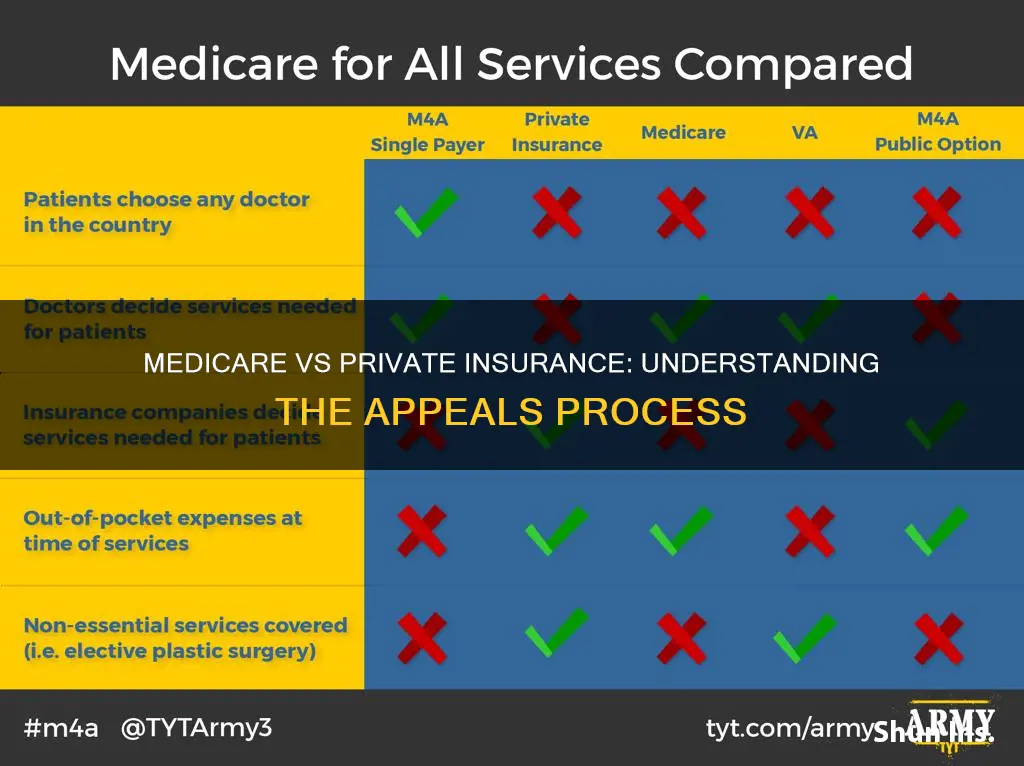

Medicare and private insurance plans differ in their costs, benefits, plan options, and coverage rules. Medicare is a federal government health insurance program for individuals 65 and older or those with qualifying disabilities, while private insurance is available to anyone. Medicare offers more coverage choices and combinations, while private insurance plans have a limited number of offices, hospitals, and healthcare providers in their network. Private insurance plans often offer more customization options and additional benefits such as dependent coverage, dental, vision, and mental health coverage. The costs of Medicare and private insurance plans depend on various factors, including age, location, premiums, out-of-pocket costs, deductibles, and coinsurance charges. When it comes to appeals, both Medicare and private insurance plans have processes in place to dispute coverage or payment decisions, with Medicare having five levels of appeals.

| Characteristics | Values |

|---|---|

| Number of coverage choices | Medicare surpasses private insurance |

| Flexibility of provider choice | Medicare offers more flexibility |

| Cost of premiums | Medicare premiums may be lower than private insurance |

| Out-of-pocket costs | Medicare Advantage and private insurance have yearly limits |

| Coverage rules and restrictions | Private insurance offers more customization options |

| Coverage for dependents | Private insurance typically covers dependents, while Medicare does not |

| Prescription drug coverage | Private insurance may offer more extensive coverage for certain medications |

| Age eligibility | Medicare is generally for individuals 65 and older, while private insurance has no age limit |

| Provider network | Private insurance plans have a limited number of offices, hospitals, and providers in their network |

Explore related products

What You'll Learn

![]()

Medicare appeal process: There are 5 levels of appeals

The Medicare appeal process is available if you disagree with a coverage or payment decision by Original Medicare, your Medicare Advantage or other Medicare health plan, or your Medicare drug plan. Before starting an appeal, you can ask your provider or supplier for any information to strengthen your appeal.

There are 5 levels of appeals. If you disagree with the decision made at any level of the process, you can generally proceed to the next level. At each level, you'll receive a decision letter with instructions on how to move to the next level of appeal.

Level 1: Health Plan Reconsideration

If you disagree with the initial decision from your plan, you or your representative can ask for a reconsideration by following the directions in the plan's initial denial notice and plan materials. If your appeal is for a service you haven't received yet, your doctor can request a reconsideration on your behalf.

Level 2: Review by an Independent Review Entity (IRE)

If your plan upholds their denial in your Level 1 appeal, they will automatically forward their reconsideration decision to an IRE to initiate a Level 2 appeal. The time taken by the IRE to respond depends on the type of appeal.

Level 3: Medicare Appeals Council Review

If you disagree with the IRE's decision, you can request a review by the Medicare Appeals Council. They will review your case and issue a decision.

Level 4: Federal District Court Review

If you are still dissatisfied with the decision, you can file an appeal with the Federal District Court. This level involves a judicial review of your case by a federal judge.

Level 5: Court of Appeals

The final level of appeal is the Court of Appeals. If you disagree with the decision made by the Federal District Court, you can request a review by the Court of Appeals.

The Medicare appeal process offers a structured mechanism for beneficiaries to challenge coverage and payment decisions made by Medicare plans. It ensures that individuals have the right to seek reconsideration and receive a fair assessment of their case at multiple levels.

Medical Insurance: Letter of Necessity Checks by Companies

You may want to see also

Explore related products

![]()

Private insurance: Coverage for dependents

Private insurance plans may be a more attractive option for those seeking coverage for their dependents, as Medicare plans do not offer this.

Private insurance plans can include coverage for spouses, children, and sometimes other relatives. In contrast, Medicare is only available to people aged 65 or older, or those with qualifying disabilities.

The Affordable Care Act (ACA) requires most employer plans to allow young adults to remain on a parent's plan until the age of 26. This has been credited with reducing the uninsured rate among young adults. Before the ACA, employers typically limited dependent eligibility for young adults to an age less than 26 and often imposed additional eligibility requirements.

According to a 2024 survey, 56% of young adults aged 18-25 were covered by an employer-sponsored plan. The likelihood of enrolling as a dependent decreases with age. Nearly all children (aged 0-17) with employer-sponsored coverage are enrolled as dependents, usually on a parent's plan. Young adults, particularly those aged 18-25, are more likely to be covered as dependents than adults overall (72% vs. 47%).

It is important to note that each health insurance policy has its own rules about who qualifies as a dependent. For example, some private plans may require that the dependent lives with the policyholder for more than half the year, or that they are financially dependent on them.

Life Insurance: Can You Sell When Seriously Ill?

You may want to see also

Explore related products

![]()

Medicare Advantage: Hospital stays and expedited appeals

If you disagree with a coverage or payment decision by Original Medicare, your Medicare Advantage or other Medicare health plan, you can file an appeal. There are five levels of appeals, and you can generally progress to the next level if you disagree with the decision made at the current level.

If you are in a hospital and you think your Medicare-covered services are ending too soon, you have the right to a fast appeal. This includes services you get from a hospital, skilled nursing facility, home health agency, comprehensive outpatient rehabilitation facility, or hospice. You must file an appeal within 65 days from the date on the initial denial notice sent by your plan. If you think your health could be seriously harmed by waiting the standard 30 days for a decision, you can ask your plan for an expedited appeal. The plan must give you its decision within 72 hours.

If you request an appeal within the deadline, you can stay in the hospital while you wait for the decision. Medicare will continue to cover your hospital stay as long as it is medically necessary. However, if you miss the deadline for a fast appeal, you may be responsible for the cost of the hospital stay past the original day of discharge.

If you are in a Medicare Advantage Plan, you can ask your plan for an appeal, but different rules apply. You will receive a Detailed Notice of Discharge, which explains why your hospital care is ending and lists any Medicare coverage rules related to your case. If your appeal is unsuccessful, you will not be held responsible for the cost of the 24-hour period while you waited for the decision. However, if you remain in the hospital after that, you may be responsible for the cost of your care if you do not win at a higher level.

Should You Cancel Your Medical Insurance?

You may want to see also

Explore related products

![]()

Medicare Part C: Out-of-pocket costs capped

Medicare Part C, also known as Medicare Advantage, is provided by private insurers but regulated by the federal government. Unlike Original Medicare, Part C plans have out-of-pocket maximums, which means there is a limit to how much you will spend on covered healthcare within a year. This is called the maximum out-of-pocket (MOOP) limit.

The MOOP for Medicare Part C plans in 2025 is $9,350 for in-network services and $14,000 for out-of-network services. Many Part C plans also offer lower out-of-pocket limits. Once you reach this dollar figure, your plan will pay 100% for all your covered healthcare costs for the remainder of the plan period.

It is important to note that the out-of-pocket maximum does not include the cost of prescriptions. If your Medicare Advantage plan includes Part D (prescription drug) coverage, the cost of your medications will not go towards your Part C out-of-pocket maximum.

While Medicare Part C has capped out-of-pocket costs, Original Medicare does not. This means that, with Original Medicare, there is no limit to how much you may have to pay out of pocket for covered healthcare services. However, you may be able to get supplemental coverage, such as a Medicare Supplement Insurance (Medigap) policy, which can help with out-of-pocket costs.

When comparing Medicare to private insurance, it is important to consider that both options may have different costs, benefits, plan options, and coverage rules. Some private plans may have higher deductibles to keep monthly premiums lower, while others may have higher monthly premiums and lower out-of-pocket costs. Medicare Part C plans have capped out-of-pocket costs, while Original Medicare does not, but it is important to consider all factors when deciding which option is best for you.

Medicare: Do Salespeople Knock on Doors?

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Private insurance premiums: Vary by age and location

Private insurance premiums vary based on several factors, including age and location.

Age is a significant factor in determining health insurance premiums. In general, older individuals tend to pay higher premiums than younger people. This is because older people typically develop health conditions as they age and, consequently, require more medical attention and incur higher costs for insurance companies. Most states in the US use age 21 as a base rate, applying a multiplier for individuals above this age. The premium multiplier is capped at 3.00 for older individuals, ensuring they do not pay more than three times the rate of a 21-year-old based solely on age.

Location also influences private insurance premiums. Pricing for medical products and services can vary by state and even city, resulting in different health insurance costs across geographic areas. The cost of living in a particular region impacts the pricing of insurance plans.

Other factors that affect private insurance premiums include tobacco use, the number of insured individuals, and the chosen plan category or tier. Tobacco users may pay significantly more for insurance, and adding dependents can increase costs. Different plan categories, such as Bronze, Silver, Gold, Platinum, and Catastrophic, offer varying balances of monthly premiums and out-of-pocket expenses.

It is worth noting that Original Medicare premiums may sometimes be lower than private insurance premiums, especially if an individual qualifies for premium-free Part A. However, Medicare Advantage and private plans have annual limits on out-of-pocket expenses, while Original Medicare does not.

Insuring Your Unborn Baby: Understanding Medicaid Coverage

You may want to see also

Frequently asked questions

Medicare is mostly for Americans aged 65 and over, while private insurance can be purchased by anyone. Medicare offers more coverage combinations and choices, while private insurance plans have a limited number of offices, hospitals, and healthcare providers that they contract with.

You can file an appeal if Medicare refuses to cover a health care service, supply, item, or drug that you think they should, or if they refuse to pay for a health care service, supply, item, or drug you already got. You must file an appeal within 65 days from the date on the initial denial notice sent by your plan.

There are 5 levels of appeals. If you disagree with the decision made at any level of the process, you can generally go to the next level.

The process for filing an appeal for private insurance varies depending on the insurance company and the specific plan. You will need to contact your insurance company to find out the specific process for filing an appeal.

The time it takes to complete the appeal process may vary depending on the specific case and the level of the appeal. For Medicare, the plan has a certain amount of time to respond to your initial appeal, which depends on the type of appeal being filed. For private insurance, there is no standard time frame for the appeal process, as it may vary depending on the insurance company and the specific plan.