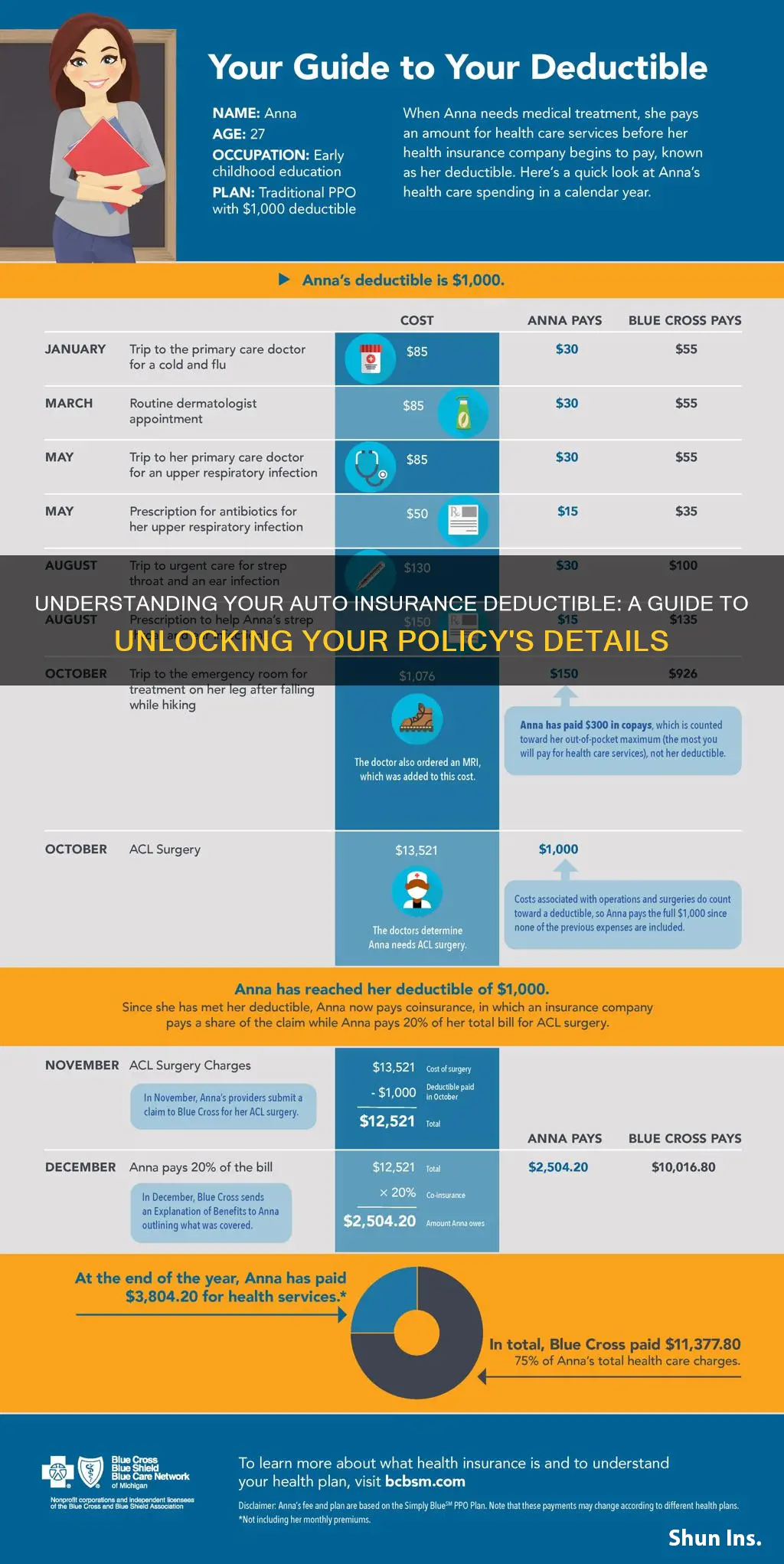

If you're unsure about your auto insurance deductible, there are several ways to find out. Your car insurance deductible is the amount you pay out of pocket before your insurance coverage kicks in. This amount is usually listed on your proof of insurance card, declarations page, or policy documents. You can also contact your insurance company to ask about your deductible. It's important to know your deductible amount, as it will affect how much you pay for your policy and how much you'll need to pay in the event of a claim.

| Characteristics | Values |

|---|---|

| Where to find your car insurance deductible | On your proof of insurance card, declarations page, and policy documents |

| When to pay your car insurance deductible | When you submit a claim that uses a specific coverage type |

| Choosing your car insurance deductible | The higher the deductible, the lower the insurance premium and vice versa |

Explore related products

What You'll Learn

![]()

Where to find your auto insurance deductible

Your auto insurance deductible is the amount you pay out of pocket when filing a car insurance claim. It is one of the most important numbers to know about your insurance policy, so you should always know where to look to find it. Your car insurance deductible is listed in several places:

- Your proof of insurance card

- The declarations page of the policy document

- Official policy documents

- By asking your insurer

Your proof of insurance card usually has a brief summary of your coverage. The declarations page also contains other important information about your coverage, including your rates, payment frequency, and details about what's covered. If you can't find your deductible on any of your documents, a quick call to your insurance company should help.

Spouse Insurance: Auto Exclusion in Georgia

You may want to see also

Explore related products

![]()

How auto insurance deductibles work

An auto insurance deductible is the amount you pay out of pocket when filing a car insurance claim. It is the amount you pay before your insurance company covers the remaining costs.

When buying an insurance policy, you can choose between a low and high deductible. A low deductible means a higher insurance rate, while a high deductible means a lower insurance rate. For example, if you have a $500 deductible and $3,000 in damage from a covered accident, your insurer will pay $2,500, and you will pay the remaining $500.

The most common deductible amount is $500, but deductibles can range from $0 to $2,000. When choosing a deductible amount, you should consider your financial situation and how likely you are to file an insurance claim. If you choose a high deductible, you will have lower monthly payments but may be stuck with a large bill if you are in an at-fault accident. On the other hand, a low deductible will result in higher monthly payments but lower out-of-pocket costs if you are in an accident.

It is important to note that deductibles are applied to each claim you make, and you are responsible for paying the deductible every time you file a claim. Additionally, different types of insurance coverage may have different deductibles. Comprehensive and collision coverage typically require a deductible, while minimum coverage does not.

Gap Insurance: Do I Need It?

You may want to see also

Explore related products

![]()

Choosing your auto insurance deductible

- Risk assessment: Evaluate your risk of filing an insurance claim. If you have a history of speeding tickets, prior at-fault accidents, or frequently drive in high-risk areas, you may be more likely to file a claim. In such cases, a lower deductible with a higher premium might be more suitable. On the other hand, if you have a safe driving record and are less likely to file a claim, you could opt for a higher deductible to reduce your monthly costs.

- Vehicle value: Consider the value of your car. If your car is older or has a lower value, a lower deductible may be preferable. This is because the insurance payout may not exceed the cost of repairs, even with a higher deductible. Conversely, for more expensive cars, a higher deductible can help offset the higher insurance rates.

- Financial situation: Assess your financial situation and savings. If you have sufficient savings or an emergency fund, you may be comfortable with a higher deductible, as it will lower your monthly insurance costs. On the other hand, if a large unexpected bill would be a financial burden, a lower deductible with higher monthly premiums may be a better option.

- Claim likelihood: Determine how likely you are to file a claim. If you have a history of accidents or engage in high-risk driving behaviours, you may be more likely to file a claim. In this case, a lower deductible might be more appropriate. Conversely, if you are a cautious driver with a clean record, a higher deductible could be a good choice.

- Affordability: Choose a deductible that you can comfortably afford to pay in the event of a claim. Ensure that the deductible amount does not exceed your financial capabilities, as you will be responsible for paying it each time you file a claim.

- Lender requirements: If you have taken out a loan or leased a vehicle, check with your lender or leasing company for any specific deductible requirements. They may have maximum deductible limits that you need to adhere to.

Remember, a higher deductible typically results in lower insurance rates, but it also means higher out-of-pocket expenses if you need to file a claim. On the other hand, a lower deductible leads to higher monthly premiums but provides more financial protection in the event of an accident. Carefully consider your personal circumstances and financial situation when selecting your auto insurance deductible.

Farmers Auto Insurance: Good Option?

You may want to see also

Explore related products

![]()

When to pay your auto insurance deductible

You will need to pay your auto insurance deductible when you file a claim under a coverage that carries a deductible. This means that you will pay your deductible every time you file a claim that uses a specific coverage type. For example, if you have comprehensive coverage and need to file a claim, you will pay your comprehensive coverage deductible.

There are some instances where you won't need to pay your deductible. If you are in an accident where another driver is at fault, you won't need to pay a deductible as the at-fault driver's liability insurance will cover the cost of your repairs. Similarly, if the claim you're filing is covered under liability insurance, which covers injuries and property damage in accidents you are at fault for, you won't need to pay a deductible.

Your deductible may also be waived in certain circumstances. For example, if you have comprehensive coverage and need to make a claim to repair windshield glass damage, your deductible may be waived.

It's important to note that your deductible applies per accident rather than once a year. Additionally, you will need to pay your deductible upfront before your insurance company covers the remaining cost of repairs or replacements.

Auto Insurance: Protecting Your Assets

You may want to see also

Explore related products

![]()

How auto insurance deductibles affect your premium

Choosing a higher deductible for your auto insurance will result in a lower premium, as you are assuming more financial responsibility in the event of a claim. This means that you will pay more out of pocket for repairs, but your monthly insurance payments will be cheaper. For example, increasing a deductible from $200 to $500 could reduce collision and comprehensive coverage costs by 15% to 30%, according to the Insurance Information Institute. Moving to a $1,000 deductible may save you 40% or more.

On the other hand, a lower deductible will increase your premium payments. If you don't have an at-fault accident resulting in a claim, you will have paid more for your insurance than someone with a higher deductible.

The deductible you choose will depend on your financial situation and personal preference. A higher deductible could lower your premiums, but if it's too high, it may strain your finances if you need to pay it. A lower deductible will make it easier to handle a claim financially, but your premiums will be higher.

Comprehensive Auto Insurance: Necessary Protection or Unnecessary Expense?

You may want to see also

Frequently asked questions

You can find your auto insurance deductible on your proof of insurance card, declarations page, and policy documents.

A car insurance deductible is the amount you pay out of pocket towards a claim before your insurance covers the rest.

You pay your deductible every time you file a claim under a coverage that carries a deductible. Your insurance company will then cover the remaining cost.

Collision, comprehensive, uninsured motorist, and personal injury protection coverages typically have a car insurance deductible.

The higher you set your deductible, the lower your car insurance premiums will be. However, choosing a lower deductible means you'll pay a higher premium. It's important to select a deductible that you can comfortably afford in case you need to file a claim.