Finding health insurance for yourself can be a daunting task, but it’s a crucial step in ensuring financial security and access to quality healthcare. Start by assessing your needs, such as preferred doctors, prescription coverage, and budget, to narrow down your options. Research available plans through your employer, government marketplaces like Healthcare.gov, or private insurers, comparing premiums, deductibles, and out-of-pocket costs. Consider factors like network coverage, whether you need specialized care, and any subsidies or tax credits you may qualify for. If you’re self-employed or without employer-sponsored options, explore individual plans or short-term coverage. Consulting a licensed insurance broker or using online comparison tools can simplify the process and help you make an informed decision tailored to your health and financial situation.

Explore related products

What You'll Learn

- Understand Coverage Needs: Assess your health, budget, and preferred doctors/hospitals for tailored insurance

- Compare Plan Types: Explore HMOs, PPOs, EPOs, and HDHPs to match your needs

- Use Marketplaces: Check Healthcare.gov or state exchanges for subsidized plans

- Review Employer Options: Evaluate workplace insurance benefits and costs

- Check Eligibility: Determine if you qualify for Medicaid, Medicare, or discounts

![]()

Understand Coverage Needs: Assess your health, budget, and preferred doctors/hospitals for tailored insurance

Your health insurance should fit you like a well-tailored suit, not a one-size-fits-all poncho. Start by taking your own health pulse. Are you a marathon runner with a pristine medical history, or do you manage chronic conditions requiring regular specialist visits? Be honest about your current health status, including any pre-existing conditions. This self-assessment is crucial because it directly impacts the level of coverage you'll need. Someone with diabetes, for instance, will require a plan that covers insulin, regular check-ups, and potential complications, while a healthy 25-year-old might prioritize lower premiums and a higher deductible.

Think of it as a risk assessment: the more health risks you have, the more comprehensive your coverage should be.

Budget is your reality check. Health insurance isn't just about premiums; it's a complex equation of deductibles, copays, and out-of-pocket maximums. Calculate your monthly healthcare expenses, including prescriptions and anticipated doctor visits. Are you comfortable with a higher deductible and lower monthly payments, or do you prefer predictable costs with a lower deductible? Remember, a plan with a $1,000 deductible might seem appealingly affordable until you factor in the $300 monthly premium and 20% copay for specialist visits. Online calculators can help you estimate your annual healthcare costs and find a plan that aligns with your financial reality.

Imagine your budget as a pie chart: how much can you realistically allocate to healthcare without sacrificing other essential expenses?

Don't underestimate the power of familiarity. If you have a trusted doctor or a preferred hospital, ensure they're in-network with the plans you're considering. Out-of-network care can be significantly more expensive, and some plans may not cover it at all. Research provider directories carefully, and don't hesitate to call your doctor's office to confirm their participation in specific insurance networks. Remember, continuity of care is important for managing chronic conditions and building a strong patient-doctor relationship.

Finally, consider your lifestyle and future plans. Are you planning to start a family soon? Do you travel frequently and need coverage outside your state? Some plans offer maternity care, while others provide international coverage. Think about your potential healthcare needs in the next year or two and choose a plan that offers the flexibility and coverage you might require. It's better to be over-prepared than caught off guard by unexpected medical expenses.

Medical Treatment Denial: Insured Patients Face Doctor Rejections

You may want to see also

Explore related products

![]()

Compare Plan Types: Explore HMOs, PPOs, EPOs, and HDHPs to match your needs

Choosing the right health insurance plan requires understanding the distinct features of HMOs, PPOs, EPOs, and HDHPs. Each type caters to different priorities, whether it’s cost control, flexibility, or access to specialists. Start by evaluating your healthcare habits, budget, and preferences to narrow down the options. For instance, if you rarely visit the doctor and want lower premiums, a High-Deductible Health Plan (HDHP) paired with a Health Savings Account (HSA) might align with your needs. Conversely, if you prioritize a broad network of providers without referrals, a Preferred Provider Organization (PPO) could be more suitable.

HMOs (Health Maintenance Organizations) are ideal for those who value cost efficiency and are comfortable with a primary care physician (PCP) managing their care. These plans typically require referrals to see specialists and limit coverage to in-network providers, except in emergencies. While HMOs offer lower premiums and out-of-pocket costs, they lack flexibility for out-of-network care. For example, a 30-year-old individual with no chronic conditions might find an HMO sufficient, as it covers preventive care and basic medical needs without breaking the bank.

PPOs (Preferred Provider Organizations) provide greater flexibility by allowing you to see any doctor or specialist without a referral, though staying in-network reduces costs. Premiums for PPOs are higher than HMOs, but they’re a better fit for those who want the freedom to choose providers or anticipate needing out-of-network care. For instance, a family with children who frequently see multiple specialists might prefer a PPO to avoid the hassle of referrals and higher out-of-network fees.

EPOs (Exclusive Provider Organizations) combine elements of HMOs and PPOs, offering lower costs than PPOs but requiring in-network care, except in emergencies. Unlike HMOs, EPOs typically don’t require referrals to see specialists. This plan type is ideal for individuals who want a balance between affordability and flexibility within a specific network. A young professional with moderate healthcare needs might find an EPO appealing, as it provides access to specialists without the need for referrals while keeping costs manageable.

HDHPs (High-Deductible Health Plans) pair with HSAs, offering tax advantages and lower premiums but higher deductibles. These plans are best for those who are generally healthy and want to save on premiums while preparing for unexpected medical expenses. For example, a 25-year-old with no chronic conditions could contribute $3,850 annually (the 2023 individual HSA contribution limit) to cover potential costs, while enjoying the tax benefits of the HSA. However, HDHPs may not be suitable for those who require frequent medical care, as the high deductible must be met before most services are covered.

In summary, the choice between HMOs, PPOs, EPOs, and HDHPs hinges on your healthcare needs, budget, and preference for provider flexibility. Assess your medical history, anticipated care requirements, and financial situation to select a plan that aligns with your priorities. For instance, if cost is your primary concern, an HMO or HDHP might be best, while a PPO or EPO offers more flexibility at a higher price. Always review plan details, including deductibles, copays, and network restrictions, to ensure the plan meets your specific needs.

Illinois Straight Medicaid: Which Insurance Companies are Accepted?

You may want to see also

Explore related products

![]()

Use Marketplaces: Check Healthcare.gov or state exchanges for subsidized plans

One of the most effective ways to find affordable health insurance for yourself is by exploring government-run marketplaces like Healthcare.gov or your state’s health insurance exchange. These platforms are designed to simplify the process of comparing and purchasing plans, often with subsidies that lower your costs based on income. For example, if you earn between 100% and 400% of the federal poverty level (FPL), you may qualify for premium tax credits that reduce your monthly premiums. In 2023, for a single individual, this income range translates to approximately $13,590 to $54,360 annually.

To get started, visit Healthcare.gov and create an account. The platform will guide you through a series of questions about your income, household size, and location to determine your eligibility for subsidies. If your state operates its own exchange (e.g., Covered California or New York State of Health), you’ll be redirected there automatically. Pro tip: Gather documents like your most recent tax return, pay stubs, and Social Security numbers beforehand to streamline the application process.

Comparing plans on these marketplaces requires attention to detail. Beyond premiums, consider deductibles, copays, and out-of-pocket maximums. For instance, a plan with a lower monthly premium might have a higher deductible, meaning you’ll pay more upfront before coverage kicks in. Conversely, a higher-premium plan may offer lower out-of-pocket costs for services like doctor visits or prescriptions. Use the marketplace’s filtering tools to narrow options based on your priorities, such as preferred providers or specific medications.

A common misconception is that marketplace plans are only for low-income individuals. In reality, even middle-income earners can benefit from subsidies, especially during open enrollment or special enrollment periods (triggered by life events like job loss or marriage). For example, a 30-year-old earning $40,000 annually in Texas could pay as little as $100 per month for a mid-tier plan after subsidies. To maximize savings, apply during open enrollment (typically November 1 to January 15) or within 60 days of a qualifying event.

Finally, don’t overlook the value of navigator programs or brokers who specialize in marketplace plans. These professionals can help you navigate complex eligibility rules and plan details at no additional cost. For instance, a navigator might explain how cost-sharing reductions (CSRs) can lower your deductible and copays if you qualify. By leveraging these resources and understanding the mechanics of subsidies, you can secure a plan that fits both your health needs and budget.

Why Big Companies Offer Lower Health Insurance Premiums: Key Factors

You may want to see also

Explore related products

![]()

Review Employer Options: Evaluate workplace insurance benefits and costs

If you're currently employed, your workplace might be your first stop in the quest for health insurance. Many employers offer health insurance as part of their benefits package, and this can be a cost-effective way to secure coverage. However, not all employer-provided plans are created equal, and it's essential to evaluate your options carefully.

Understanding Your Employer's Offerings

Begin by requesting a detailed summary of the health insurance plans available through your employer. This document should outline the different tiers of coverage, such as Bronze, Silver, Gold, and Platinum, each with varying levels of premiums, deductibles, and out-of-pocket costs. For instance, a Gold plan typically has higher monthly premiums but lower deductibles, making it suitable for individuals who anticipate frequent medical visits. In contrast, a Bronze plan might be more affordable monthly but could result in higher costs when you need medical services.

Analyzing Costs and Coverage

When reviewing these plans, consider your current health status and anticipated medical needs. If you're generally healthy and rarely visit the doctor, a high-deductible plan with a Health Savings Account (HSA) could be advantageous. HSAs allow you to save pre-tax dollars for medical expenses, providing a tax benefit and a way to save for future healthcare costs. On the other hand, if you have ongoing medical conditions or require regular prescriptions, a plan with lower out-of-pocket costs might be more suitable, despite potentially higher premiums.

Comparing Employer Plans to Individual Market Options

It's also crucial to compare your employer's offerings with plans available on the individual market. In some cases, you might find more affordable or comprehensive coverage outside of your workplace. However, be mindful of the tax implications. Employer-sponsored insurance is often provided pre-tax, reducing your taxable income. If you opt for an individual plan, you may need to pay taxes on the entire premium, which could offset any potential savings.

Negotiating and Customizing Your Coverage

Don't be afraid to negotiate or seek clarification on any aspects of the employer-provided plans. Some companies offer flexible benefits, allowing employees to customize their coverage. For example, you might be able to opt for a higher level of dental or vision care if these are priorities for you. Additionally, inquire about any wellness programs or incentives that could further reduce your healthcare costs. Many employers now offer discounts or rewards for healthy behaviors, such as gym memberships or smoking cessation programs.

Making an Informed Decision

Evaluating employer-provided health insurance requires a thorough understanding of your own healthcare needs and a careful comparison of costs and benefits. By analyzing the specifics of each plan, considering your health status, and exploring all available options, you can make an informed decision that ensures you have the right coverage at the best possible price. Remember, the goal is to find a balance between monthly premiums and potential out-of-pocket expenses, ensuring you're protected financially while also receiving the necessary medical care.

How Health Insurance Companies Create Barriers to Healthcare Access

You may want to see also

Explore related products

![]()

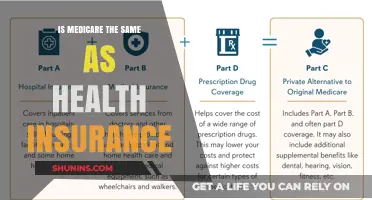

Check Eligibility: Determine if you qualify for Medicaid, Medicare, or discounts

Before diving into private health insurance plans, it’s crucial to explore whether you qualify for government-funded programs or discounts. Medicaid and Medicare are two primary options that can significantly reduce your healthcare costs, but eligibility depends on factors like income, age, disability status, and family size. Start by visiting the official Healthcare.gov website or your state’s Medicaid portal to assess your eligibility. These programs are designed to assist low-income individuals, seniors, and people with disabilities, offering comprehensive coverage at little to no cost.

For Medicaid, eligibility varies by state, but generally, individuals earning up to 138% of the federal poverty level (FPL) qualify. For example, in 2023, this translates to approximately $18,754 for a single person. Families with children, pregnant women, and adults with disabilities often have additional pathways to qualify. To apply, gather documents like pay stubs, tax returns, and proof of residency, then submit them through your state’s Medicaid office or online portal. Approval times vary, but you’ll receive a decision within 45 days.

Medicare, on the other hand, is primarily for individuals aged 65 and older, though younger people with certain disabilities or End-Stage Renal Disease (ESRD) may also qualify. Part A (hospital insurance) is typically free if you or your spouse paid Medicare taxes for at least 10 years. Part B (medical insurance) requires a monthly premium, which in 2023 starts at $164.90 but can increase based on income. If you’re nearing 65, enroll during your Initial Enrollment Period, which begins three months before your birthday month and ends three months after.

Discounts on private insurance plans are another avenue to explore, particularly if you don’t qualify for Medicaid or Medicare. The Affordable Care Act (ACA) offers premium tax credits for individuals earning between 100% and 400% of the FPL. For instance, a single person earning up to $54,360 in 2023 may qualify. Use the Healthcare.gov subsidy calculator to estimate your savings. Additionally, some insurers provide discounts for healthy lifestyles, such as nonsmoker rates or fitness program incentives.

Finally, don’t overlook local and state-specific programs that may supplement federal options. For example, some states have expanded Medicaid to cover more residents, while others offer health insurance pools for high-risk individuals. Nonprofit organizations and community health centers may also provide low-cost or sliding-scale services. By thoroughly checking your eligibility for these programs, you can maximize your coverage while minimizing out-of-pocket expenses.

Pradhan Mantri Insurance: Application Process Simplified

You may want to see also

Frequently asked questions

Begin by assessing your healthcare needs, budget, and preferred coverage options. Use online marketplaces like Healthcare.gov (for ACA plans) or private insurance websites to compare plans. You can also consult with a licensed insurance broker for personalized guidance.

Consider monthly premiums, deductibles, copayments, out-of-pocket maximums, network coverage (in-network vs. out-of-network providers), prescription drug coverage, and whether your preferred doctors and hospitals are included in the plan.

Yes, you can purchase individual health insurance through the Health Insurance Marketplace, private insurers, or professional associations. Self-employed individuals may also qualify for tax deductions on premiums.

PPOs offer flexibility to see any doctor but cost more; HMOs require choosing a primary care physician and referrals for specialists but are typically cheaper; HDHPs have lower premiums but higher deductibles and often pair with Health Savings Accounts (HSAs).

Yes, if you qualify based on income, you may be eligible for premium tax credits or cost-sharing reductions through the Health Insurance Marketplace. Medicaid and CHIP also provide low-cost or free coverage for eligible individuals.