Insurance rates vary depending on location, with factors such as crime rates, population density, weather, state laws, and road conditions affecting costs. For example, in the US, Detroit, Michigan, ranks as the most expensive city for car insurance, with an average of $5,300 per year, while Raleigh, North Carolina, is the cheapest, with Charlotte coming in second. In the UK, London is the most expensive city for car insurance, with an average of £816. These differences in insurance rates between cities can be attributed to varying levels of risk associated with specific locations, with more densely populated areas, higher crime rates, and unfavourable weather conditions often resulting in higher premiums.

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

What You'll Learn

![]()

Population density and crime rates

For instance, in Texas, full coverage car insurance in a large city like Houston is approximately $42 more per month than in smaller cities like Corpus Christi due to higher traffic volumes. Similarly, Detroit, Michigan, ranks as the most expensive city for car insurance, costing $5,300 per year, while Raleigh, North Carolina, has the cheapest rates.

The risk of theft or vandalism is also higher in densely populated urban areas, affecting insurance rates. Insurance companies consider the likelihood of theft or vandalism when calculating premiums, resulting in higher rates for areas with increased risk. Additionally, areas with a high cost of living tend to have higher insurance premiums since the cost of repairs and medical care is typically higher.

In contrast, rural areas with lower population densities generally have lower insurance rates due to reduced traffic and crime rates. However, they may face other risks, such as a higher likelihood of animal collisions. For example, Maine has the lowest car insurance rates, with full coverage averaging $103 per month, while Nevada, with its densely populated cities like Las Vegas and Reno, has the highest rates.

When determining insurance rates, companies consider various factors, including state regulations, weather conditions, crime rates, road risks, and the cost of living in a particular area. Crime rates, specifically car theft and vandalism, play a significant role in insurance premiums, with cities experiencing higher crime rates resulting in increased insurance costs.

Auto Insurance: Aunt's Policy Extension

You may want to see also

Explore related products

![]()

Repair and labour costs

Insurance rates vary across different cities due to factors such as population size, traffic congestion, accident rates, crime rates, weather, and the cost of repairs and labour. Repair and labour costs are higher in bigger cities, which contributes to higher insurance rates.

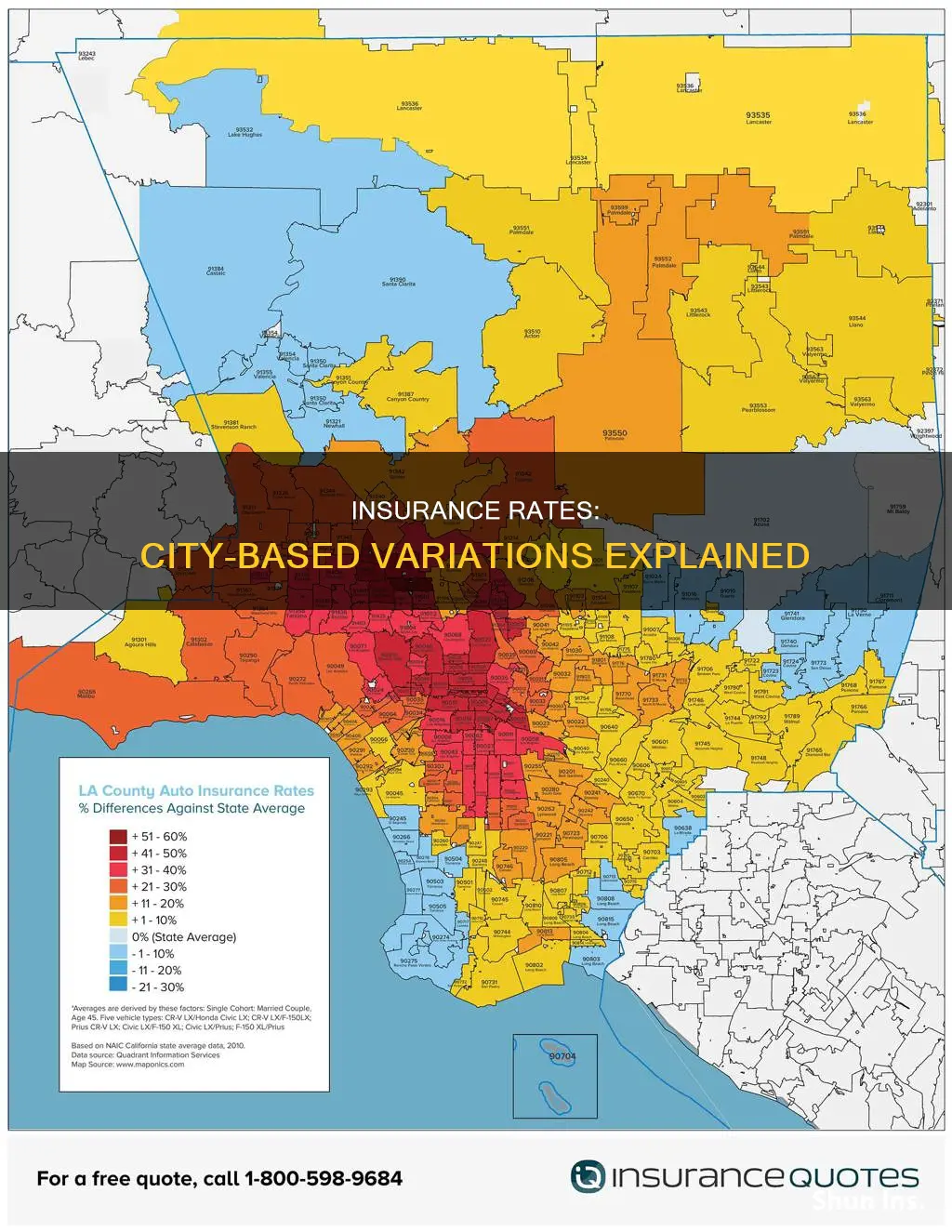

In general, urban areas with larger populations have higher insurance rates than smaller towns or rural areas. This is because busier roads and higher traffic congestion in cities lead to a higher likelihood of accidents, resulting in increased insurance claims. For example, in Texas, car insurance in a large city like Houston is approximately $42 more per month than in a smaller city like Corpus Christi. Similarly, within New York City, the Brooklyn neighbourhood of Brownsville has an average insurance cost of $562 per month, while the Upper East Side has an average cost of $279 per month.

The cost of repairs and labour is a significant factor in insurance rates. In bigger cities, these costs tend to be higher, which insurance companies reflect in their rates. The type of vehicle also influences repair costs, as luxury, sports, and electric cars are generally more expensive to repair, leading to higher insurance rates. Additionally, vehicles with higher-quality safety equipment may qualify for premium discounts, as insurers consider the safety features that protect occupants and reduce potential damage to other vehicles.

States with a history of severe weather, such as hurricanes, floods, hail, or snow, tend to have higher insurance rates due to the increased likelihood of weather-related damage. For example, Florida and Louisiana, which are prone to hurricanes and floods, have some of the highest insurance rates in the country. Similarly, Nevada, which experiences traffic congestion in cities like Las Vegas and Reno, has the highest insurance rates nationwide.

The prevalence of car theft and vandalism also impact insurance rates. Urban areas with higher crime rates tend to have higher insurance rates due to the increased risk of theft and vandalism. However, comprehensive coverage may be cheaper in certain urban areas compared to rural spots, as the risk of vandalism and theft decreases in the suburbs, while the risk of weather damage may increase.

Auto Insurance Transferability: Who Is Covered?

You may want to see also

Explore related products

![]()

Weather conditions

The frequency of weather-related claims also influences insurance rates. Cities or regions with a history of frequent property damage or weather-related claims often have higher premiums as insurers adjust their prices to cover potential losses. For example, states like Florida, Michigan, and California consistently have some of the highest insurance rates due to their higher minimum coverage requirements and inflated repair costs. In contrast, states like Maine and Vermont enjoy lower insurance averages due to their milder weather and fewer claims.

Weather patterns are not limited to extreme conditions; even mild weather patterns can impact insurance rates. Cities with favourable weather conditions often benefit from lower insurance rates, as the risk of weather-related damage is reduced. Additionally, areas with a low risk of natural disasters, such as hurricanes, floods, or hailstorms, typically experience lower insurance premiums.

It is worth noting that weather conditions are just one aspect considered by insurance companies when calculating premiums. Other factors, such as crime rates, population density, traffic congestion, and local regulations, also come into play when determining insurance rates for specific cities. However, weather conditions significantly influence insurance rates, especially in areas prone to severe weather events or those with a history of frequent weather-related claims.

Auto Insurance: Is Comprehensive Coverage Mandatory?

You may want to see also

Explore related products

![]()

Cost of living

The cost of living is a significant factor in determining insurance rates across different cities. Urban areas, for instance, often come with higher insurance premiums due to increased risks of vandalism, theft, and accidents. Higher population density also means more traffic congestion, resulting in higher accident probabilities and insurance rates.

In addition to population size, the cost of living in a city is influenced by the cost of healthcare and auto repairs. Cities with higher living costs tend to have more expensive insurance rates, as insurers must account for potential extra costs. For example, Detroit, Michigan, is ranked as the most expensive city for car insurance, with an average annual cost of $5,300. This is followed by New York City, with an average of over $4,700 per year.

The frequency of insurance claims also impacts insurance rates. Cities prone to natural disasters, such as hurricanes and floods, often face higher insurance costs. For instance, states like Florida and Louisiana experience higher insurance premiums due to their vulnerability to natural disasters. Similarly, areas with a high number of uninsured motorists tend to have higher insurance rates, as the risk of uninsured claims is greater.

The cost of living also varies with the cost and frequency of litigation, medical care, and car repair costs. Cities with higher litigation costs can drive up insurance rates, as insurers factor in the potential expenses. Additionally, areas with higher medical care and car repair costs can influence insurance rates, as these expenses are considered when setting premiums.

The cost of living in a particular city can significantly impact insurance rates. Insurers consider the cost of living when assessing the potential financial risks associated with a specific location. By analyzing factors such as population density, crime rates, and the frequency of natural disasters, insurers can adjust their rates accordingly.

Direct Line's Gap Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Natural disasters

Insurance companies classify some regions as high-risk areas for natural disasters, such as hurricanes, earthquakes, and floods. Coastal regions, for example, are more prone to hurricanes, while flood plains near large rivers face higher flood risks. In these high-risk areas, insurance coverage may be more restrictive, with higher deductibles and exclusions for certain types of damage.

The frequency and severity of natural disasters have increased due to climate change, which has resulted in reinsurance companies drastically increasing their rates for insurance companies. This, in turn, gets passed back to policyholders in the form of higher insurance rates.

The impact of natural disasters on insurance rates can vary across different cities. For instance, Florida and Louisiana often face natural disasters like hurricanes and floods due to their coastal locations. As a result, car insurance rates in these states tend to be higher than in other states. Similarly, Texas and Florida are projected to experience a significant increase in flood exposure by 2050, which will likely influence insurance rates in these states.

Additionally, local building codes and construction practices can also affect insurance rates in areas prone to natural disasters. Regions with stricter building codes may have lower insurance premiums due to a reduced risk of damage. On the other hand, areas with older homes that do not meet current building codes may find it challenging to obtain adequate insurance coverage.

Understanding the impact of natural disasters on insurance rates is essential for homeowners to make informed decisions and engage in effective financial planning and risk management.

Vehicle Ownership: Insurance Costs After Paying Off Loans

You may want to see also

Frequently asked questions

Insurance rates vary between cities due to factors such as crime rates, population density, weather, state laws, and road conditions. Cities with higher population densities tend to have higher insurance rates because busier roads mean a higher likelihood of accidents.

Detroit, Michigan, is the most expensive city for car insurance, with an average annual cost of $5,300. New York City is the second-priciest location for auto insurance, with an average cost of over $4,700. Other states with high insurance rates include Nevada, Florida, and Louisiana.

Raleigh, North Carolina, has the cheapest insurance rates, followed by Charlotte. Vermont, Idaho, Maine, and New Hampshire also have low insurance rates due to their smaller populations, lower accident rates, and lower percentages of uninsured motorists.

You can use online tools such as The Zebra's Dynamic Insurance Rating Tool or CarInsurance.com's rates by ZIP code calculator to estimate insurance rates for your city or ZIP code. These tools consider various factors, including location, age, vehicle type, and coverage level.