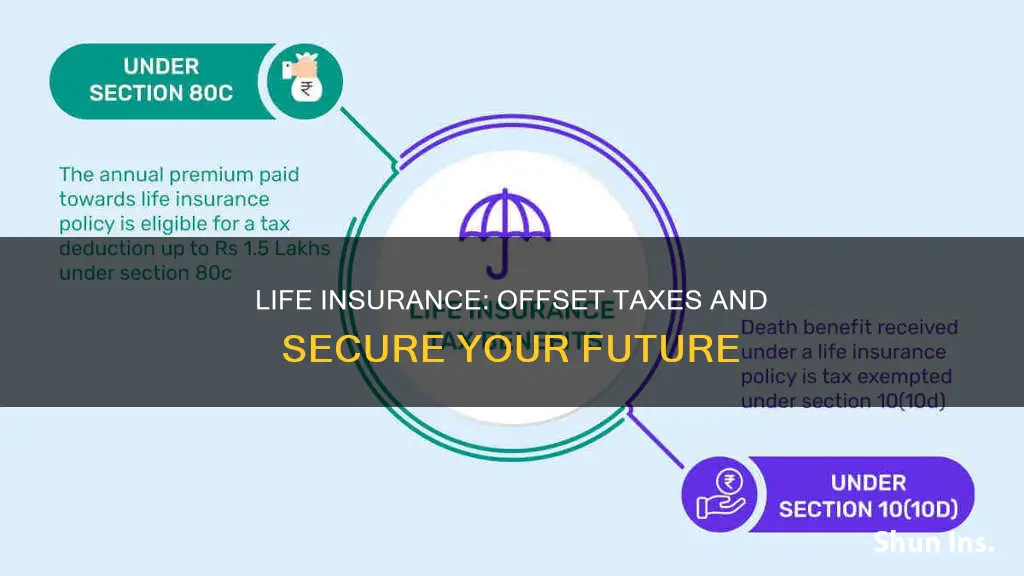

Life insurance is a valuable tool for financial planning, and it can be used to offset taxes in several ways. Firstly, life insurance payouts are generally not subject to income tax in Canada and the US, meaning beneficiaries receive tax-free proceeds. This is particularly advantageous as other financial accounts, such as IRAs, tax-deferred annuities, and qualified retirement plans, are often taxed. Secondly, permanent life insurance allows for tax-free cash withdrawals while the policyholder is alive, and any cash value accumulated grows tax-deferred. Thirdly, transferring ownership of a life insurance policy to a spouse or qualifying trust is typically a tax-free transaction, preserving the tax-deferred status of the policy. Finally, in the case of corporate-owned life insurance, businesses can deduct premiums when they use the policy as loan collateral or when they pay premiums on behalf of their employees. These features of life insurance policies can help individuals and businesses reduce their tax burden and maximise their financial benefits.

Explore related products

What You'll Learn

![]()

Life insurance payouts are generally not taxable

However, there are some exceptions. If you receive a payout in installments, any interest that accrues is taxable, though the principal death benefit is not. If you are receiving proceeds from an employer-paid life insurance policy, any death benefit beyond $50,000 is taxed as income. If your estate is the beneficiary of your life insurance policy, the death benefit may be subject to estate taxes.

If you are the policyholder and you surrender your life insurance policy, you will typically receive the cash surrender value, which is your policy's cash value minus any fees. You don't have to pay taxes on the principal when it's returned, but any cash value your policy has accrued will be taxed as income.

Life Insurance: Extreme Sports and Your Coverage

You may want to see also

Explore related products

$15.95

![]()

Death benefits are tax-free for beneficiaries

In most cases, beneficiaries do not need to pay taxes on their life insurance payout. This is true even if the death benefit is a large amount. However, there are a few exceptions to this rule.

If the death benefit is paid out in installments, any interest that accrues on the remaining portion will be taxable.

If the money is paid to the insured's estate instead of an individual or entity, it could be taxable. For example, in 2024, estates over $13.61 million will owe estate tax.

If the owner of the policy is not the same as the insured, the payout to the beneficiary could be considered a taxable gift.

Tips to avoid paying taxes on a life insurance payout

If you're concerned about taxes on a life insurance policy, there are a few things you can do:

- Transfer policy ownership. However, note that value beyond what was paid for the policy will be regarded as taxable. And if you transfer it within three years of your death, the IRS will treat it as though it still belongs to you.

- Create an irrevocable life insurance trust (ILIT). This removes the policy from your estate, but this kind of trust cannot be revoked after you set it up.

- Be aware of gift tax limits. The 2024 annual gift tax exemption is $18,000, and the lifetime exclusion amount is $13.61 million. If you’re careful that your policy's cash value does not exceed these limits, you may be able to avoid taxation.

If you fail to name a beneficiary on your life insurance policy, the money will be transferred to your estate when you die. It will then be up to a probate court to distribute your assets to your heirs, which could result in legal fees and other expenses that diminish the size of your estate.

Dialysis and Life Insurance: What's Covered and What's Not

You may want to see also

Explore related products

$12.99 $14.95

$1.99

![]()

Life insurance can be used to reduce tax on your final return

Secondly, certain types of life insurance policies, such as whole life insurance, offer tax-free growth while the policyholder is alive. This allows the cash value of the policy to grow without being subject to annual taxation, providing a larger sum to the beneficiaries upon the policyholder's death.

Thirdly, transferring ownership of a life insurance policy to a spouse or a qualifying trust is typically a tax-free transaction in Canada and the US bypassing estate taxes. This helps to preserve the policy's tax-deferred status. However, transferring ownership to someone other than a spouse or qualifying trust can trigger taxes on any accrued gains.

Additionally, in the US, life insurance proceeds can be removed from the taxable estate by creating an irrevocable life insurance trust (ILIT). By transferring ownership of the policy to an ILIT, the proceeds are no longer included as part of the estate, reducing the tax burden on heirs. It is important to note that the three-year rule applies to ownership transfers and ILITs, meaning that if the policyholder dies within three years of the transfer, the proceeds will be included in the estate and taxed accordingly.

Haven Life: Quick Insurance Payouts for Peace of Mind

You may want to see also

Explore related products

![]()

Policy surrender or lapse may be taxable

Surrendering or allowing a life insurance policy to lapse may result in tax consequences. If you surrender your policy, you will receive a cash surrender value, which is based on the policy's duration, growth, and assets. This amount can be taxable, depending on whether it exceeds the policy's basis or the amount paid in premiums.

There are several scenarios in which surrendering your policy may trigger tax consequences:

- You receive more funds than the policy's cost basis.

- You have outstanding policy loans that exceed the policy's cost basis.

- Your cost basis changed while you had the policy, such as reducing the death benefit or adding riders.

The tax rules provide that any gain from the surrender of a policy, to the extent that the cash surrender value plus any outstanding policy loans exceed the investment in the policy, will be taxed as ordinary income. It's important to consult with a tax expert to properly report any gains and understand the tax implications.

In some cases, rather than surrendering the policy, you may consider selling it. This is known as a life settlement and can sometimes result in a higher payout than the cash surrender value. If you sell a cash value life insurance policy to an unrelated third-party investor, any gain to the extent of the amount of the cash surrender value of the policy over the investment in the contract will be taxed as ordinary income. Any cash received above the cash surrender value will be taxed as long-term capital gains.

It's worth noting that the tax consequences of surrendering or lapsing a life insurance policy can vary depending on the type of policy and the specific circumstances. It's always recommended to consult with a tax professional or financial advisor before making any decisions regarding your life insurance policy.

Sun Life Insurance: Shingles Vaccine Coverage Explained

You may want to see also

Explore related products

![]()

Policy loans may be taxable

Policy loans are generally not taxable as income, as long as the policy remains in effect and the loan amount does not exceed the sum of the premiums paid. However, if the policy lapses or is surrendered with an outstanding loan, the loan amount may be subject to income tax. In such cases, the policyholder will have to pay taxes on any gains made through investments, and the outstanding loan will be deducted from the payout.

A policy loan is treated as a policy disposition, and if it exceeds the policy's adjusted cost basis (ACB), the excess amount is taxable. The ACB is the amount of premiums paid minus any distributions received. If the loan is taken in cash and does not exceed the ACB, the only result will be a reduction in the policy's ACB. However, if the loan exceeds the ACB, the excess will be taxed as income.

For example, let's consider Tasha, who owns a universal life policy with a cash surrender value (CSV) of $10,000 and an ACB of $5,000. If she takes out a policy loan of $4,000, the policy's ACB will be reduced to $1,000. If she takes another loan of $3,000 the following year, there will be a taxable gain of $2,000, and the ACB will be reduced to zero. At this point, she will have a $7,000 policy loan (excluding interest), $3,000 of net CSV, and an ACB of $0.

If a policy loan is subsequently repaid and the original loan was not taxable, the repayment is added to the policy's ACB. However, if any part of the loan resulted in a taxable gain, this amount can be deducted from the policyholder's income. In Tasha's case, if she repays the entire policy loan, she would be entitled to a $2,000 deduction, and the ACB would return to $5,000.

It's important to note that policy loans typically come with interest charges, and if the loan amount plus interest exceeds the policy's CSV, the policy may lapse. In such cases, the policyholder may need to pay additional money into the policy to keep it in force. Additionally, if there is an outstanding loan at the time of the policyholder's death, the loan amount will be deducted from the death benefit paid to the beneficiary.

While policy loans can provide easy access to funds, it is crucial to understand the potential tax implications and risks involved. Failure to repay the loan and interest can result in a reduced death benefit for beneficiaries and, in some cases, trigger taxable events.

Drunk Driving and Life Insurance: What's the Verdict?

You may want to see also

Frequently asked questions

Life insurance payouts are generally not taxable. Death benefits made directly to named beneficiaries are tax-free and do not need to be reported as income. However, policies that generate interest or dividend income, flow through an estate, offer a policy loan, or permit cash withdrawals may lead to tax consequences.

Naming primary and contingent beneficiaries ensures that your death benefit won't pass through your estate and be subject to probate fees.

In most cases, life insurance premiums are not tax-deductible for individuals or businesses. However, there are exceptions. For instance, if you use your policy as loan collateral or take out a policy loan and use the loan for business activities, the premiums may be deductible.

Transferring ownership to a spouse or qualifying trust is typically tax-free. However, transferring ownership to another individual or entity can trigger taxes on any accrued gains.