Filing for health insurance under the poverty line can be a critical step for individuals and families who need affordable healthcare coverage. To accurately navigate this process, it is essential to understand the eligibility criteria, which typically include income thresholds based on the Federal Poverty Level (FPL). Applicants must gather necessary documentation, such as proof of income, residency, and household size, to demonstrate their financial situation. Depending on the state, this may involve applying through the Health Insurance Marketplace or directly through Medicaid, as eligibility and procedures can vary. Additionally, seeking assistance from local healthcare navigators or community organizations can provide valuable guidance to ensure the application is completed correctly and submitted on time, maximizing the chances of approval for much-needed health coverage.

| Characteristics | Values |

|---|---|

| Eligibility Criteria | Varies by state; generally based on household income and family size. |

| Income Threshold | Federal Poverty Level (FPL) guidelines (e.g., 100-138% FPL for Medicaid). |

| Application Process | Online via Healthcare.gov, state Medicaid websites, or in-person. |

| Required Documents | Proof of income, citizenship/immigration status, and household size. |

| Coverage Types | Medicaid, Children’s Health Insurance Program (CHIP), or subsidized plans. |

| Enrollment Period | Year-round for Medicaid; Open Enrollment for Marketplace plans (Nov 1–Jan 15). |

| Cost | Often $0 premiums for those below poverty line; subsidies available. |

| Renewal Process | Annual redetermination of eligibility required. |

| State Variations | Eligibility and benefits differ by state (e.g., Medicaid expansion states). |

| Additional Benefits | May include dental, vision, and mental health services depending on plan. |

| Latest Data Source | Healthcare.gov, CMS (Centers for Medicare & Medicaid Services), 2023 FPL guidelines. |

Explore related products

What You'll Learn

- Eligibility Criteria: Understand income limits, household size, and state-specific requirements for poverty line health insurance

- Application Process: Gather documents, complete forms, and submit via online portals or local offices

- Coverage Details: Learn benefits, exclusions, and preventive care services included in the insurance plan

- Renewal Procedures: Track deadlines, update income information, and reapply annually to maintain coverage

- Appeals & Assistance: Navigate denials, seek help from navigators, or file appeals for incorrect decisions

![]()

Eligibility Criteria: Understand income limits, household size, and state-specific requirements for poverty line health insurance

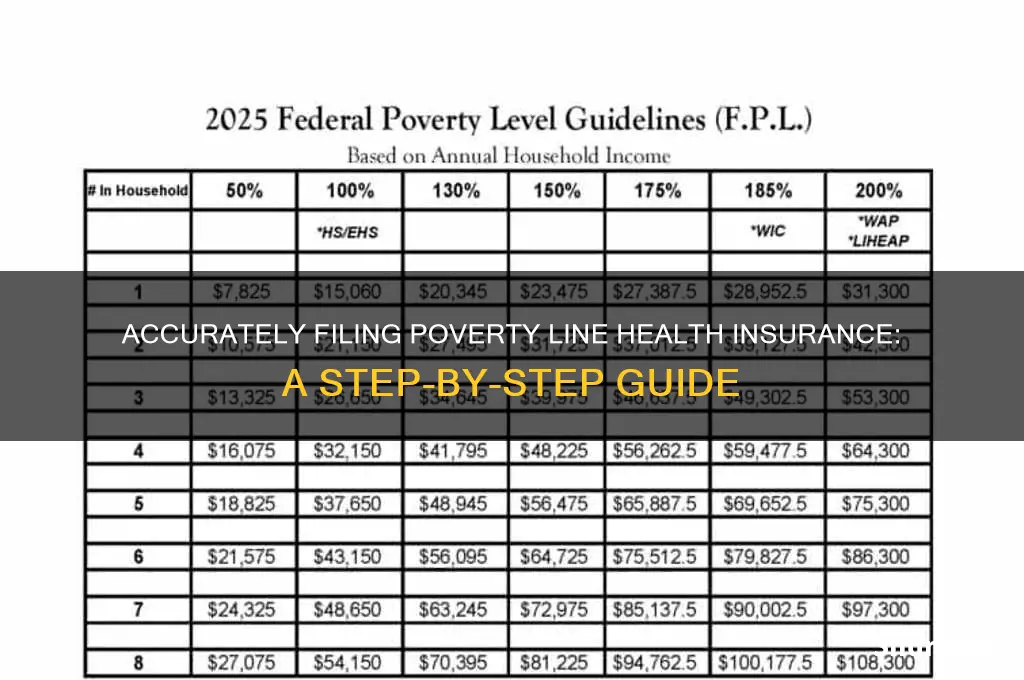

To accurately file for poverty line health insurance, understanding eligibility criteria is paramount. Income limits are the cornerstone of this process, as they determine whether you qualify for programs like Medicaid or the Children’s Health Insurance Program (CHIP). These limits are typically set at a percentage of the Federal Poverty Level (FPL), which varies annually. For instance, in 2023, a single individual earning up to 138% of the FPL may qualify for Medicaid in states that expanded coverage under the Affordable Care Act. However, non-expansion states often have stricter limits, sometimes as low as 50% of the FPL. Calculating your income against these thresholds is the first step in determining eligibility.

Household size plays a critical role in this calculation, as it directly impacts the income limit applicable to your situation. For example, a family of four in 2023 would need to earn below 262% of the FPL to qualify for CHIP in some states. Each additional household member increases the income threshold, but it also complicates the filing process. Dependents, spouses, and even non-related individuals living together may be counted, depending on state rules. Accurately listing all household members and their income sources is essential to avoid discrepancies that could delay or disqualify your application.

State-specific requirements add another layer of complexity to eligibility. While federal guidelines provide a framework, states have significant leeway in setting their own rules. For instance, some states require asset tests, where your savings, property, or investments are evaluated alongside income. Others may impose work requirements or mandate specific documentation, such as proof of citizenship or residency. Researching your state’s Medicaid or CHIP website is crucial, as it provides detailed instructions tailored to local regulations. Ignoring these nuances could lead to an incorrect filing, wasting time and effort.

Practical tips can streamline the eligibility assessment process. Start by gathering all necessary documents, including pay stubs, tax returns, and proof of household size. Use online calculators provided by healthcare.gov or state agencies to estimate your income as a percentage of the FPL. If you’re near the threshold, consider consulting a certified application counselor or navigator, who can provide personalized guidance. Additionally, keep track of deadlines and renewal requirements, as eligibility must often be re-verified annually. By approaching eligibility criteria methodically, you can ensure a smooth and accurate filing process for poverty line health insurance.

Understanding Insurance: Which Physicians Qualify as PCPs in Coverage Plans

You may want to see also

Explore related products

![]()

Application Process: Gather documents, complete forms, and submit via online portals or local offices

Filing for poverty line health insurance begins with meticulous document gathering, a step often overlooked but critical to a seamless application. Essential documents typically include proof of income, such as pay stubs or tax returns, identification like a driver’s license or state ID, and residency verification, often a utility bill or lease agreement. For households with dependents, birth certificates or Social Security cards may be required. Inaccurate or missing documents can delay approval, so double-check each item against the program’s checklist. Pro tip: Organize documents in a folder or digital drive for easy access during the application process.

Once documents are in hand, the next phase involves completing forms, a task that demands precision and patience. Most poverty line health insurance programs provide detailed instructions, but common pitfalls include skipping sections, misinterpreting questions, or using outdated forms. For instance, Medicaid applications often require information on household size, income sources, and medical expenses. If English isn’t your first language, seek assistance from bilingual staff or community organizations to ensure accuracy. Remember, errors can lead to denials or delays, so take your time and review each field before submission.

Submission methods vary by program and location, offering flexibility but also potential confusion. Online portals are increasingly popular for their convenience, allowing applicants to upload documents and track progress in real time. However, not all programs accept digital submissions, and technical glitches can occur. Alternatively, local offices provide in-person assistance, ideal for those who prefer face-to-face interaction or lack internet access. If choosing this route, call ahead to confirm office hours and required materials. Whichever method you select, retain a copy of your submission for your records.

A comparative analysis of submission methods reveals trade-offs. Online portals save time and reduce paperwork but may exclude those without internet access or digital literacy. Local offices offer personalized guidance but can involve long wait times and travel. Hybrid approaches, such as starting online and visiting an office for clarification, can balance these pros and cons. For example, some states allow applicants to initiate the process online and complete it in person, ensuring both efficiency and support. Assess your needs and resources to determine the best approach for your situation.

Finally, practical tips can streamline the application process. Create a timeline to avoid missing deadlines, especially if your state has open enrollment periods. Use a checklist to track completed steps and pending tasks. If you’re unsure about any part of the process, reach out to program representatives or community health workers for guidance. For families with children, consider applying for related programs like SNAP or WIC simultaneously, as many agencies handle multiple applications. By staying organized and proactive, you can navigate the application process with confidence and secure the health coverage you need.

SSI and Medical Insurance: What's the Connection?

You may want to see also

Explore related products

![Insurance versus poverty 1912 [Leather Bound]](https://m.media-amazon.com/images/I/81nNKsF6dYL._AC_UY218_.jpg)

![]()

Coverage Details: Learn benefits, exclusions, and preventive care services included in the insurance plan

Understanding the specifics of your health insurance plan is crucial, especially when navigating poverty line health insurance. Coverage details dictate what medical services are included, what’s excluded, and how preventive care is handled. Start by reviewing the Summary of Benefits and Coverage (SBC) provided by your insurer. This document breaks down essential services like hospitalization, prescription drugs, and maternity care, often categorized by metal tiers (Bronze, Silver, Gold, Platinum) that indicate cost-sharing levels. For instance, a Silver plan typically covers 70% of healthcare costs, while the remaining 30% is your responsibility through copays or deductibles.

Exclusions are equally important to identify, as they outline what your plan won’t cover. Common exclusions include cosmetic procedures, experimental treatments, and certain pre-existing conditions during a waiting period. For example, dental implants or fertility treatments might not be covered under basic plans. Knowing these limitations prevents unexpected out-of-pocket expenses. Additionally, some plans exclude specific prescription drugs or require prior authorization for high-cost medications. Always cross-reference your medical needs with the exclusions list to avoid surprises.

Preventive care services are a cornerstone of poverty line health insurance, often fully covered to promote long-term health and reduce costs. These services include vaccinations, cancer screenings, and annual check-ups. For instance, women aged 21–65 are entitled to a Pap smear every 3 years, while adults over 50 should receive regular colonoscopies. Children under 18 are covered for developmental screenings and immunizations, such as the MMR vaccine. Utilize these services proactively; they’re designed to catch health issues early, saving money and improving outcomes.

To maximize your plan’s benefits, familiarize yourself with in-network providers. Out-of-network services often incur higher costs or may not be covered at all. Use your insurer’s provider directory to locate participating doctors, hospitals, and specialists. If you require a specialist, obtain a referral from your primary care physician to ensure coverage. For prescriptions, check the plan’s formulary to confirm which medications are covered and at what tier. Generic drugs are typically cheaper and more likely to be covered than brand-name alternatives.

Finally, keep detailed records of all medical visits, prescriptions, and communications with your insurer. This documentation is invaluable if disputes arise over coverage or billing. Set reminders for annual renewals and open enrollment periods to review changes in your plan. Poverty line health insurance often evolves with policy updates, so staying informed ensures you’re leveraging all available benefits. By mastering coverage details, exclusions, and preventive care, you can navigate your plan confidently and make the most of its protections.

Combining Commercial Insurance and Medicaid: Is It Possible?

You may want to see also

Explore related products

![]()

Renewal Procedures: Track deadlines, update income information, and reapply annually to maintain coverage

Maintaining health insurance coverage under poverty line programs requires vigilance and proactive management. One critical aspect is understanding and adhering to renewal procedures, which often involve tracking deadlines, updating income information, and reapplying annually. Missing these steps can result in a lapse of coverage, leaving individuals vulnerable during critical health needs. For instance, Medicaid and Children’s Health Insurance Program (CHIP) beneficiaries must reapply every 12 months, with some states requiring updates as frequently as every six months. Marking these deadlines on a calendar or setting digital reminders can prevent accidental gaps in coverage.

Income verification is a cornerstone of renewal procedures for poverty line health insurance. Programs like Medicaid use income thresholds to determine eligibility, which can fluctuate based on federal poverty level (FPL) guidelines. For example, in 2023, the FPL for a family of four was $28,000 annually. If your income changes—due to a new job, reduced hours, or other factors—it’s essential to report these updates promptly. Failure to do so may result in ineligibility or overpayment penalties. Keep detailed records of income changes, including pay stubs, tax returns, and unemployment benefits, to streamline the renewal process.

Reapplying annually is not merely a formality but a necessary step to reassess eligibility and ensure continued coverage. The application process often involves submitting updated income documentation, household size changes, and other relevant information. Some states offer online portals for renewal, while others require paper submissions. For example, Healthcare.gov provides a user-friendly platform for updating information and reapplying for Marketplace plans. If you’re unsure about the process, contact your state’s health insurance marketplace or a local navigator for assistance. Proactive engagement with these steps can save time and reduce stress during the renewal period.

A comparative analysis of renewal procedures across different states reveals variations in timelines and requirements. For instance, California’s Medi-Cal program allows beneficiaries to renew coverage online, by mail, or in person, with reminders sent 60 days before the deadline. In contrast, Texas requires Medicaid recipients to complete a renewal packet and submit it 30 days before expiration. Understanding these state-specific nuances is crucial for accurate filing. Additionally, leveraging community resources, such as nonprofit organizations or legal aid services, can provide tailored guidance for navigating these processes effectively.

In conclusion, mastering renewal procedures for poverty line health insurance demands attention to detail, timely updates, and a proactive approach. By tracking deadlines, maintaining accurate income records, and reapplying annually, individuals can safeguard their coverage and avoid unnecessary disruptions. Practical tips, such as using digital tools for reminders and seeking state-specific guidance, can further simplify the process. Remember, staying informed and organized is key to maintaining access to essential healthcare services.

Medigap vs. Medicare: What's the Difference?

You may want to see also

Explore related products

![]()

Appeals & Assistance: Navigate denials, seek help from navigators, or file appeals for incorrect decisions

Denials of health insurance applications based on income eligibility can feel like a dead end, but they’re often just a detour. Understanding the appeals process is critical for those near the poverty line, as marginal income fluctuations or documentation errors frequently trigger rejections. For instance, a single parent earning $1,200 monthly might fall below the Federal Poverty Level (FPL) but be denied due to unreported child support income. Appeals allow applicants to correct such oversights, ensuring access to Medicaid or subsidized Marketplace plans.

Navigators and certified application counselors are underutilized lifelines in this process. These professionals, funded by state or federal programs, provide free, unbiased assistance to decipher denial letters, gather necessary documents, and file appeals. For example, a navigator might help a 55-year-old applicant whose denial cited "insufficient proof of unemployment" by guiding them to obtain a formal termination letter from their employer or a state unemployment benefits statement. Their expertise can transform a confusing bureaucratic maze into a manageable task.

Filing an appeal requires precision and persistence. Start by requesting a case review within 90 days of the denial notice—missing this deadline can force you to reapply from scratch. Include all supporting documents, such as pay stubs, tax returns, or proof of household size, even if they were submitted initially. For instance, a family of four earning $30,000 annually might need to provide updated W-2 forms to reflect a recent job loss. Be concise in your appeal letter: state the reason for denial, explain why it’s incorrect, and highlight the evidence provided.

Comparatively, while navigators offer hands-on support, legal aid organizations can step in for complex cases. For example, if a denial stems from a disputed citizenship status, an attorney specializing in immigration and healthcare law might be necessary. Some states also offer ombudsman services to mediate between applicants and insurance agencies. Knowing when to escalate from a navigator to legal assistance can save months of back-and-forth.

Ultimately, denials are not final verdicts but opportunities to correct the record. Whether leveraging a navigator’s expertise, meticulously filing an appeal, or seeking legal intervention, persistence pays off. For those hovering at the poverty line, every effort to secure health insurance is an investment in stability—one that can prevent medical debt and ensure access to essential care.

Trader Joe's Insurance: Medical Coverage Offerings Explained

You may want to see also

Frequently asked questions

The poverty line for health insurance eligibility varies by state and household size. It is typically based on the Federal Poverty Level (FPL), which is updated annually. For example, in 2023, the FPL for a single individual is $14,580, while for a family of four, it is $30,000. Check your state’s Medicaid or Marketplace guidelines to determine if you qualify.

To prove your income is below the poverty line, you’ll need to provide documentation such as recent pay stubs, tax returns, unemployment benefits statements, or Social Security benefit letters. If you’re self-employed, bank statements or profit/loss statements may be required. Submit these documents when applying for Medicaid or subsidized health insurance through the Marketplace.

Yes, even if your income is slightly above the poverty line, you may still qualify for subsidized health insurance through the Affordable Care Act (ACA) Marketplace. Subsidies are available for individuals and families earning up to 400% of the FPL. Additionally, some states have expanded Medicaid to cover individuals with incomes above the traditional poverty line, so check your state’s eligibility criteria.