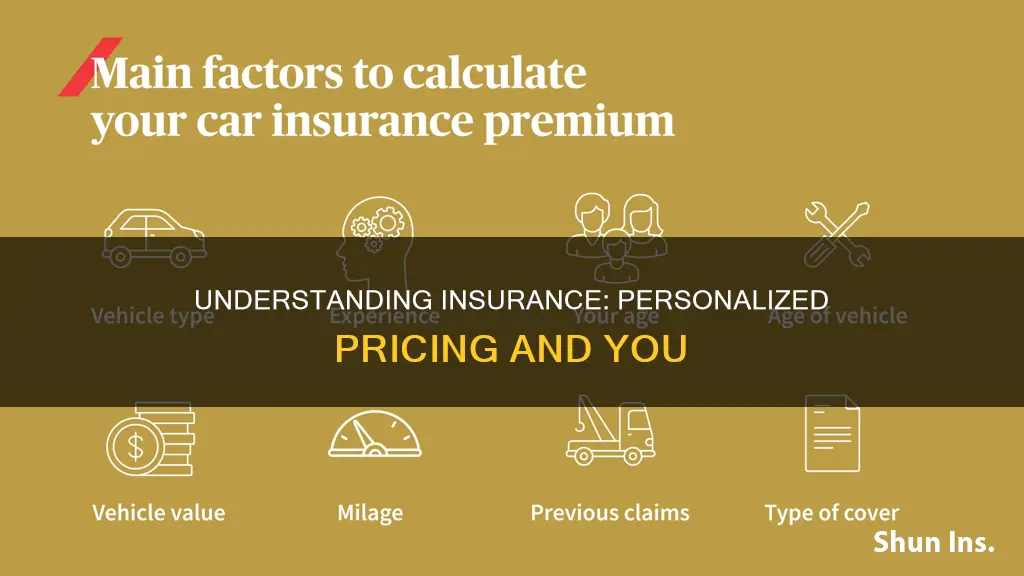

Insurance companies use a multitude of factors to determine the cost of insurance premiums for their customers. These factors include personal risk factors, such as age, location, and credit score, as well as the company's own costs and spending on claims. While the specific formula used to calculate premiums varies from company to company, understanding these factors can help customers make informed decisions about their insurance choices.

| Characteristics | Values |

|---|---|

| Insurance scores | Used to predict the likelihood a customer will file an insurance claim |

| Credit scores and history | Used to determine the premium on insurance |

| Age | Premiums can be up to 3 times higher for older people than for younger ones |

| Location | Where you live has a big effect on your premiums |

| Tobacco use | Insurers can charge tobacco users up to 50% more than those who don’t use tobacco |

| Individual vs. family enrollment | Insurers can charge more for a plan that also covers a spouse and/or dependents |

| Plan category | There are five plan categories – Bronze, Silver, Gold, Platinum, and Catastrophic |

| Driving record | Insurance companies generally charge higher rates for drivers in their 20s |

| Gender | In most states, insurers can charge different rates for male and female drivers |

| Inflation | Rising costs from inflation can cause insurers to increase rates |

| Number of claims | An increase in the number of claims can cause insurers to raise rates |

Explore related products

What You'll Learn

![]()

Credit history and score

- Payment history (40%): This includes how well you've made payments on outstanding debts in the past. Making timely payments on bills, taxes, and fines can improve your score.

- Outstanding debt (30%): The amount of debt you currently hold is considered. Keeping credit card balances low can positively impact your score.

- Credit history length (15%): The duration of your credit history matters, and a longer history can contribute to a better score.

- Pursuit of new credit (10%): Recent applications for new lines of credit can affect your score.

- Credit mix (5%): The types of credit you have, such as credit cards, mortgages, or auto loans, are also considered.

It's important to note that insurance companies cannot solely rely on your credit history to deny coverage or set premiums. They must also consider other factors, such as claims history, the insured asset, and state regulations. Additionally, consumers are entitled to a free credit report annually from major credit reporting agencies, allowing them to identify and correct any errors that could impact their insurance scores.

Insuring Guns: Is It Common?

You may want to see also

Explore related products

![]()

Age, gender, and marital status

Age is a significant factor in determining insurance rates. Younger people are considered to be riskier clients, as they cause more accidents than older people. Therefore, insurance rates decrease as the insured gets older. However, not all states allow insurers to set rates based on age. For example, Massachusetts has rules against age-based rates, while Hawaii is the only state that does not allow insurance providers to consider age when determining premiums.

Gender is also a factor in insurance rates. Women are statistically safer drivers and are less likely to file a claim than men. As a result, they generally pay less for car insurance. Men, on the other hand, tend to pay higher insurance rates, especially at a younger age. By the age of 30, insurance rates for men and women become more comparable, and between the ages of 30 and 50, men even pay slightly less than women. However, it is important to note that some states, such as California, Hawaii, Massachusetts, Michigan, Montana, North Carolina, and Pennsylvania, have bans on using gender as a factor in auto insurance rates.

Marital status also plays a role in insurance pricing. Married people are considered less risky than single people, as they are assumed to be more stable and responsible. As a result, a married 20-year-old can pay up to 21% less for car insurance than a single 20-year-old.

Princeton WV: May Insurance Services for You

You may want to see also

Explore related products

![]()

Location

Insurers calculate your likelihood of an auto accident based on the state, city, or county in which you live. For example, residents of states with a high number of uninsured drivers, such as Mississippi, will be charged higher premiums to help cover the higher expenses associated with accidents. Similarly, states with extensive claim requirements, such as Michigan, tend to have higher insurance rates. Conversely, states with fewer cars on the road, such as Wisconsin, tend to have cheaper insurance.

The risk of vehicle theft or vandalism is calculated based on the city or neighborhood in which you live. If you live in a densely populated urban area, you may be at a higher risk of vehicle theft or vandalism. As a result, your insurance premium may be higher. On the other hand, if you live in an area with low crime rates and secure parking, you may be eligible for a discount on your premium.

Insurers also consider the type and frequency of claims filed in an area when calculating rates, as well as the parts and labor costs to fix your vehicle. For example, states prone to severe weather conditions such as floods, hurricanes, tornadoes, and snow may have higher insurance rates due to increased claims frequencies. Similarly, areas with poor road conditions and high traffic congestion increase the risk of auto accidents, resulting in higher insurance costs.

It is important to note that location is not the only factor influencing insurance premiums. Personal factors such as age, gender, marital status, driving history, and credit score also play a significant role in determining the cost of insurance.

Endoscopy: Surgery or Not?

You may want to see also

Explore related products

![]()

Driving record

When it comes to auto insurance, insurance companies will always check your driving record. They do this to assess your risk level and set your insurance premium accordingly. A driver's license is not a requirement for having a driving record; any driver can have an official record if they've been ticketed, had a license suspended, or been convicted of a traffic violation. Insurance companies can access this information with your driver's license number.

Insurance companies are looking for negative marks on your driving record that may indicate you are a high-risk driver. They consider accidents, excessive insurance claims, and traffic violations as the biggest red flags. Incidents such as speeding tickets, at-fault accidents, and DUIs/DWIs are also taken into account. The more incidents on your record, the higher your insurance rates are likely to be. For example, one accident can raise insurance rates by $80 per month, and one speeding ticket can raise rates by $45 per month.

The time incidents stay on your record can vary by state, though it typically ranges from three to five years. Some states, such as Virginia, allow drivers to earn one safety point per year for safe driving habits, and some allow drivers to take safe driving courses to remove points. However, some states don't have a point reduction system, and drivers will have to wait for points to fall off their driving record.

Insurance companies will also consider other factors when setting your premium, such as your credit score, age, where you live, and the type of car you drive.

Navigating the Insurance Billing Maze: Unraveling the 'Which Insurance to Bill' Conundrum

You may want to see also

Explore related products

![]()

Claim history

When it comes to determining insurance rates, insurance companies consider a variety of factors, including an individual's claim history. This information is used to assess the risk associated with providing coverage and calculating premium costs.

An individual's claim history is a record of insurance claims made over a certain period. In the case of car insurance, this typically includes claims made within the past three years, although insurance companies may review up to five years of driving history. For home insurance, claim history can include records of claims made on a particular property before the current owner or occupant.

For car insurance, claim history is an important factor in determining rates and can impact insurance premiums, especially if an individual has a high number of claims. The Claims and Underwriting Exchange (CUE) is another central database that stores records of incidents reported to insurance companies, even those that don't lead to a claim. CUE reports are typically stored for six years and are used by insurance providers to calculate premium costs based on an individual's claim history.

It's important to note that insurance companies may also consider other factors in addition to claim history, such as age, gender, location, and credit score, when determining insurance rates.

Porting Term Insurance: Navigating the Transition for Continued Coverage

You may want to see also

Frequently asked questions

There are five factors that can affect the price of health insurance: location, age, family size, tobacco use, and plan category.

The price of auto insurance is influenced by factors such as the age of the driver, the safety features of the car, the driver's credit score, the location of the driver, and the number of miles driven.

The price of home insurance is influenced by factors such as the location of the home, the age of the homeowner, and the credit score of the homeowner.

The price of pet insurance is influenced by factors such as the age and breed of the pet, the location of the owner, and the pet's health history.