Health insurance tax credits can significantly impact your tax return by either reducing the amount of taxes you owe or increasing your refund. These credits, such as the Premium Tax Credit (PTC) under the Affordable Care Act, are designed to help lower- and middle-income individuals and families afford health insurance purchased through the Marketplace. If you qualify, the credit can be applied directly to your monthly premiums, reducing your out-of-pocket costs, or you can claim the full credit when filing your taxes. However, if you receive advance payments of the PTC, you must reconcile the amount received with the actual credit you qualify for on your tax return, which could result in owing additional taxes or receiving a larger refund depending on your income and circumstances. Understanding how these credits work is crucial for accurately filing your taxes and maximizing your financial benefits.

Explore related products

What You'll Learn

![]()

Eligibility requirements for health insurance tax credits

Health insurance tax credits can significantly reduce your out-of-pocket costs for health coverage, but not everyone qualifies. Eligibility hinges on a combination of income, household size, and access to other insurance options. Understanding these requirements is crucial to determining whether you can claim this valuable tax benefit.

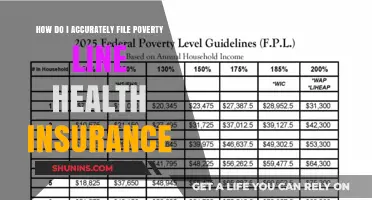

Health insurance tax credits, specifically the Premium Tax Credit (PTC), are designed to make health insurance more affordable for individuals and families with moderate incomes. To be eligible, your household income must fall within a specific range, generally between 100% and 400% of the federal poverty level (FPL). For 2023, this translates to an annual income of approximately $13,590 to $54,360 for an individual and $27,750 to $111,000 for a family of four. However, these figures can vary slightly depending on your state and family size.

Beyond income, your eligibility also depends on your access to other health insurance options. If you or a family member are offered affordable health insurance through an employer, you may not qualify for the PTC. "Affordable" is defined as coverage that costs no more than 9.83% of your household income for the employee's share of the premium. Additionally, you must not be eligible for coverage through a government program like Medicare, Medicaid, or the Children's Health Insurance Program (CHIP).

It's important to note that eligibility is determined on a year-by-year basis. Changes in your income, family size, or access to other insurance can affect your eligibility for the PTC in subsequent years. Therefore, it's essential to review your situation annually and update your information on the Health Insurance Marketplace to ensure you receive the correct amount of tax credit.

To apply for the PTC, you must enroll in a health insurance plan through the Health Insurance Marketplace. During the enrollment process, you'll provide information about your income, household size, and any other insurance options available to you. The Marketplace will then determine your eligibility and calculate the amount of tax credit you qualify for. This credit can be applied directly to your monthly premiums, reducing your out-of-pocket costs, or claimed when you file your federal tax return.

In conclusion, understanding the eligibility requirements for health insurance tax credits is essential for maximizing your potential savings on health coverage. By meeting the income and insurance criteria, you can take advantage of this valuable tax benefit and make health insurance more affordable for you and your family. Remember to review your eligibility annually and update your information on the Marketplace to ensure you receive the correct amount of tax credit.

Understanding Medical Insurance Credentialing: A Primer

You may want to see also

Explore related products

$0.99 $13.99

![]()

Calculating tax credit amounts and impact on returns

Health insurance tax credits can significantly reduce your out-of-pocket costs for premiums, but understanding how they’re calculated and their impact on your tax return requires a clear breakdown. The first step is determining your eligibility for the Premium Tax Credit (PTC), which depends on your household income relative to the federal poverty level (FPL). For 2023, individuals earning between 100% and 400% of the FPL qualify, though recent legislation has temporarily expanded eligibility to those earning above 400% of the FPL. Once eligibility is confirmed, the credit amount is calculated based on the difference between your expected contribution (a percentage of your income) and the cost of the second-lowest Silver plan in your area, known as the benchmark plan.

To illustrate, consider a family of four earning $60,000 annually in 2023. If their expected contribution is 9.12% of their income ($5,472), and the benchmark plan costs $12,000, their tax credit would be $6,528 ($12,000 - $5,472). This credit can be applied monthly to reduce premiums or claimed as a lump sum on your tax return. However, if you receive advance payments, reconciliation at tax time is crucial. Form 8962 is used to compare the advance credits received with the actual credit you qualify for, ensuring you neither owe additional taxes nor receive a refund for overpayment.

A common pitfall is underestimating income, which can lead to repaying excess credits. For instance, if your income increases mid-year but you don’t update your marketplace information, you may receive more advance credits than you’re entitled to. To avoid this, report income changes promptly and use the IRS’s Tax Credit Reduction Worksheet to estimate potential repayment limits, which are capped based on income level. For example, households earning up to 200% of the FPL have no repayment obligation for excess credits in 2023.

The impact of tax credits on your return extends beyond premium reduction. If you choose not to take advance payments, claiming the full credit on your return can result in a substantial refund. Conversely, if you’ve received advance payments exceeding your eligibility, you’ll owe the difference, though repayment limits apply. For instance, a single taxpayer earning 300% of the FPL would repay up to $1,650 for excess credits in 2023. Strategic planning—such as estimating income accurately and adjusting advance payments—can maximize benefits while minimizing tax-time surprises.

Finally, understanding the interplay between tax credits and other deductions is essential. Health insurance premiums paid out-of-pocket (after applying credits) may be deductible if you itemize and exceed 7.5% of your adjusted gross income. Additionally, self-employed individuals can deduct 100% of health insurance premiums, regardless of tax credits received. By carefully calculating credit amounts and considering their broader tax implications, you can optimize both your insurance costs and your return.

Switching to Medicaid: Removing Yourself from Private Insurance

You may want to see also

Explore related products

$13.9 $25

![]()

Advance payments vs. claiming credits at tax time

Health insurance tax credits can significantly impact your tax return, but the method of receiving them—advance payments or claiming at tax time—carries distinct implications. Advance payments of the Premium Tax Credit (PTC) reduce your monthly health insurance premiums throughout the year, providing immediate financial relief. However, this convenience comes with a trade-off: you must reconcile these payments on your tax return using Form 8962. If your actual income differs from the estimate used to calculate the advance payments, you may owe money or receive a smaller refund. For instance, if your income increases mid-year, you might have received more advance credit than you qualify for, creating a repayment obligation.

Claiming credits at tax time, on the other hand, requires paying full premiums upfront but offers greater control and predictability. This approach is ideal for those with stable, predictable incomes or those who prefer to avoid potential repayment surprises. By waiting to claim the PTC, you ensure the credit is based on your actual income for the year, not an estimate. This method also allows you to allocate the refund strategically, such as paying down debt or investing, rather than spreading the benefit across monthly premiums.

Consider a scenario where a self-employed individual estimates their income at $50,000 but ends the year at $65,000. If they received advance payments based on the lower estimate, they could face a repayment of up to $600, depending on their income level and filing status. Conversely, if they claimed the credit at tax time, the higher income would reduce the credit amount, but there would be no repayment risk. This example highlights the importance of accurately estimating income when choosing between advance payments and claiming later.

Practical tips for navigating this decision include monitoring income fluctuations throughout the year and updating your Marketplace account if your circumstances change. For those with variable income, claiming credits at tax time may be safer, as it eliminates the risk of overpayment. Conversely, individuals with fixed incomes or those needing immediate premium relief may benefit more from advance payments. Always consult IRS guidelines or a tax professional to ensure compliance and optimize your financial outcome.

In conclusion, the choice between advance payments and claiming credits at tax time hinges on your income stability, financial preferences, and risk tolerance. Advance payments offer immediate savings but require careful reconciliation, while claiming credits later provides accuracy and control. Understanding these nuances ensures you maximize the benefits of health insurance tax credits while minimizing potential pitfalls.

Get Free Medical Insurance: Tips and Tricks

You may want to see also

Explore related products

![]()

Penalties for overestimating or underestimating tax credits

Overestimating or underestimating health insurance tax credits can lead to penalties, repayment requirements, or missed benefits, depending on the direction and magnitude of the error. When you overestimate your eligibility for the Premium Tax Credit (PTC), the IRS may require you to repay all or part of the excess amount received during the year. For instance, if your income ends up higher than projected and you received $3,000 more in credits than you qualified for, you could owe that sum at tax time. Lower-income individuals may qualify for a repayment cap, but it’s not automatic—you must meet specific income thresholds to avoid full repayment.

Underestimating your tax credits, on the other hand, means leaving money on the table. If your actual income falls below your initial estimate, you may be entitled to a larger credit, which you can claim when filing your return. For example, if you projected an income of $50,000 but earned $45,000, the difference could translate to hundreds or even thousands in additional refundable credits. However, this scenario doesn’t incur penalties—only missed opportunities if you fail to reconcile the discrepancy on Form 8962.

The IRS uses a reconciliation process to compare your estimated credits with your actual eligibility based on year-end income. Overestimations trigger repayment demands, while underestimations result in refunds or reduced tax liability. For instance, a family of four earning $70,000 instead of the projected $60,000 might face a $1,200 repayment if they received excess credits. Conversely, if their income dropped to $55,000, they could claim an additional $800 in credits. Precision in income estimation is critical, as even small discrepancies can lead to financial surprises.

To minimize penalties or missed benefits, update your income projections with the Marketplace throughout the year whenever circumstances change—job loss, raises, or marriage, for example. If you’re self-employed or have variable income, consider conservative estimates to avoid overpayment risks. For instance, a freelancer might project 80% of their highest-earning year’s income to create a buffer. Additionally, consult a tax professional or use IRS tools like the Tax Withholding Estimator to refine your projections and avoid pitfalls.

Ultimately, understanding the consequences of miscalculating tax credits empowers you to navigate the system proactively. Overestimations can lead to unexpected debt, while underestimations forfeit financial aid. By staying vigilant, updating estimates, and leveraging available resources, you can optimize your tax return while avoiding penalties. Treat tax credit reconciliation as an ongoing process, not a year-end scramble, to ensure accuracy and maximize benefits.

Omnipod Dash Coverage: Which Insurance Companies Offer Support?

You may want to see also

Explore related products

![]()

Reporting health insurance tax credits on tax forms

Health insurance tax credits, such as the Premium Tax Credit (PTC), directly impact your tax return by either reducing the amount of tax you owe or increasing your refund. When reporting these credits on your tax forms, accuracy is crucial to avoid discrepancies that could trigger audits or delays in processing. The primary form for reporting health insurance tax credits is Form 8962, which reconciles the advance payments you received against the actual credit you qualify for based on your final income.

To begin reporting, gather all necessary documentation, including Form 1095-A, which details the health insurance coverage you purchased through the Marketplace. This form lists the monthly premiums and any advance payments applied to your plan. If you received advance payments, you must complete Form 8962 and attach it to your Form 1040. The process involves calculating the credit based on your household income, family size, and the cost of the second-lowest-cost Silver plan in your area. For example, if your household income is 200% of the federal poverty level, you may qualify for a higher credit, but the exact amount depends on the premium you paid.

One common pitfall is failing to reconcile advance payments correctly. If you underestimate your income and receive excess advance payments, you may owe the IRS the difference. Conversely, if you overestimate your income, you could be entitled to a larger credit, increasing your refund. For instance, a family of four with an income of $60,000 might receive $500 in advance payments monthly but qualify for $600 based on their final income, resulting in an additional $1,200 refund. To avoid errors, use the IRS’s instructions for Form 8962 and consider consulting a tax professional if your situation is complex.

Reporting health insurance tax credits also requires attention to detail regarding changes in circumstances. If you experienced income fluctuations, marriage, divorce, or the birth of a child during the tax year, these events can affect your eligibility and credit amount. For example, a single taxpayer earning $30,000 who marries mid-year and combines income with a spouse earning $40,000 must recalculate their credit based on the new household income. Failure to report such changes can lead to penalties or underpayment of taxes.

Finally, keep in mind that the rules for reporting health insurance tax credits can change annually due to legislative updates or adjustments to the federal poverty level. Staying informed about these changes ensures compliance and maximizes your tax benefits. For instance, the American Rescue Plan Act of 2021 expanded eligibility for the PTC, allowing more individuals to qualify for assistance. By carefully following the reporting guidelines and staying updated on tax laws, you can navigate the complexities of health insurance tax credits with confidence.

Life Insurance: Can You Sell When Seriously Ill?

You may want to see also

Frequently asked questions

A health insurance tax credit, such as the Premium Tax Credit (PTC), is a subsidy that helps lower your health insurance premiums. If you received advance payments of the PTC, you must reconcile the amount on your tax return using Form 8962. This may result in a smaller refund or a higher tax liability if the advance payments were too high.

You may qualify for a health insurance tax credit if you purchase coverage through the Marketplace, meet income requirements, and aren’t eligible for other affordable coverage. If you claim the credit, it reduces your taxable income, potentially lowering your overall tax liability. However, you must report it accurately to avoid penalties.

Yes, if you qualify for the Premium Tax Credit and didn’t receive advance payments, claiming the full credit on your tax return can increase your refund. Conversely, if you received too much in advance payments, you may owe money, reducing your refund or increasing your tax bill.

Failing to reconcile your health insurance tax credit using Form 8962 can result in delays in processing your return, penalties, or ineligibility for advance payments in future years. It’s crucial to accurately report and reconcile the credit to avoid these issues.