Medicare and health insurance are often discussed interchangeably, but they are not the same. Medicare is a federal health insurance program primarily for individuals aged 65 and older, as well as certain younger people with disabilities or specific medical conditions. It is divided into parts—A, B, C, and D—each covering different services, such as hospital stays, medical visits, and prescription drugs. In contrast, health insurance is a broader term referring to any policy that helps cover medical expenses, which can be provided by private companies, employers, or government programs like Medicare. While Medicare is a type of health insurance, not all health insurance plans are Medicare, and understanding the distinctions is crucial for making informed decisions about healthcare coverage.

| Characteristics | Values |

|---|---|

| Type | Medicare is a federal health insurance program, while private health insurance is offered by private companies. |

| Eligibility | Medicare is primarily for individuals aged 65+, certain younger people with disabilities, and those with End-Stage Renal Disease (ESRD). Private insurance is available to anyone, often through employers or individual purchase. |

| Coverage | Medicare consists of Parts A (hospital), B (medical), C (Medicare Advantage), and D (prescription drugs). Private insurance plans vary widely in coverage. |

| Cost | Medicare has premiums, deductibles, and copays, but costs are standardized. Private insurance costs vary by plan, provider, and location. |

| Provider Network | Medicare has a broad network of providers, but some may not accept it. Private insurance often has specific provider networks. |

| Supplemental Coverage | Medicare allows supplemental plans (Medigap) to cover gaps. Private insurance may offer add-ons but typically covers more comprehensively. |

| Funding | Medicare is funded by the federal government through taxes and premiums. Private insurance is funded by premiums, employer contributions, and profits. |

| Portability | Medicare is portable across states. Private insurance may have limitations based on location or employer. |

| Enrollment Periods | Medicare has specific enrollment periods (e.g., Initial Enrollment Period). Private insurance enrollment is often tied to open enrollment or qualifying events. |

| Prescription Drug Coverage | Medicare Part D covers prescription drugs. Private insurance often includes drug coverage as part of the plan. |

| Preventive Services | Medicare covers many preventive services at no cost. Private insurance typically covers preventive care but may require copays. |

| Long-Term Care | Medicare does not cover long-term care. Private insurance may offer long-term care coverage as an add-on. |

| Flexibility | Medicare has less flexibility in plan choice compared to private insurance, which offers a wide range of plans. |

| Administration | Medicare is administered by the Centers for Medicare & Medicaid Services (CMS). Private insurance is managed by individual companies. |

Explore related products

What You'll Learn

![]()

Medicare vs. Private Insurance: Coverage Differences

Medicare and private insurance serve as two distinct pathways to healthcare coverage, each with its own set of benefits, limitations, and eligibility criteria. While both aim to provide financial protection against medical expenses, their coverage differences can significantly impact the care you receive. Understanding these disparities is crucial for making informed decisions about your health insurance needs.

Coverage Scope: Comprehensive vs. Customizable

Medicare, a federal program, offers standardized coverage through its parts: Part A (hospital insurance), Part B (medical insurance), and optional Part D (prescription drug coverage). It also includes Medicare Advantage (Part C) plans, which bundle Parts A, B, and often D. Private insurance, on the other hand, provides customizable plans tailored to individual or employer preferences. For instance, private plans may include vision, dental, or mental health coverage as standard benefits, whereas Medicare typically requires supplemental plans (like Medigap) to fill these gaps. A 65-year-old retiree might find Medicare sufficient for basic needs but may need a Medigap policy to cover the 20% coinsurance Medicare Part B doesn’t pay.

Cost Structure: Predictability vs. Flexibility

Medicare’s costs are relatively predictable, with fixed premiums, deductibles, and copayments. For example, in 2023, the Part B premium is $164.90 monthly, and the Part A deductible is $1,600 per benefit period. Private insurance costs vary widely based on plan type, provider network, and employer contributions. A 40-year-old professional might pay $300 monthly for a family plan with a $3,000 deductible but enjoy lower out-of-pocket costs for in-network services. While Medicare offers stability, private insurance allows for cost-sharing flexibility, such as choosing higher deductibles for lower premiums.

Provider Networks: Accessibility vs. Choice

Medicare’s provider network is extensive, with most healthcare providers accepting it. However, Medicare Advantage plans often restrict beneficiaries to specific networks, limiting choice. Private insurance plans, particularly HMOs, also use networks but may offer more options for out-of-network care at higher costs. For a 55-year-old with a preferred specialist, private insurance might be preferable if that provider is out-of-network for Medicare Advantage plans.

Practical Tips for Decision-Making

To navigate these differences, assess your healthcare needs and budget. If you require frequent specialist visits, compare Medicare Advantage networks with private plan options. For prescription drug coverage, evaluate Part D plans against private insurance formularies. Use tools like Medicare’s Plan Finder or consult a broker to compare costs and benefits. For example, a 70-year-old with chronic conditions might benefit from Medicare’s comprehensive drug coverage, while a 35-year-old with minimal health needs could opt for a high-deductible private plan with a health savings account (HSA).

In summary, Medicare and private insurance differ in coverage scope, cost structure, and provider access. Medicare offers standardized, predictable coverage, while private insurance provides customization and flexibility. By evaluating your specific needs and using available resources, you can choose the plan that best aligns with your health and financial goals.

Starbucks Insurance: Steps to Apply for Coverage

You may want to see also

Explore related products

![]()

Eligibility Criteria for Medicare and Health Insurance

Medicare and private health insurance serve as distinct pathways to healthcare coverage, each with its own eligibility criteria. Medicare, a federal program, primarily caters to individuals aged 65 and older, offering a safety net for seniors. However, it also extends its reach to younger individuals with specific disabilities or those diagnosed with End-Stage Renal Disease (ESRD) or Amyotrophic Lateral Sclerosis (ALS), regardless of age. This inclusive approach ensures that vulnerable populations receive essential healthcare services.

In contrast, private health insurance operates on a different eligibility model, often tied to employment or individual purchase. Employers frequently offer group health insurance plans as part of employee benefits, with eligibility based on full-time employment status. For those without employer-sponsored options, individual health insurance plans are available through state marketplaces or private insurers. These plans typically require applicants to be U.S. citizens or legally present in the country, with premiums and coverage varying based on age, location, and health status.

A critical distinction lies in the enrollment periods. Medicare has specific enrollment windows, such as the Initial Enrollment Period (IEP) around one’s 65th birthday, while private insurance follows Open Enrollment Periods (OEPs) typically from November 1 to December 15 annually. Missing these windows can result in penalties or delayed coverage, underscoring the importance of timely action. For instance, late enrollment in Medicare Part B may incur a 10% premium surcharge for each 12-month period of delay.

Income and assets play a role in eligibility, particularly for Medicare Savings Programs (MSPs) and Medicaid, which assist low-income individuals with Medicare premiums. For example, in 2023, the income limit for Qualified Medicare Beneficiary (QMB) programs is $1,235 per month for individuals and $1,663 for couples. Private insurance, however, does not impose income limits but may offer subsidies through the Affordable Care Act (ACA) for those earning up to 400% of the federal poverty level.

Understanding these eligibility criteria is crucial for navigating the complexities of healthcare coverage. While Medicare provides a structured framework for seniors and disabled individuals, private insurance offers flexibility and broader options for the general population. By aligning personal circumstances with the right program, individuals can secure the coverage they need without unnecessary financial strain. Practical tips include reviewing eligibility annually, especially during life transitions like retirement or job changes, and leveraging resources like Healthcare.gov or State Health Insurance Assistance Programs (SHIPs) for guidance.

Choosing the Right Title Insurance Company: Key Factors to Consider

You may want to see also

Explore related products

![]()

Cost Comparison: Premiums, Deductibles, and Out-of-Pocket Expenses

Medicare and private health insurance both involve costs, but their structures differ significantly, impacting how much you pay out of pocket. Let's break down the key components: premiums, deductibles, and out-of-pocket expenses.

Premiums: Think of premiums as your monthly membership fee. Medicare Part B, for example, has a standard premium of $170.10 in 2023 for individuals earning below $97,000 annually. Private insurance premiums vary widely based on factors like age, location, plan type, and coverage level. A healthy 30-year-old might pay around $200-$400 monthly for a mid-tier plan, while someone older or with pre-existing conditions could face significantly higher costs.

Pro Tip: Compare premiums across different Medicare plans (like Part D for prescription drugs) and private insurers to find the best value for your needs.

Deductibles: This is the amount you pay out of pocket before your insurance coverage kicks in. Medicare Part A (hospital insurance) has a deductible of $1,600 per benefit period in 2023. Part B has an annual deductible of $226. Private insurance deductibles can range from $1,000 to $5,000 or more, depending on the plan. Consider: If you anticipate frequent doctor visits or prescriptions, a plan with a lower deductible might be more cost-effective despite potentially higher premiums.

Example: Imagine you need a $2,500 medical procedure. With a $1,000 deductible, you'd pay $1,000, and insurance covers the remaining $1,500. With a $5,000 deductible, you'd be responsible for the entire $2,500.

Out-of-Pocket Maximums: This is your financial safety net. It's the most you'll pay for covered services in a year, including deductibles, copays, and coinsurance. Medicare Advantage plans cap out-of-pocket costs at $8,300 in 2023. Private insurance plans often have similar caps, but they can vary widely. Crucial Insight: Out-of-pocket maximums are crucial for protecting yourself from catastrophic expenses. Choose a plan with a maximum you can afford, especially if you have chronic conditions or anticipate major medical needs.

Practical Tip: Review your expected healthcare needs for the year and choose a plan with an out-of-pocket maximum that aligns with your budget and risk tolerance.

Medical Insurance: Divorce and Spousal Coverage

You may want to see also

Explore related products

![]()

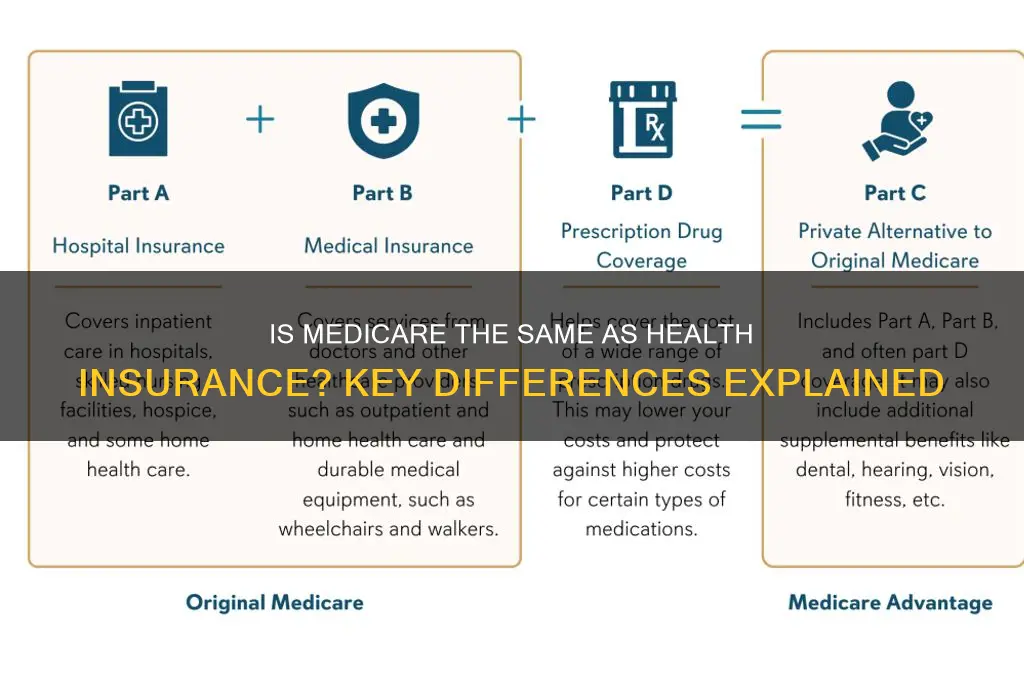

Medicare Parts: A, B, C, and D Explained

Medicare is often confused with traditional health insurance, but it’s a federal program designed primarily for individuals aged 65 and older, though younger people with certain disabilities or conditions may also qualify. Unlike private health insurance, which varies widely in coverage and cost, Medicare is standardized into distinct parts—A, B, C, and D—each serving a specific purpose. Understanding these parts is crucial for maximizing benefits and avoiding gaps in coverage.

Part A: Hospital Insurance

Part A covers inpatient hospital stays, skilled nursing facility care, hospice care, and some home health services. Most beneficiaries don’t pay a premium for Part A if they or their spouse paid Medicare taxes while working. However, it’s not all-inclusive; for example, it doesn’t cover long-term care or custodial care. A common misconception is that Part A fully covers hospital costs, but beneficiaries are responsible for deductibles ($1,632 per benefit period in 2023) and coinsurance after 60 days of hospitalization. Pro tip: Review your hospital stay classification—observation vs. inpatient—as only inpatient stays count toward Part A coverage.

Part B: Medical Insurance

Part B covers outpatient services, including doctor visits, preventive care, lab tests, and durable medical equipment. Unlike Part A, Part B requires a monthly premium, which in 2023 is $164.90 (or higher for higher-income individuals). It also has an annual deductible ($226 in 2023) and typically covers 80% of approved services, leaving beneficiaries to pay the remaining 20%. This cost-sharing structure highlights why many pair Part B with supplemental insurance. Caution: Failing to enroll in Part B when first eligible can result in late penalties, increasing the premium by 10% for each 12-month period you delay.

Part C: Medicare Advantage Plans

Part C, also known as Medicare Advantage, is an alternative to Original Medicare (Parts A and B). Offered by private insurers, these plans often include additional benefits like vision, dental, and prescription drug coverage. They typically operate as HMOs or PPOs, with provider networks and out-of-pocket maximums. While Part C can offer more comprehensive coverage, it may limit provider choice and require referrals for specialists. Example: A Medicare Advantage plan might include gym memberships or telehealth services, which Original Medicare doesn’t cover. Key takeaway: Compare plans annually during open enrollment, as benefits and costs can change.

Part D: Prescription Drug Coverage

Part D provides prescription drug coverage, which is not included in Original Medicare. Offered through private insurers, these plans vary in formularies (lists of covered drugs), costs, and pharmacies. Beneficiaries pay a monthly premium, deductible, and copays or coinsurance based on the drug tier. For instance, generic drugs typically have lower copays than brand-name drugs. A critical detail is the coverage gap (aka the “donut hole”), though the Affordable Care Act has reduced costs here. Practical tip: Use Medicare’s Plan Finder tool to compare Part D plans based on your specific medications, as costs can differ dramatically.

In summary, Medicare’s parts work together to provide comprehensive coverage, but each has unique features and limitations. Parts A and B form the foundation, while Parts C and D offer expanded options. Understanding these distinctions ensures beneficiaries can navigate the system effectively, avoiding unexpected costs and maximizing their healthcare benefits.

Will Insurance Cover Branded Titles? Understanding Your Policy's Fine Print

You may want to see also

Explore related products

![]()

Does Medicare Replace Private Health Insurance?

Medicare and private health insurance serve distinct purposes, often complementing rather than replacing each other. Medicare, a federal program, primarily covers individuals aged 65 and older, as well as younger people with certain disabilities or conditions. It consists of several parts: Part A (hospital insurance), Part B (medical insurance), Part C (Medicare Advantage), and Part D (prescription drug coverage). While Medicare provides a robust foundation, it does not cover all healthcare costs, leaving gaps that private insurance can fill.

Consider the example of prescription medications. Medicare Part D helps with drug costs, but it often includes deductibles, copayments, and coverage gaps (the "donut hole"). Private insurance plans, particularly those offered through employers or purchased individually, may offer more comprehensive prescription coverage, reducing out-of-pocket expenses. Similarly, Medicare typically does not cover dental, vision, or hearing care, which are often included in private health insurance plans. This highlights how private insurance can supplement Medicare rather than be replaced by it.

From a financial perspective, relying solely on Medicare can expose individuals to significant costs. For instance, Medicare Part A has a deductible of $1,632 per benefit period for hospital stays, and Part B requires a monthly premium and a $226 annual deductible. Private insurance plans, especially those with supplemental policies like Medigap, can help cover these expenses. Medigap policies, for example, can pay for copayments, coinsurance, and deductibles, providing a safety net that Medicare alone does not offer.

However, the decision to retain private insurance alongside Medicare depends on individual needs and circumstances. For those with employer-sponsored health plans, it’s often advisable to keep the private insurance, especially if it offers better coverage for specific needs like specialist visits or chronic conditions. Conversely, individuals without access to employer plans might find that Medicare, combined with a Medigap policy and Part D plan, suffices. Evaluating the costs, benefits, and coverage gaps of both options is crucial for making an informed decision.

In summary, Medicare does not fully replace private health insurance but rather works alongside it to provide comprehensive coverage. By understanding the limitations of Medicare and the strengths of private insurance, individuals can tailor their healthcare strategy to minimize costs and maximize benefits. Whether through supplemental policies or retaining employer-sponsored plans, combining Medicare with private insurance often yields the most effective protection against healthcare expenses.

Medical Insurance Plans: Two Types, Many Options

You may want to see also

Frequently asked questions

Medicare is a type of health insurance, but it is specifically a federal program primarily for people aged 65 and older, as well as certain younger individuals with disabilities or specific medical conditions.

Medicare coverage differs from private health insurance. It typically includes hospital insurance (Part A), medical insurance (Part B), and optional prescription drug coverage (Part D), but may require additional plans like Medicare Advantage (Part C) for more comprehensive benefits.

Medicare can replace private health insurance for eligible individuals, but it may not cover all the same services. Some people choose to supplement Medicare with additional plans or Medigap policies to fill coverage gaps.

Medicare is not entirely free. While Part A is premium-free for most enrollees, Parts B and D require monthly premiums, and there are deductibles, copayments, and coinsurance costs. Additional plans like Medicare Advantage or Medigap also come with their own costs.