Applying for health insurance can seem daunting, but it’s a crucial step in securing financial protection and access to healthcare services. The process typically begins with researching available plans, whether through your employer, government marketplaces like Healthcare.gov, or private insurers. Key factors to consider include coverage options, premiums, deductibles, and provider networks. Once you’ve identified a suitable plan, gather necessary documentation, such as proof of income and identification, and complete the application either online, by phone, or in person. Be mindful of enrollment periods, as missing deadlines may limit your options. After submitting your application, review the details carefully and await confirmation of your coverage. Understanding the steps and requirements ensures a smoother experience and helps you choose a plan that best fits your needs.

| Characteristics | Values |

|---|---|

| Eligibility Requirements | Varies by country/region; typically based on age, income, residency. |

| Application Methods | Online portals, in-person at government offices, via brokers/agents. |

| Required Documents | Proof of identity, income, residency, and citizenship/immigration status. |

| Enrollment Periods | Open enrollment (annual) and special enrollment (qualifying events). |

| Coverage Options | Private insurance, government-funded (e.g., Medicaid, Medicare), employer-sponsored. |

| Cost Factors | Premiums, deductibles, copayments, and out-of-pocket maximums. |

| Subsidies/Assistance | Available for low-income individuals (e.g., ACA subsidies in the U.S.). |

| Processing Time | Varies; typically 2-6 weeks depending on the provider and method. |

| Renewal Process | Automatic renewal or reapplication required annually/periodically. |

| Coverage Start Date | Usually the first day of the month following approval. |

| Network Restrictions | In-network vs. out-of-network providers (affects costs). |

| Pre-existing Conditions | Covered under most plans (e.g., ACA in the U.S. prohibits discrimination). |

| International Coverage | Limited; may require additional travel or international health plans. |

| Cancellation Policy | Can cancel during specific periods; may incur fees or penalties. |

| Customer Support | Available via phone, email, or online chat for application assistance. |

Explore related products

What You'll Learn

- Eligibility Requirements: Check age, income, residency, and citizenship criteria for health insurance plans

- Plan Comparison: Compare coverage, premiums, deductibles, and provider networks to choose the best plan

- Application Process: Gather documents, complete forms, and submit applications online or via mail

- Enrollment Periods: Understand open enrollment, special enrollment, and Medicaid/CHIP year-round options

- Cost Assistance: Explore subsidies, tax credits, and Medicaid to reduce insurance costs

![]()

Eligibility Requirements: Check age, income, residency, and citizenship criteria for health insurance plans

Understanding eligibility requirements is the first step in navigating the health insurance application process. Each plan has specific criteria that determine who can enroll, and these criteria often revolve around age, income, residency, and citizenship. For instance, Medicaid and the Children’s Health Insurance Program (CHIP) have income limits based on the federal poverty level, while Medicare is primarily for individuals aged 65 and older, regardless of income. Knowing where you fit within these categories ensures you apply for the right plan and avoid unnecessary complications.

Age is a straightforward but critical factor. Most health insurance plans categorize applicants into age groups, with different options available for children, adults, and seniors. For example, young adults under 26 may still qualify for coverage under a parent’s plan, while seniors aged 65 and older are eligible for Medicare. Some plans also offer special benefits for children, such as CHIP, which covers kids in families with incomes too high for Medicaid but still unable to afford private insurance. Always verify the age requirements for the plan you’re considering to ensure eligibility.

Income plays a significant role, particularly for government-funded programs like Medicaid and subsidized Marketplace plans. Eligibility for these programs is often tied to a percentage of the federal poverty level (FPL). For instance, in 2023, individuals earning up to 138% of the FPL in states that expanded Medicaid may qualify for coverage. For Marketplace plans, households earning between 100% and 400% of the FPL may be eligible for premium tax credits. Use the Healthcare.gov subsidy calculator to estimate your eligibility and potential savings before applying.

Residency and citizenship status are equally important. Most health insurance plans require applicants to be legal residents of the state where they’re applying. For federal programs like Medicaid and Medicare, U.S. citizenship or qualified immigration status is typically mandatory. However, some states offer health insurance options for undocumented immigrants, particularly for children or pregnant women. Always check the specific residency and citizenship requirements for your state and chosen plan to avoid ineligibility issues.

Practical tip: Gather all necessary documentation before starting your application. This includes proof of age (e.g., birth certificate or driver’s license), income verification (e.g., tax returns or pay stubs), residency proof (e.g., utility bills or lease agreements), and citizenship or immigration status documents. Having these on hand streamlines the process and reduces the risk of delays. Remember, eligibility criteria can vary widely, so take the time to research and understand the requirements for your specific situation.

Should You Share All Medical Insurance Details?

You may want to see also

Explore related products

![]()

Plan Comparison: Compare coverage, premiums, deductibles, and provider networks to choose the best plan

Choosing the right health insurance plan requires a meticulous comparison of key factors: coverage, premiums, deductibles, and provider networks. Each element plays a distinct role in determining the plan’s value and suitability for your needs. Start by listing your healthcare priorities—frequent doctor visits, prescription medications, or specialized care—to identify which plans align with your requirements. For instance, a plan with lower premiums might seem appealing, but if it excludes your preferred doctors or lacks coverage for essential treatments, the cost savings could be illusory. Conversely, a higher-premium plan with a robust provider network and comprehensive coverage may offer better long-term value.

Premiums are the recurring payments you make to maintain coverage, but they’re only part of the financial equation. Deductibles—the amount you pay out-of-pocket before insurance kicks in—can significantly impact your overall costs. For example, a plan with a $1,500 deductible and a $200 monthly premium might be more cost-effective than a $100 premium plan with a $5,000 deductible if you anticipate frequent medical needs. Use a simple calculation: multiply your expected annual medical expenses by the plan’s coinsurance rate, then add the deductible. This will help you estimate total out-of-pocket costs for each plan.

Provider networks are another critical factor, especially if you have established relationships with specific doctors or hospitals. HMOs typically require in-network care and referrals for specialists, while PPOs offer more flexibility but at higher costs. If you’re tied to a particular healthcare system, ensure the plan includes it in its network. For instance, a PPO with out-of-network coverage might be worth the extra premium if your preferred specialist isn’t in-network. Conversely, if you’re open to new providers, an HMO could save you money without compromising quality.

Coverage details often reveal hidden strengths or weaknesses in a plan. Pay attention to exclusions, limitations, and additional benefits like mental health services, maternity care, or telehealth options. For example, a plan covering 80% of specialty care costs after the deductible could be a lifeline for chronic conditions. Similarly, plans with no-cost preventive services align well with proactive health management. Always review the Summary of Benefits and Coverage (SBC) document for each plan to understand exactly what’s included and what’s not.

Finally, consider your risk tolerance and financial flexibility. If you’re generally healthy and rarely visit the doctor, a high-deductible plan paired with a Health Savings Account (HSA) might offer tax advantages and lower premiums. However, if you have dependents or a history of medical issues, a plan with higher premiums but lower out-of-pocket costs could provide greater peace of mind. Use online comparison tools or consult a broker to streamline the process, but remember: the best plan isn’t the cheapest—it’s the one that balances affordability with the coverage you need.

Securing Trade Insurance: Why Robust Security Measures Are Non-Negotiable

You may want to see also

Explore related products

$19.99 $67.66

![]()

Application Process: Gather documents, complete forms, and submit applications online or via mail

Applying for health insurance begins with a meticulous gathering of documents, a step often overlooked but critical to a seamless process. Essential items include proof of identity (like a driver’s license or passport), income verification (recent pay stubs or tax returns), and any existing health coverage details. For dependents, birth certificates or adoption papers are mandatory. Pro tip: Organize these in a digital folder or physical binder to avoid last-minute scrambling. Missing even one document can delay approval, so double-check the insurer’s checklist before proceeding.

Once your documents are in order, the next hurdle is completing the application forms, a task that demands precision and patience. Most insurers provide online portals with guided questions, but errors like misspelled names or incorrect dates can lead to rejections. If applying via mail, ensure all fields are legible and complete. For families, list all members accurately, including their relationship to the primary applicant. A common mistake is omitting part-time income or failing to disclose pre-existing conditions—transparency here prevents future claim disputes.

The submission phase offers flexibility: online or mail. Online applications are faster, with instant confirmation and real-time error checks. However, older adults or those without internet access may prefer mailing physical forms. If choosing this route, use certified mail to track delivery and retain proof of submission. Regardless of method, keep a copy of your completed application and supporting documents. Processing times vary—typically 2–4 weeks—so plan ahead, especially if coverage is time-sensitive.

Comparing the two submission methods reveals trade-offs. Online applications save time but require digital literacy and reliable internet. Mailed applications offer a tangible record but risk delays due to postal errors. For instance, a 2022 study found that 15% of mailed applications were delayed by 10 days or more. If deadlines are tight, prioritize online submission and follow up with a phone call to confirm receipt. Both methods require equal attention to detail, but the choice hinges on your comfort and urgency.

Finally, a persuasive argument for thoroughness: treating the application process as a priority ensures you secure the best possible coverage. Incomplete or inaccurate submissions not only delay approval but may result in higher premiums or denied claims later. For example, failing to disclose a chronic condition could void future treatments. Conversely, a well-prepared application positions you for potential discounts or waivers. Think of it as an investment—time spent now pays dividends in long-term health security.

Medical Director Insurance Jobs: Stable Career Choice?

You may want to see also

Explore related products

![]()

Enrollment Periods: Understand open enrollment, special enrollment, and Medicaid/CHIP year-round options

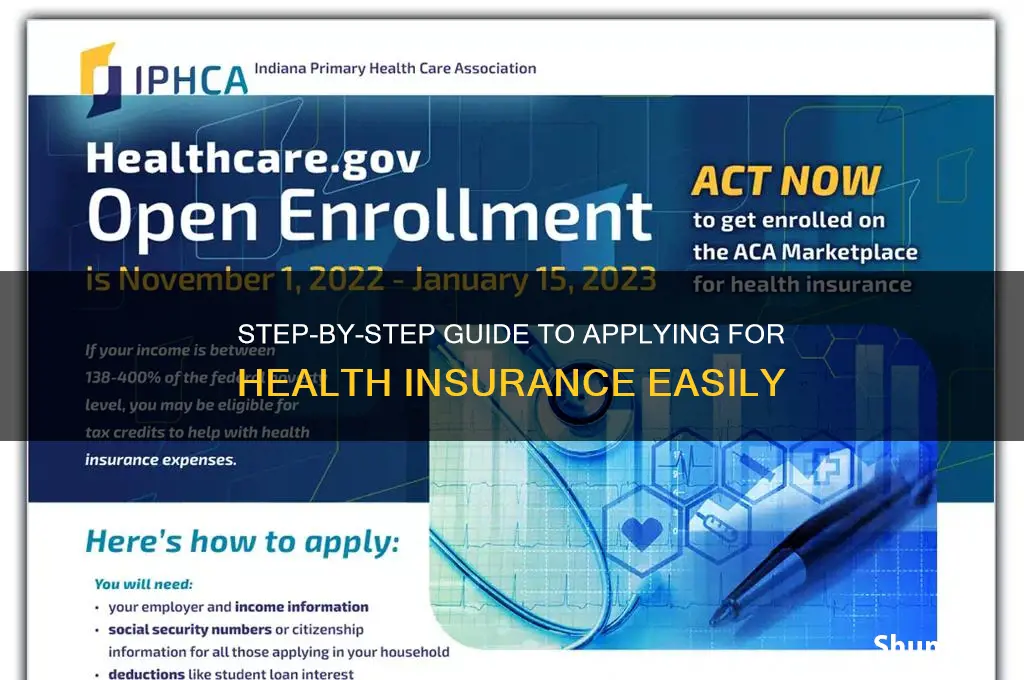

Timing is everything when applying for health insurance, and understanding enrollment periods is crucial to securing coverage. The annual Open Enrollment Period (OEP) is your primary window to sign up for a health plan or switch to a new one. Typically running from November 1 to December 15 (though dates may vary by state), this is the time when most individuals and families can enroll in a plan without needing a qualifying event. Missing this window means you’ll likely have to wait until the next year unless you qualify for a Special Enrollment Period (SEP).

Life doesn’t always align with annual schedules, which is where Special Enrollment Periods come in. These are triggered by specific life events, such as losing job-based coverage, getting married, having a baby, or moving to a new area. For example, if you lose your job and employer-sponsored insurance, you have 60 days to enroll in a new plan through the marketplace. Each qualifying event has its own timeline, so act promptly—you typically have 60 days before or after the event to apply. Documentation is key here; be prepared to provide proof of the life event to qualify.

For low-income individuals and families, Medicaid and the Children’s Health Insurance Program (CHIP) offer year-round enrollment, bypassing the need to wait for an OEP or SEP. Eligibility is based on income and household size, with thresholds varying by state. For instance, in 2023, a family of four earning up to 138% of the federal poverty level ($38,295 annually) may qualify for Medicaid in states that expanded the program. CHIP covers children in families earning too much for Medicaid but still below a certain income cap, often around 200-300% of the poverty level. Applications can be submitted at any time, and coverage often begins immediately upon approval.

Comparing these options highlights the importance of knowing your circumstances. If you’re healthy and miss the OEP, an SEP could be your lifeline, but it requires a qualifying event. Medicaid and CHIP, on the other hand, provide a safety net for those who meet income criteria, with no enrollment deadlines. For example, a single parent earning $25,000 annually with two children would likely qualify for CHIP, ensuring her kids are covered year-round. Understanding these distinctions ensures you don’t miss out on critical coverage opportunities.

To navigate enrollment periods effectively, mark your calendar for the OEP, keep an eye on life changes that trigger an SEP, and explore Medicaid/CHIP if your income qualifies. Pro tip: If you’re nearing the end of an SEP window, start gathering documents early to avoid delays. For Medicaid/CHIP, use the Healthcare.gov tool to estimate eligibility and apply directly through your state’s agency. By mastering these enrollment periods, you’ll ensure continuous coverage tailored to your needs.

Herpes Medication: Out-of-Pocket Costs and Treatment Options

You may want to see also

Explore related products

$9.97 $19.99

$9.09 $12.99

![]()

Cost Assistance: Explore subsidies, tax credits, and Medicaid to reduce insurance costs

Health insurance costs can be a significant financial burden, but you don’t have to shoulder the full expense alone. Subsidies, tax credits, and Medicaid are powerful tools designed to reduce your out-of-pocket costs, making coverage more affordable. Understanding these options is the first step toward securing the financial support you need.

Subsidies and Tax Credits: A Path to Lower Premiums

The Affordable Care Act (ACA) offers premium tax credits to individuals and families with incomes between 100% and 400% of the federal poverty level (FPL). For example, in 2023, a single person earning up to $54,360 or a family of four earning up to $111,000 may qualify. These credits are applied directly to your monthly premiums, significantly reducing what you pay. To determine eligibility, use the Health Insurance Marketplace’s application, which calculates your subsidy based on income and household size. Pro tip: Even if you think you earn too much, recent expansions have increased eligibility, so it’s worth checking.

Medicaid: Comprehensive Coverage for Low-Income Individuals

Medicaid provides free or low-cost health insurance to those with incomes below 138% of the FPL in states that expanded the program. Eligibility criteria vary by state, but generally, adults, children, pregnant women, and people with disabilities may qualify. For instance, a single adult earning up to $18,754 annually could be eligible in expansion states. Applying is straightforward—you can do so through your state’s Medicaid website or the Health Insurance Marketplace, which will redirect your application if Medicaid is a better fit. Caution: Some states have not expanded Medicaid, so eligibility thresholds may be lower.

Cost-Sharing Reductions: Lowering Out-of-Pocket Expenses

If your income falls between 100% and 250% of the FPL, you may also qualify for cost-sharing reductions (CSRs). These subsidies reduce deductibles, copays, and coinsurance, making it easier to afford care when you need it. For example, a silver-level plan with CSRs might have a deductible of $200 instead of $4,000. To access CSRs, you must enroll in a silver plan through the Marketplace. This option is particularly beneficial for those who anticipate frequent medical visits or prescriptions.

Practical Steps to Maximize Assistance

- Gather Documentation: Have proof of income, citizenship, and household size ready when applying.

- Use the Marketplace: Start your application at Healthcare.gov to explore all available options.

- Check State Programs: Some states offer additional assistance beyond federal programs.

- Reassess Annually: Income and eligibility can change, so update your application during open enrollment.

By leveraging subsidies, tax credits, and Medicaid, you can significantly reduce health insurance costs. These programs are designed to ensure that financial barriers don’t stand between you and essential care. Take the time to explore your options—affordable coverage is within reach.

Does Health Insurance Cover Oral Surgery? What You Need to Know

You may want to see also

Frequently asked questions

Begin by researching available plans through your state’s health insurance marketplace, Healthcare.gov, or private insurers. Compare coverage options, costs, and provider networks to find the best fit for your needs.

You’ll typically need proof of identity (e.g., driver’s license or passport), income verification (e.g., tax returns or pay stubs), and information about your household members.

Yes, if you qualify for a special enrollment period due to life events like marriage, birth of a child, or loss of other coverage. Otherwise, you must wait for the annual open enrollment period.

Use the marketplace application to check your eligibility for premium tax credits or Medicaid based on your income and household size.

Applying through the marketplace allows you to compare plans and access subsidies, while applying directly through a private insurer limits you to their plans but may offer faster processing.