Home insurance isn't a legal requirement in the US, but it is still essential for protecting your property, finances, and peace of mind. However, with insurance costs skyrocketing, more Americans are choosing to go without coverage. This decision could have devastating consequences, as homeowners expose themselves to serious financial risks if their homes are damaged or destroyed. While it may seem like an unnecessary expense, the data shows that the number of homeowners without insurance is falling, with 88% of homeowners covered, down from 95% a few years ago. This equates to more than 6 million homeowners nationwide who do not have insurance, including a disproportionately high number of Native American, Hispanic, and Black homeowners.

| Characteristics | Values |

|---|---|

| Home insurance coverage in the US | 88% (down from 95% a few years ago) |

| Number of homeowners without insurance | Over 6 million |

| Percentage of uninsured properties | 7.4% |

| Value of uninsured properties | $1.6 trillion |

| Percentage of Native American homeowners without insurance | 22% |

| Percentage of Hispanic homeowners without insurance | 14% |

| Percentage of Black homeowners without insurance | 11% |

| Owners of manufactured homes without insurance | 35% |

| Homeowners who inherited their homes without insurance | 29% |

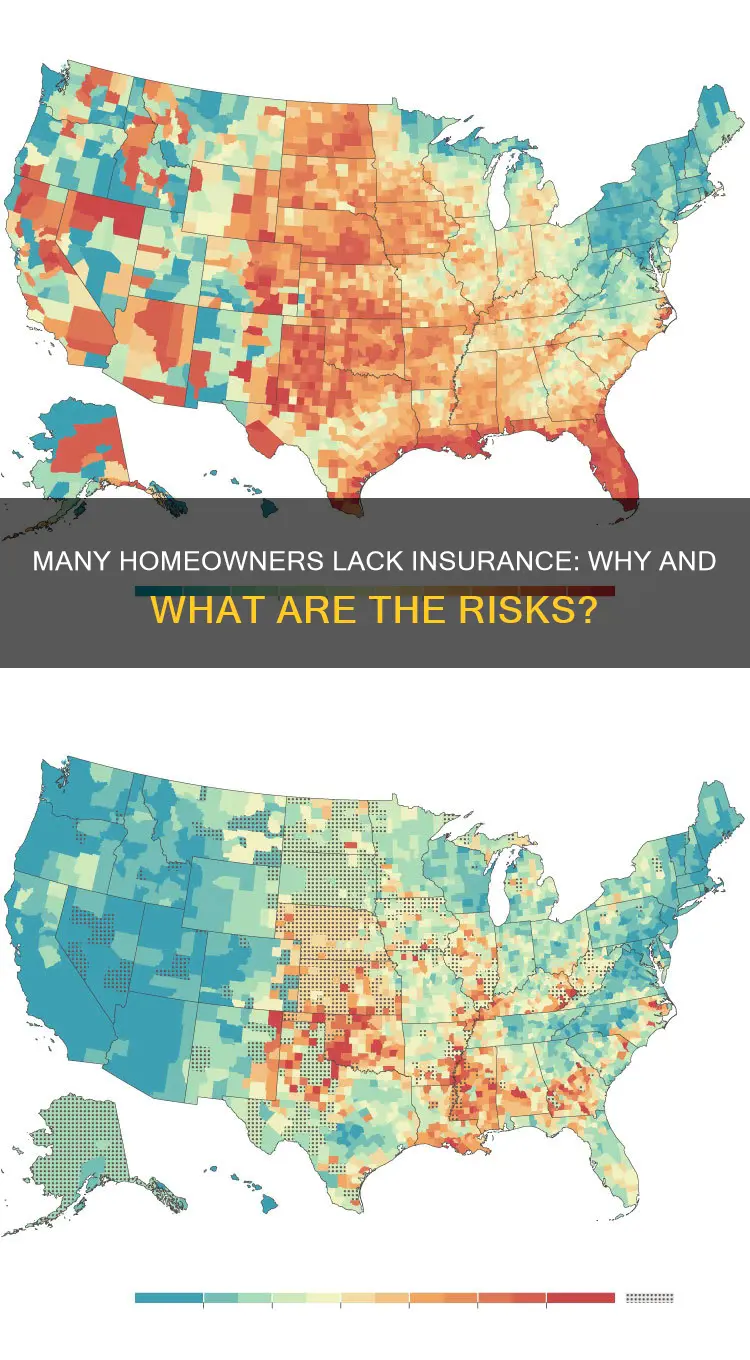

| States where residents are most likely to not have insurance | Mississippi, New Mexico, Louisiana |

| Cities where residents are most likely to not have insurance | Houston, Miami |

| Average annual insurance premium | Expected to exceed $2,500 |

| Average annual insurance premium in Florida | Expected to exceed $11,700 |

Explore related products

What You'll Learn

- Home insurance isn't legally required in the US, but mortgage lenders usually demand it

- Rising insurance costs are causing more people to skip home insurance

- Home insurance covers rebuilding costs after disasters, which can easily reach hundreds of thousands of dollars

- Home insurance covers liability costs if someone is injured on your property

- Home insurance isn't required after a mortgage is paid off, but it's still advisable

![]()

Home insurance isn't legally required in the US, but mortgage lenders usually demand it

Home insurance is not a legal requirement in the US. However, if you have a mortgage, your lender will likely mandate it as part of the loan agreement. This is due to the risks associated with loaning large sums of money. While it may not be legally required, the financial consequences of forgoing home insurance can be dire. Damage to your home can be expensive, and insurance provides financial protection from repair costs after a covered event. For example, a house fire or a dog bite could result in costly repair bills or legal fees, which would be covered by insurance.

Home insurance rates have been increasing rapidly, with some annual premiums exceeding $2,500. In states prone to hurricanes, wildfires, or tornadoes, such as Florida, rates can be significantly higher, with Florida residents expecting to pay over $11,700 per year. As a result, more Americans are opting to go without insurance, with an estimated 6 million homeowners nationwide, or 7.4% of all properties, currently uninsured. This trend is particularly prevalent among certain demographics, with higher rates of uninsured homeowners among Native American, Hispanic, and Black communities.

While forgoing insurance may seem like a way to save money, it is a risky gamble. If something happens to your home, you will be solely responsible for the potentially substantial costs of repairs or rebuilding. Additionally, if you have a mortgage and let your insurance lapse, your lender may purchase insurance on your behalf, which may only cover them and be more expensive than what you could obtain independently.

Overall, while home insurance may not be legally mandated in the US, it is generally a requirement for those with mortgages and provides essential financial protection for homeowners.

Farmers Insurance Availability in Montana: What You Need to Know

You may want to see also

Explore related products

![]()

Rising insurance costs are causing more people to skip home insurance

While home insurance is not a legal requirement in the US, it is still essential for protecting your property, finances, and peace of mind. However, rising insurance costs are causing more people to skip home insurance, leaving them vulnerable to financial risks.

Home insurance covers the costs of rebuilding or repairing a home in the event of disasters such as fires, floods, or storms, which can easily reach tens or hundreds of thousands of dollars. It also provides liability protection in case of accidents, injuries, or lawsuits, covering legal fees and medical bills.

The latest data shows a downward trend in the percentage of homeowners with insurance coverage, falling from over 95% a few years ago to 88% currently. This dip is attributed to the rapid increase in insurance prices, with some areas experiencing double-digit hikes. As a result, many homeowners are choosing to go without insurance to save money, especially those from lower-income backgrounds.

Certain demographics are disproportionately affected by the lack of insurance. For example, 22% of Native American homeowners, 14% of Hispanic homeowners, and 11% of Black homeowners have no insurance. Additionally, 35% of owners of manufactured homes and 29% of homeowners who inherited their homes are also uninsured. These disparities contribute to racial inequality and widen the long-standing racial wealth gap.

While skipping home insurance may provide short-term financial relief, it exposes homeowners to serious risks. Uninsured properties account for 7.4% of all properties in the country, leaving $1.6 trillion in property value unprotected. This not only impacts individual homeowners but also communities and the national housing stock.

As insurance costs continue to rise, it is crucial for homeowners to carefully consider their options and prioritize protecting their assets. While it may be tempting to forego insurance, the potential consequences of being uninsured can be financially devastating.

Home Insurance: Is It Mandatory?

You may want to see also

Explore related products

![]()

Home insurance covers rebuilding costs after disasters, which can easily reach hundreds of thousands of dollars

Home insurance isn't a legal requirement in the US, but it is still essential for protecting your most valuable asset. While it may be tempting to skip it to save money, this could be a costly mistake in the long run. Home insurance covers rebuilding costs after disasters, which can easily reach hundreds of thousands of dollars.

After a disaster, the cost to rebuild a home can skyrocket due to demand surge. There may be a shortage of local labour and a scarcity of raw materials, making it difficult and more expensive to ship them into a disaster zone. Price gouging, which is illegal, can also occur. As a result, rebuilding costs after a catastrophe can be significantly higher than before. For example, if a hurricane hits your neighbourhood and your home is a total loss due to wind damage, your insurer will only pay up to the policy limit. However, if prices for labour and materials have increased since you took out the policy, you may have to pay thousands of dollars out of your own pocket.

In some states, valued policy laws require insurers to pay out the full dwelling coverage amount in the event of a total loss, regardless of the actual cost to rebuild. These laws protect policyholders from underpayment, but they only apply under specific conditions and typically to losses caused by certain perils, such as fire. Most homeowners' insurance policies are replacement cost policies, which means the dwelling coverage amount is based on the cost to rebuild your home from scratch using similar materials and workmanship at today's prices.

To ensure you have enough coverage, it's important to review your home's replacement cost annually and update your policy accordingly. Consider purchasing a guaranteed replacement cost endorsement, which will pay the total amount to rebuild your home, regardless of how much the costs exceed the coverage limit. Not all insurance companies offer this, so it's essential to discuss your options with your agent. Additionally, if your home is older, it may need to be upgraded to meet current building codes, which can be stricter and more expensive. Some insurance companies offer a "rebuilding ordinance or law coverage" rider to help with these upgrade costs.

While it may be tempting to skip home insurance to save money, this could leave you financially vulnerable in the event of a disaster. More than 6 million homeowners in the US, particularly those from minority backgrounds, do not have insurance, putting them at extreme risk of losing their homes and facing significant financial hardship. Home insurance provides crucial protection against these risks, covering the costs of rebuilding or repairing your home after a disaster.

Protect Your Home: AmFam Insurance for Peace of Mind

You may want to see also

Explore related products

![]()

Home insurance covers liability costs if someone is injured on your property

Home insurance isn't a legal requirement in the US, but it is still important to have it. Homeowners insurance costs have been rising, leading to more people considering dropping their coverage to save money. While this might be tempting, it is a risky move. Home insurance covers liability costs if someone is injured on your property, and without it, you could be facing a huge bill.

If someone is injured on your property, they may be able to sue for the cost of their medical bills and other injury-related costs, including attorney and court fees. If you are found liable, your personal liability coverage may help with these costs, up to the limits of your policy. This includes injuries caused by your dog, although certain breeds are excluded. It is important to check your policy carefully to understand what is and isn't covered.

Personal liability coverage also applies away from your home. For example, if you or a family member accidentally injure someone in a park, your homeowners liability insurance can help cover the person's medical bills and legal costs if you are sued. It can also cover damage to someone else's property, such as if your child breaks a neighbor's window.

However, personal liability coverage does not cover costs related to your injuries or the injuries of others in your household. If you cut your hand at home, for instance, your health insurer would cover the medical bills, not your homeowners liability insurance. It also doesn't cover injuries resulting from business activities or vehicle-related injuries, which would fall under your auto insurance policy.

While it might be tempting to skip home insurance to save money, it is a risky move. If something happens and you are found liable, you could be facing significant costs. As one expert notes, "Going bare [...] spells financial ruin for most homeowners."

Homeowner's Insurance: Does It Cover Stolen Utility Trailers?

You may want to see also

Explore related products

![]()

Home insurance isn't required after a mortgage is paid off, but it's still advisable

Home insurance is not a legal requirement in the US, even when paying off a mortgage. However, it is highly recommended that homeowners continue to insure their property and assets even after their mortgage is paid off.

Home insurance provides financial protection for your home and belongings and offers liability protection if someone is injured on your property. Without insurance, you could be sued, and your savings and investments could be at risk. While it may be tempting to cancel your policy to save money, especially considering the rapid increase in insurance prices, it is a risky move that could result in significant financial loss.

After paying off your mortgage, you may be able to save on insurance premiums by reviewing your coverage and ensuring it meets your needs. Some insurers offer discounts for homes that are mortgage-free, so it is worth contacting your insurance provider to discuss any potential savings.

It is important to remember that your home is likely your biggest asset, and protecting it should be a priority. While it may be tempting to "go bare" or "self-insure", as some homeowners choose to do, it is a gamble that could result in financial ruin if disaster strikes.

In conclusion, while home insurance may not be required after paying off your mortgage, it is a wise investment to protect your home, belongings, and assets. The financial peace of mind that comes with insurance is invaluable, and the potential savings on premiums for mortgage-free homes make it even more advisable.

Dave Ramsey's Take on Mortgage Insurance

You may want to see also

Frequently asked questions

Yes, it is becoming increasingly common for homeowners to go without insurance due to rising costs. A study by the Consumer Federation of America found that over 6 million homeowners, or 7.4% of all properties in the country, do not have insurance.

Experts attribute the rise in insurance costs to the effects of climate change and inflationary pressures. People moving to disaster-prone areas are also causing insurance prices to rise.

No, home insurance is not a legal requirement in the US. However, most homeowners have a mortgage, and mortgage lenders typically require homebuyers to have home insurance as part of the loan terms.

Without insurance, homeowners are exposed to serious financial risks. In the event of a fire, flood, or other disasters, the costs of repairing or rebuilding a home can be extremely high. Home insurance also typically covers personal belongings, so without insurance, homeowners would have to cover the cost of replacing lost or damaged items.

Yes, the Consumer Federation of America's study found that certain demographics of homeowners are disproportionately at risk. 22% of Native American homeowners, 14% of Hispanic homeowners, and 11% of Black homeowners are uninsured.