Poor credit can significantly increase insurance rates, with drivers paying up to 114% more for full coverage.

Several factors contribute to credit-based insurance scores, including outstanding debt, credit history length, credit mix, and payment history. These factors are used to predict the likelihood of filing a claim, which helps insurance companies determine the potential risk and set the insurance rate accordingly.

Auto Insurance Rates in Michigan:

Michigan is one of the states that prohibit the use of credit scores in determining auto insurance rates. Instead, auto insurance companies in Michigan rely on other factors to set insurance rates. These factors include driving records, location, and other characteristics.

While credit scores are not directly considered in Michigan, there are still some indirect connections between credit and auto insurance rates. For example, auto insurance companies in Michigan can use credit scores to determine premium installment payment options. Additionally, individuals with no credit history may be considered similarly to those with poor credit by insurance companies, resulting in higher rates.

In conclusion, while credit scores do not directly impact auto insurance rates in Michigan, there are still some indirect connections between creditworthiness and the cost of auto insurance in the state.

GEICO Auto Insurance: Does Boat Rental Require Extra Coverage?

You may want to see also

Frequently asked questions

Auto insurance rates in Michigan are influenced by various factors, including the driver's age, driving history, vehicle type, coverage level, insurance history, and location. Other factors such as gender, credit score, and marital status may also play a role, depending on the insurance company.

Michigan's no-fault insurance system requires drivers to carry personal injury protection (PIP) coverage, which pays for medical expenses and other benefits for accident victims. This contributes to higher insurance rates in the state.

Michigan has a "file and use" system, which means insurance companies set their own rates without much regulation. This lack of regulation is often cited as a reason for the high cost of auto insurance in the state.

Michigan's auto insurance rates are among the highest in the nation. For example, the average annual premium for minimum coverage in Michigan is $856, while the national average is $595.