Life insurance is a topic that many people avoid thinking about, but it is important to understand the facts. There are many misconceptions about life insurance, including that it is too expensive and only necessary if you have children or other dependents. In reality, life insurance can be affordable, and it is worth considering even if you are young, single, and/or have no dependents. It is also important to understand that life insurance policies are designed to provide financial support for your loved ones after your death, so it is not something that will benefit you personally. Other common reasons people don't purchase life insurance include confusion about the variety of options available and a belief that they don't need it due to a healthy savings account or high-earning spouse. However, failing to get life insurance can be a gamble with your family's financial future.

| Characteristics | Values |

|---|---|

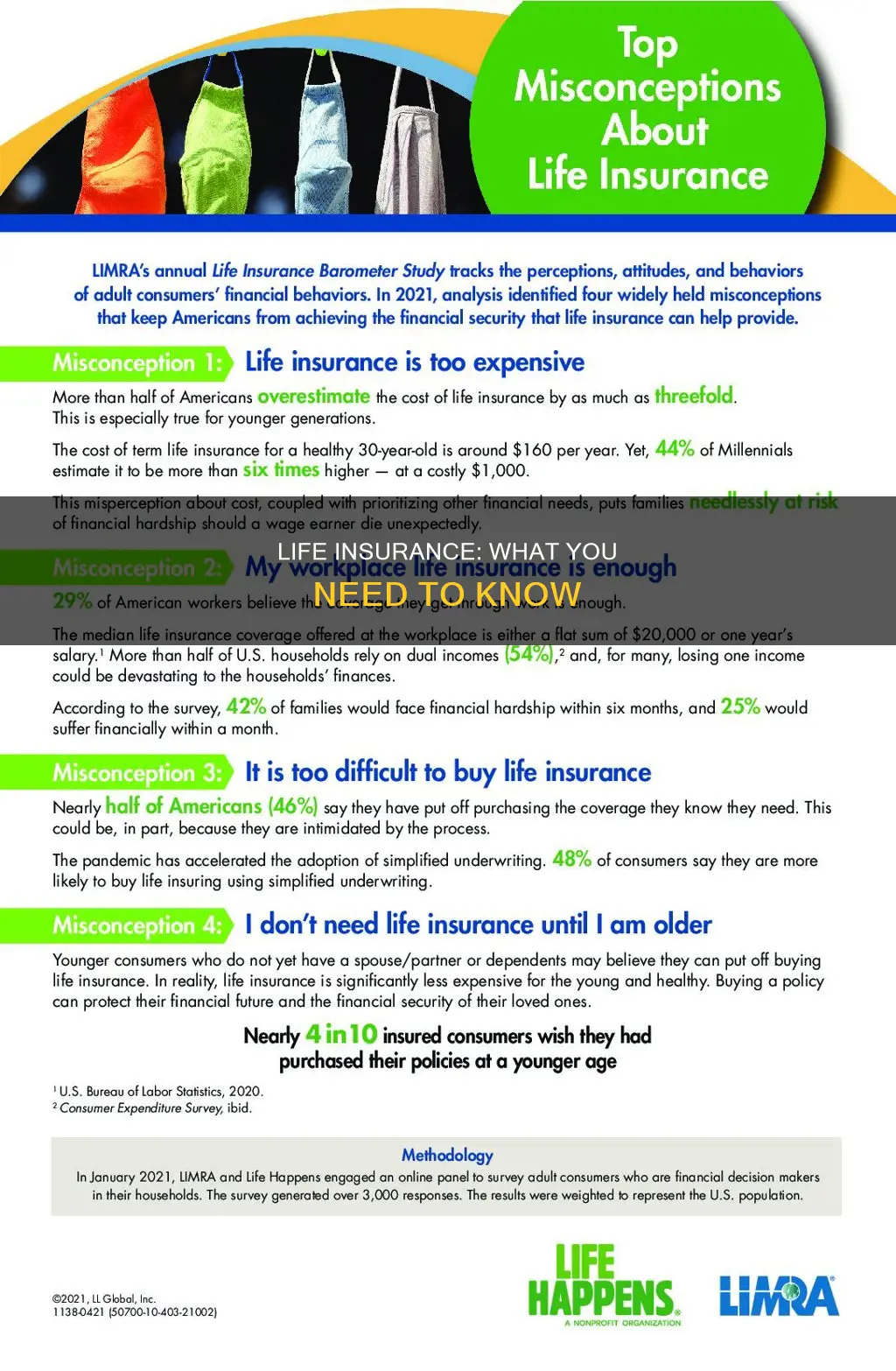

| People don't understand the cost of life insurance | Many people overestimate the cost of life insurance and believe that it is too expensive for them. |

| People don't understand the purpose of life insurance | People don't understand that life insurance is for the loved ones they leave behind, not themselves. |

| People don't understand their own needs | Some people believe they don't need life insurance because they have no dependents, or they have other plans to financially support their loved ones. |

| People don't understand the different types of life insurance | Many people are confused by all the varieties and options that are made available to them during the buying process. |

Explore related products

What You'll Learn

- People don't know how much their life insurance policy is worth

- Many don't know how much their beneficiaries will receive

- There are misconceptions about the flexibility of life insurance policies

- People don't understand the differences between term and permanent life insurance

- People don't know what life insurance money can be used for

![]()

People don't know how much their life insurance policy is worth

Many people don't know how much their life insurance policy is worth. This is often due to a lack of understanding of how much a life insurance policy costs in the first place. According to Todd Silverhart, Ph.D., corporate vice president at LIMRA Insurance Research, consumers "generally do not have a good understanding of how much a life policy might actually cost" and "tend to over-estimate the actual cost a lot". This is supported by statistics from the 2024 Insurance Barometer Study, which found that approximately 72% of participants overestimated the cost of a basic term life insurance policy.

There are a number of factors that determine the cost of a life insurance policy, including age, health, whether the individual is a smoker, the type of life insurance, and the size of the benefit. The older an individual is and the shorter their life expectancy, the more expensive their life insurance will be. Basic life insurance policies can provide beneficiaries with an amount that matches the policy owner's income or a percentage of it.

It is important to understand how much your life insurance policy is worth to ensure that your beneficiaries will be adequately provided for after your death. To calculate the amount of life insurance needed, individuals should consider their income, expenses, and financial dependents, as well as any existing assets, college funds, and current life insurance policies. By understanding the value of their life insurance policy, individuals can make informed decisions about their financial planning and ensure their loved ones are protected.

Additionally, it is worth noting that life insurance policies can be modified over time as an individual's financial situation and needs change. For example, young families often purchase life insurance to protect against the loss of the breadwinner, but as children grow up and become financially independent, the need for a large death benefit may decrease. Staying engaged with the policy and periodically reviewing its value and status can help individuals make necessary adjustments and ensure their life insurance continues to meet their needs.

Life Insurance License Renewal: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Many don't know how much their beneficiaries will receive

Life insurance is designed to provide financial support to beneficiaries after the policyholder's death. However, many people don't know how much their beneficiaries will receive, which can lead to confusion and delays in receiving benefits.

When purchasing life insurance, it is important to understand the different types of policies available and how they work. Term life insurance, for example, is only for a set period, such as 10, 20, or 30 years, and has no cash value component. On the other hand, whole life insurance offers more flexibility in how benefits are paid out but may be more expensive. The type of policy and the size of the benefit will impact the cost of premiums.

It is also important to keep beneficiaries informed about the policy and any changes. In most cases, beneficiaries are aware they are beneficiaries because the policyholder tells them ahead of time. However, policyholders may forget to provide all the necessary details, such as where to find the policy, the name and contact information of the insurance company, and the value of the policy. This can make it challenging for beneficiaries to claim their benefits, and tens of millions of dollars in death benefits go unclaimed each year as a result.

To avoid this, policyholders should communicate openly with their beneficiaries and provide them with the information they need to collect benefits. This includes the name of the insurance company, the location of the policy, and any other relevant details. Additionally, policyholders should regularly review and update their policies, especially after major life events such as the birth of a child or a divorce, to ensure that the appropriate beneficiaries are listed.

By understanding their policies and keeping their beneficiaries informed, policyholders can help ensure that their loved ones receive the full benefits of their life insurance policies without unnecessary delays or complications.

Understanding Life Insurance: Typical Division of Benefits

You may want to see also

Explore related products

$9.97 $19.99

$8

![]()

There are misconceptions about the flexibility of life insurance policies

Another misconception is that life insurance is too expensive. Most people overestimate the cost of life insurance, believing it to be an unaffordable luxury. However, the cost of life insurance depends on various factors, including age, health, coverage amount, and type of insurance. A healthy 30-year-old female, for example, can secure $250,000 of term life insurance for 20 years for around $20 per month, which is much less than most people think. Term life insurance, which is more affordable, can be a good option for those with a tight budget.

Some people also believe that they don't need life insurance if they have a healthy savings account, high-value investments, or a high-earning spouse. However, failing to get life insurance is a gamble with your family's financial future. Life insurance policies can pay out hundreds of thousands of dollars, which can help your loved ones cover monthly costs, debts, and end-of-life expenses. Additionally, life insurance can be used for various purposes, such as covering mortgage payments, keeping a business in the family, or paying for an elder's care.

Lastly, there is a misconception that life insurance is only necessary if you have children. While children are a common reason for people to get life insurance, it's important to consider other dependents or loved ones who would suffer financially from your loss. Life insurance can provide financial support and help ensure the well-being of those you care about, even if you don't have children.

Life Insurance Proceeds: Taxable in New York?

You may want to see also

Explore related products

![]()

People don't understand the differences between term and permanent life insurance

Term life insurance and permanent life insurance are the two main categories of life insurance. Term life insurance provides coverage for a specific period, typically 10 to 30 years. It is generally more affordable, with premiums that stay fixed during the term. This type of insurance is ideal for those who want to secure financial protection for their loved ones at a lower cost.

On the other hand, permanent life insurance offers lifelong coverage as long as the premiums are paid. It includes a death benefit and a cash value or savings benefit. The cash value grows over time and can be used for various purposes, such as low-interest loans, while the policyholder is still alive. Permanent life insurance usually has higher premiums than term life insurance because it funds the tax-free death benefit and the cash value account. This type of insurance is suitable for those who want coverage for their entire lives and are willing to pay a higher premium for the additional benefits.

The choice between term and permanent life insurance depends on individual needs and financial situations. Some factors to consider include the length of coverage needed, budget constraints, and the desire for wealth-building capabilities. It is important to understand these differences and seek advice from a financial advisor to determine which type of insurance is most suitable for one's unique circumstances.

Life Insurance Options for Rheumatoid Arthritis Patients

You may want to see also

Explore related products

![]()

People don't know what life insurance money can be used for

Life insurance is designed to provide financial support to people who would be at financial risk in the event of your death. However, many people don't know what life insurance money can be used for, and as a result, they may not consider purchasing it. Here are some common uses of life insurance money that people may not be aware of:

- Covering Final Expenses: Life insurance money can be used to cover the costs of final expenses, such as funeral services, burial or cremation, and other end-of-life medical bills. This can help alleviate the financial burden on loved ones during an already difficult time.

- Replacing Income: If the deceased was the primary breadwinner, life insurance money can be used to replace their income and support dependents. This includes covering daily living expenses, such as groceries, utilities, and rent or mortgage payments.

- Education Costs: Life insurance benefits can be used to cover a child's college tuition, room, and board. This can be especially beneficial for parents with young children who want to ensure their children's educational needs are met even after their death.

- Charitable Donations: Life insurance money can be used to make a substantial donation to a favorite charity or organization. This allows the deceased to leave a lasting legacy and support a cause they cared about.

- Living Benefits: Some life insurance policies offer living benefits, which provide financial support if the policyholder becomes terminally ill or disabled. This can include covering medical bills and other expenses, ensuring the policyholder can access funds while still alive.

- Mortgage Payments: Life insurance benefits can be used to pay off the remaining balance of a mortgage, lifting a financial burden from the beneficiaries.

While life insurance can offer financial security, it's important to note that it may not be necessary for everyone. Individuals without dependents or those with alternative financial plans in place may not require life insurance. Understanding personal needs and seeking professional advice can help determine if life insurance is the right choice.

Universal Life Insurance: Lump Sum Explained

You may want to see also

Frequently asked questions

Life insurance is not for the person who takes out the policy but for their loved ones. It is designed to provide financial support for beneficiaries after the plan owner’s death.

People often assume they don't need life insurance if they have no dependents, are single, or are retired. Others may have a healthy savings account or high-value investments, or their spouse is a high earner. Some also believe that life insurance is too expensive.

Even if you have no children or your children are grown up, there may be people in your life who depend on you financially, such as a sibling or spouse. Life insurance can also help pay for any debts you leave behind, like a mortgage, or end-of-life costs, such as funeral expenses.

The cost of life insurance depends on several factors, including your age, health, whether you smoke, the type of insurance, and how much coverage you want. However, people often overestimate the cost, and it can be more affordable than you think, especially if you are young and healthy.