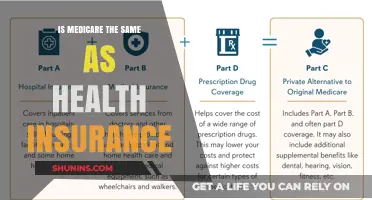

Medicare health insurance is a federal program in the United States designed to provide healthcare coverage primarily for individuals aged 65 and older, as well as certain younger people with disabilities and those with End-Stage Renal Disease (ESRD). Established in 1965, Medicare is divided into several parts, each covering different aspects of healthcare: Part A covers hospital stays, Part B covers medical services like doctor visits, Part C (Medicare Advantage) offers private insurance plans that combine Parts A and B, and Part D provides prescription drug coverage. Medicare helps millions of Americans access essential medical services, though it typically requires beneficiaries to pay premiums, deductibles, and copayments, and it does not cover all healthcare costs, often prompting individuals to supplement it with additional insurance plans.

| Characteristics | Values |

|---|---|

| Definition | A federal health insurance program in the U.S. for people aged 65+, certain younger individuals with disabilities, and those with End-Stage Renal Disease (ESRD) or Amyotrophic Lateral Sclerosis (ALS). |

| Administered By | Centers for Medicare & Medicaid Services (CMS), a division of the U.S. Department of Health and Human Services. |

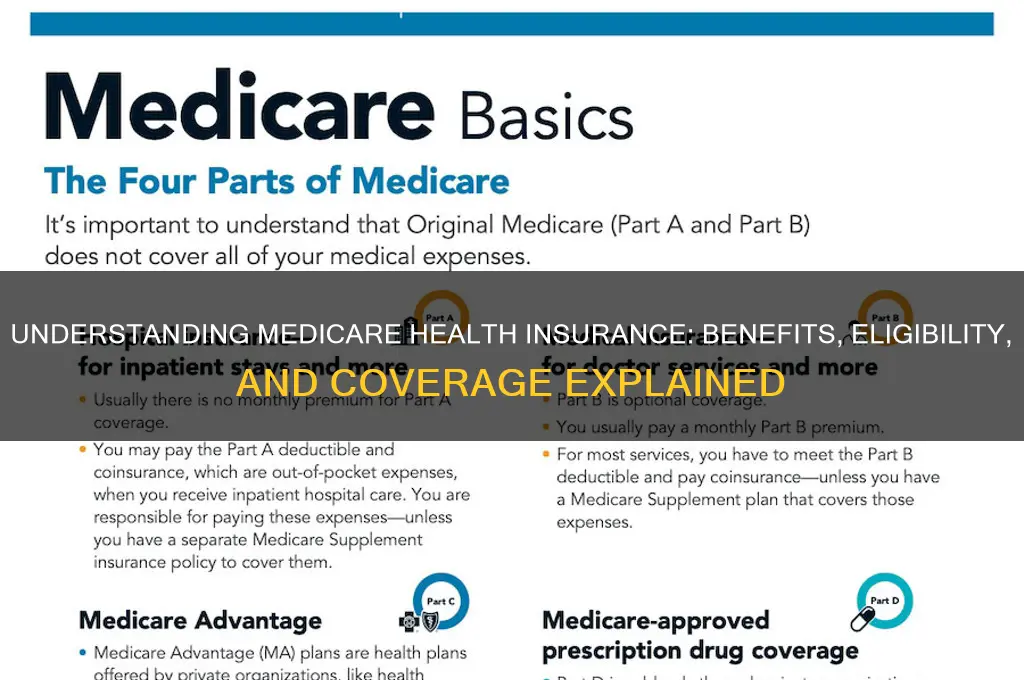

| Parts of Medicare | Part A (Hospital Insurance), Part B (Medical Insurance), Part C (Medicare Advantage), Part D (Prescription Drug Coverage). |

| Eligibility | - Age 65+ (automatically eligible if receiving Social Security benefits). - Under 65 with certain disabilities (after 24 months of disability benefits). - Any age with ESRD or ALS. |

| Enrollment Periods | Initial Enrollment Period (7 months around 65th birthday), General Enrollment Period (Jan 1 - Mar 31), Special Enrollment Periods (specific circumstances). |

| Premiums | - Part A: Usually premium-free if you or your spouse paid Medicare taxes. - Part B: Standard premium is $174.70/month (2024), may be higher based on income. - Part C & D: Varies by plan. |

| Deductibles | - Part A: $1,632 per benefit period (2024). - Part B: $240 annual deductible (2024). - Part C & D: Varies by plan. |

| Coverage | - Part A: Hospital stays, skilled nursing facility care, hospice, home health care. - Part B: Doctor visits, outpatient care, preventive services, medical supplies. - Part C: Combines Part A, B, and often Part D, with additional benefits. - Part D: Prescription drugs. |

| Out-of-Pocket Costs | Coinsurance, copayments, and deductibles apply; no annual out-of-pocket maximum in Original Medicare (Parts A & B). |

| Medigap (Supplemental Insurance) | Private insurance to cover gaps in Original Medicare, such as copayments and deductibles. |

| Provider Network | Original Medicare: Nationwide network of providers. Medicare Advantage: Typically has a network of providers. |

| Prescription Drug Coverage | Part D plans cover prescription drugs; some Medicare Advantage plans include Part D. |

| Preventive Services | Covers preventive care like screenings, vaccinations, and annual wellness visits at no cost if provider accepts Medicare assignment. |

| Funding | Funded through payroll taxes, premiums, deductibles, coinsurance, and federal budget allocations. |

| Enrollment | Over 65 million people enrolled in Medicare as of 2023. |

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/61ilSrOeMoL._AC_UY218_.jpg)

What You'll Learn

- Eligibility Requirements: Age, disability, and citizenship criteria for Medicare coverage

- Medicare Parts: Explanation of Part A, B, C, and D benefits

- Enrollment Periods: Initial, general, and special enrollment timelines

- Costs & Premiums: Deductibles, copays, and monthly premium details

- Coverage Limits: Services covered and exclusions under Medicare plans

![]()

Eligibility Requirements: Age, disability, and citizenship criteria for Medicare coverage

Medicare, a federal health insurance program in the United States, is not universally accessible to all citizens. Eligibility is strictly defined by specific criteria, primarily centered around age, disability status, and citizenship. Understanding these requirements is crucial for anyone seeking to enroll in Medicare, as it determines not only who can access the program but also which parts of Medicare they qualify for.

Medicare eligibility begins at age 65 for most Americans. This is the most common pathway to enrollment, often referred to as "Original Medicare." Individuals who have paid Medicare taxes for at least 10 years (40 quarters) while working are eligible for premium-free Part A, which covers hospital stays, skilled nursing facility care, and some home health care. Part B, which covers doctor visits, outpatient care, and preventive services, requires a monthly premium. Enrollment typically occurs during a seven-month Initial Enrollment Period surrounding the individual's 65th birthday.

While age 65 is the standard threshold, younger individuals with certain disabilities can also qualify for Medicare. People under 65 who have received Social Security Disability Insurance (SSDI) benefits for 24 months are automatically enrolled in Medicare. This includes individuals with permanent disabilities, such as end-stage renal disease (ESRD) or amyotrophic lateral sclerosis (ALS), who may qualify for Medicare immediately upon diagnosis or SSDI eligibility. It’s important to note that the 24-month waiting period for SSDI recipients does not apply to those with ALS, who are enrolled in Medicare as soon as their SSDI benefits begin.

Citizenship and residency status are non-negotiable requirements for Medicare eligibility. U.S. citizens and permanent legal residents who have lived in the country for at least five continuous years are eligible to enroll. Non-citizens, including undocumented immigrants and those on temporary visas, are generally not eligible for Medicare, though some exceptions exist for refugees and asylees who meet specific criteria. Proof of citizenship or residency, such as a birth certificate, passport, or green card, is required during the enrollment process.

Navigating Medicare eligibility can be complex, especially for those under 65 with disabilities or non-citizen status. Prospective enrollees should verify their eligibility through the Social Security Administration (SSA) or the Railroad Retirement Board (RRB) for railroad workers. Early planning is essential, particularly for understanding enrollment periods and avoiding late penalties. For example, missing the Initial Enrollment Period can result in a 10% premium surcharge for Part B for each 12-month period enrollment was delayed. Additionally, individuals nearing eligibility should review their work history to ensure they meet the 40-quarter requirement for premium-free Part A.

In summary, Medicare eligibility hinges on a combination of age, disability status, and citizenship. While age 65 is the primary gateway, younger individuals with disabilities and certain non-citizens can also qualify under specific conditions. Understanding these criteria and taking proactive steps to verify eligibility can ensure timely access to Medicare benefits and avoid costly penalties. Whether you’re approaching 65, living with a disability, or navigating citizenship requirements, careful planning and consultation with the SSA or RRB are key to a smooth enrollment process.

AARP Membership Perks: Insurance Companies Offering Exclusive Discounts

You may want to see also

Explore related products

$14.99

![]()

Medicare Parts: Explanation of Part A, B, C, and D benefits

Medicare, the federal health insurance program, is divided into distinct parts, each designed to cover specific healthcare needs. Understanding these parts—A, B, C, and D—is crucial for maximizing benefits and minimizing out-of-pocket costs. Let’s break down what each part covers and how they work together.

Part A: Hospital Insurance

Part A primarily covers inpatient hospital stays, skilled nursing facility care, hospice care, and some home health services. Most beneficiaries don’t pay a monthly premium for Part A if they or their spouse paid Medicare taxes while working. However, there’s a deductible ($1,632 in 2023) for each hospital benefit period, and coinsurance applies after 60 days of hospitalization. For example, if you’re admitted to the hospital for pneumonia, Part A covers the room, meals, and nursing care, but you’ll pay the deductible and potential coinsurance. Pro tip: Review your length of stay carefully, as observation services (not inpatient care) aren’t covered under Part A.

Part B: Medical Insurance

Part B covers outpatient services, including doctor visits, preventive care, lab tests, and durable medical equipment. Unlike Part A, Part B requires a monthly premium, which is $164.90 in 2023 for most beneficiaries. There’s also an annual deductible ($226 in 2023) and a 20% coinsurance for most services. For instance, if you need a colonoscopy, Part B covers the procedure, but you’ll pay 20% of the Medicare-approved amount after meeting the deductible. Persuasive note: Enroll in Part B when you’re first eligible to avoid late penalties, which can increase your premium by 10% for each 12-month period you delay.

Part C: Medicare Advantage Plans

Part C, also known as Medicare Advantage, is an alternative to Original Medicare (Parts A and B) offered by private insurers. These plans often include additional benefits like vision, dental, and prescription drug coverage. They typically have lower out-of-pocket costs but restrict you to a network of providers. For example, a Medicare Advantage HMO might require you to choose a primary care physician and get referrals for specialists. Comparative insight: While Part C can offer more comprehensive coverage, it’s less flexible than Original Medicare, so weigh your healthcare needs and provider preferences before enrolling.

Part D: Prescription Drug Coverage

Part D provides prescription drug coverage through private insurance plans approved by Medicare. Each plan has a formulary (list of covered drugs) and tiers that determine costs. For instance, generic drugs are usually in the lowest tier with the lowest copay, while specialty drugs may require higher out-of-pocket costs. In 2023, the average monthly premium for Part D is $31.50, but costs vary by plan and income. Practical tip: Use Medicare’s Plan Finder tool to compare plans based on your specific medications, as coverage and costs differ significantly between insurers.

By understanding the unique benefits of Medicare Parts A, B, C, and D, you can tailor your coverage to fit your healthcare needs and budget. Whether you stick with Original Medicare or opt for a Medicare Advantage plan, knowing what each part covers ensures you’re prepared for both routine care and unexpected medical expenses.

Billing D0364 to Medical Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Enrollment Periods: Initial, general, and special enrollment timelines

Medicare enrollment isn't a one-size-fits-all process. Understanding the different enrollment periods is crucial to avoiding penalties and ensuring you have the coverage you need when you need it. Let's break down the three main enrollment windows: Initial, General, and Special.

Initial Enrollment Period (IEP): Your Seven-Month Window

Your Initial Enrollment Period is a seven-month window surrounding your 65th birthday. It begins three months before the month you turn 65, includes your birthday month, and extends for three months afterward. This is the ideal time to enroll in Medicare, as you can sign up without facing late enrollment penalties. If you're already receiving Social Security benefits, you'll likely be automatically enrolled in Medicare Part A (hospital insurance) and Part B (medical insurance) during this period. If not, you'll need to actively enroll through the Social Security Administration.

General Enrollment Period (GEP): A Second Chance with a Catch

Missed your IEP? Don't panic. The General Enrollment Period runs from January 1st to March 31st each year. While this period allows you to sign up for Medicare Part A and/or Part B, there's a catch: you'll likely face a late enrollment penalty. This penalty is added to your monthly Part B premium and increases the longer you delay enrollment.

Special Enrollment Periods (SEPs): Life Changes Open Doors

Life doesn't always follow a predictable schedule. Special Enrollment Periods offer flexibility for individuals experiencing qualifying life events. These events include:

- Losing employer-sponsored health coverage: If you or your spouse lose coverage through an employer, you have an eight-month SEP to enroll in Medicare.

- Moving: Relocating to a new area may trigger an SEP if your current plan isn't available in your new location.

- Other qualifying events: These can include changes in Medicaid eligibility, release from incarceration, and more.

Key Takeaways: Timing is Everything

Understanding Medicare enrollment periods is essential for securing timely coverage and avoiding unnecessary costs. Mark your calendar for your IEP, be aware of the GEP and its penalties, and remember that life changes can open doors to SEPs. By staying informed and taking action during the appropriate enrollment window, you can navigate the Medicare landscape with confidence.

Keep Your Record Clean: Strategies to Reduce Accident Points

You may want to see also

Explore related products

![]()

Costs & Premiums: Deductibles, copays, and monthly premium details

Medicare, a federal health insurance program primarily for individuals aged 65 and older, operates through a structured cost-sharing model. Understanding its financial components—deductibles, copays, and monthly premiums—is crucial for maximizing its benefits. Each part of Medicare (A, B, C, and D) has distinct cost structures, making it essential to tailor your plan to your healthcare needs and budget.

Monthly Premiums: The Foundation of Your Coverage

Most beneficiaries pay a monthly premium for Medicare Part B, which covers outpatient services like doctor visits and preventive care. In 2023, the standard Part B premium is $164.90, though higher-income individuals may pay more due to income-related adjustments. Part A, covering hospital stays, is typically premium-free if you or your spouse paid Medicare taxes for at least 10 years. For those who need prescription drug coverage, Part D premiums vary by plan, averaging around $30 to $70 monthly. Pro tip: Use the Medicare Plan Finder tool to compare Part D plans and find one that aligns with your medication needs and budget.

Deductibles: Your Out-of-Pocket Threshold

Before Medicare coverage kicks in, you’ll often need to meet a deductible. For Part A, the deductible in 2023 is $1,600 per benefit period, which applies to hospital stays. Part B has a $226 annual deductible, after which Medicare covers 80% of approved services, leaving you responsible for the remaining 20%. Part D deductibles vary by plan but typically range from $0 to $505. Caution: Part A deductibles reset for each new benefit period, which begins when you’ve been out of the hospital for 60 consecutive days.

Copays and Coinsurance: Sharing the Cost

Copays and coinsurance are your share of costs after meeting deductibles. For Part B, you’ll pay 20% coinsurance for most services, though some preventive services are fully covered. Part D copays depend on your plan and the tier of your medication, often ranging from $1 to $100 per prescription. Medicare Advantage (Part C) plans bundle Parts A, B, and often D, with copays and coinsurance varying by plan. Example: A doctor’s visit might cost $25, while a specialist visit could be $50. Always review your plan’s Summary of Benefits to understand these costs.

Practical Tips for Managing Costs

To minimize out-of-pocket expenses, consider pairing Original Medicare (Parts A and B) with a Medigap policy, which covers deductibles, copays, and coinsurance. Alternatively, Medicare Advantage plans often have lower out-of-pocket maximums, capping your annual expenses. For Part D, use generic medications when possible and explore programs like Extra Help for low-income beneficiaries. Regularly review your coverage during the Annual Enrollment Period (October 15–December 7) to ensure your plan still meets your needs.

Takeaway: Knowledge is Your Best Tool

Medicare’s costs and premiums are not one-size-fits-all. By understanding deductibles, copays, and premiums, you can make informed decisions to optimize your coverage. Whether you’re enrolling for the first time or reassessing your plan, take advantage of resources like the Medicare website and local State Health Insurance Assistance Programs (SHIPs) to navigate this complex system effectively.

Checking Medical Insurance Status: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Coverage Limits: Services covered and exclusions under Medicare plans

Medicare, the federal health insurance program for individuals aged 65 and older, as well as certain younger people with disabilities, is a lifeline for millions. However, understanding its coverage limits is crucial to avoid unexpected out-of-pocket expenses. Medicare is divided into parts—A, B, C, and D—each covering specific services, but with distinct exclusions. For instance, while Part A covers hospital stays, it excludes long-term care, leaving beneficiaries to explore supplemental options like Medicaid or private insurance for extended nursing home needs.

Consider Part B, which covers outpatient services such as doctor visits, lab tests, and preventive care. While it pays for flu shots and diabetes screenings, it excludes routine dental, vision, and hearing care. For example, a beneficiary needing hearing aids would have to pay out of pocket, as Medicare does not cover these devices. This gap often leads individuals to purchase Medicare Advantage (Part C) plans, which may include additional benefits like dental and vision, though these plans can limit provider networks and require higher premiums.

Prescription drug coverage under Part D is another area with notable limits. Each Part D plan has a formulary, a list of covered medications, often tiered to determine cost-sharing. For instance, a Tier 1 generic drug might cost $10, while a Tier 4 specialty drug could require a 33% coinsurance, potentially costing hundreds of dollars monthly. Beneficiaries must review their plan’s formulary annually during the Open Enrollment Period (October 15–December 7) to ensure their medications remain covered, as plans can change their formularies yearly.

Exclusions across Medicare plans also extend to services deemed "not medically necessary." For example, cosmetic surgery, acupuncture, and most custodial care are not covered. However, exceptions exist for certain conditions. For instance, acupuncture is covered for chronic low back pain under a CMS-approved study, highlighting the importance of staying informed about evolving coverage policies. Beneficiaries should consult their plan’s Evidence of Coverage document or contact Medicare directly to clarify coverage for specific services.

Practical tips for navigating coverage limits include enrolling in a Medigap policy to fill gaps in Original Medicare (Parts A and B), such as copayments and deductibles. For those on Part D, using preferred pharmacies within the plan’s network can reduce drug costs. Additionally, beneficiaries should take advantage of Medicare’s Annual Wellness Visit, a no-cost preventive service that includes a personalized prevention plan and can identify potential health issues early. Understanding these limits and exclusions empowers beneficiaries to make informed decisions and maximize their Medicare benefits.

Does Health Insurance Cover Cataract Surgery? What You Need to Know

You may want to see also

Frequently asked questions

Medicare is a federal health insurance program in the United States primarily for people aged 65 and older, as well as younger individuals with certain disabilities or specific medical conditions like End-Stage Renal Disease (ESRD) or Amyotrophic Lateral Sclerosis (ALS).

Medicare is divided into parts: Part A covers hospital stays, Part B covers medical services like doctor visits, Part C (Medicare Advantage) offers additional benefits through private plans, and Part D covers prescription drugs. Coverage varies by part and plan.

Eligibility for Medicare includes U.S. citizens or permanent residents aged 65 and older, individuals under 65 with certain disabilities, and those with ESRD or ALS, regardless of age. Enrollment typically begins three months before turning 65.

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/61wrmwXah3L._AC_UL320_.jpg)