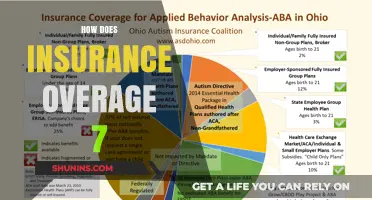

Insurance is a complex yet essential financial tool designed to protect individuals, businesses, and assets from unforeseen risks and losses. It operates on the principle of risk pooling, where policyholders pay premiums to an insurer, who then uses these funds to cover claims when insured events occur. The structure of insurance varies widely depending on the type—whether it’s health, auto, life, property, or liability—each tailored to address specific risks. Policies typically outline coverage limits, deductibles, and exclusions, ensuring clarity on what is protected and under what circumstances. Premiums are calculated based on factors like risk assessment, policyholder history, and the likelihood of claims, making insurance both a personalized and standardized product. Understanding how insurance works—from policy terms to claims processes—is crucial for maximizing its benefits and ensuring financial security in an unpredictable world.

| Characteristics | Values |

|---|---|

| Type of Insurance | Health, Life, Auto, Home, Travel, Business, Pet, Disability, etc. |

| Coverage | Varies by policy (e.g., liability, comprehensive, collision, critical illness) |

| Premiums | Monthly, quarterly, or annual payments; amount depends on risk factors. |

| Deductibles | Fixed amount paid by the policyholder before insurance coverage kicks in. |

| Policy Limits | Maximum amount the insurer will pay for a covered claim. |

| Risk Assessment | Based on age, health, driving record, location, occupation, etc. |

| Claims Process | Filing a claim, investigation, approval, and payout. |

| Renewability | Annual or term-based renewal options. |

| Exclusions | Specific conditions or events not covered by the policy. |

| Riders/Add-ons | Optional additional coverage for specific needs (e.g., accidental death). |

| Regulation | Governed by local, state, or national insurance regulatory bodies. |

| Payout Methods | Lump sum, installments, or reimbursement based on policy terms. |

| Underwriting | Process of evaluating risk and determining policy terms. |

| Policy Duration | Short-term (e.g., 6 months) or long-term (e.g., 10-30 years). |

| Digital Integration | Online quotes, claims filing, and policy management via apps/websites. |

| Global Trends | Increasing adoption of AI, telematics, and personalized policies. |

Explore related products

![Insurance Law and Policy: Cases and Materials [Connected eBook] (Aspen Casebook)](https://m.media-amazon.com/images/I/61KCOsTIc+L._AC_UY218_.jpg)

![Property and Casualty Insurance License Exam Study Guide: Property Casualty Insurance Book and Practice Test Questions [3rd Edition]](https://m.media-amazon.com/images/I/71MhA+5nDML._AC_UY218_.jpg)

What You'll Learn

- Types of Insurance: Life, health, auto, home, and business coverage options explained

- Policy Structure: Premiums, deductibles, coverage limits, and claim processes detailed

- Insurance Providers: Comparison of companies, agents, brokers, and online platforms

- Risk Assessment: How insurers evaluate risks to determine policy terms and costs

- Claims Process: Steps to file, investigate, and settle insurance claims efficiently

![]()

Types of Insurance: Life, health, auto, home, and business coverage options explained

Insurance is a multifaceted tool designed to protect individuals, assets, and businesses from financial loss. Understanding the types of insurance available is crucial for making informed decisions. Here’s a breakdown of five essential coverage options: life, health, auto, home, and business insurance.

Life Insurance: Securing Your Loved Ones’ Future

Life insurance provides a financial safety net for beneficiaries after the policyholder’s death. Term life insurance offers coverage for a specified period (e.g., 10, 20, or 30 years) and is ideal for those seeking affordable, temporary protection. Whole life insurance, on the other hand, provides lifelong coverage with a cash value component, making it a more expensive but permanent solution. For instance, a 30-year-old nonsmoker might pay $25–$35 monthly for a $500,000 term policy, while whole life premiums could exceed $100 monthly. The key takeaway? Choose based on your long-term financial goals and dependents’ needs.

Health Insurance: Navigating Medical Expenses

Health insurance offsets the cost of medical care, including doctor visits, hospitalizations, and prescriptions. Plans vary widely: HMOs require in-network providers, while PPOs offer more flexibility at higher costs. High-deductible health plans (HDHPs) pair with Health Savings Accounts (HSAs), allowing tax-free savings for medical expenses. For example, a family of four might pay $1,200–$1,500 monthly for a comprehensive PPO plan, while an HDHP could reduce premiums to $800–$1,000 with a $5,000 deductible. Pro tip: Evaluate your annual medical needs and budget to find the best fit.

Auto Insurance: Protecting Drivers and Vehicles

Auto insurance is legally required in most states and typically includes liability, collision, and comprehensive coverage. Liability covers damages to others in an accident, while collision and comprehensive protect your vehicle from accidents, theft, and natural disasters. For instance, a driver with a new car might opt for full coverage, paying $1,500–$2,000 annually, whereas someone with an older vehicle might choose liability-only for $500–$800. Caution: Skimping on coverage can lead to significant out-of-pocket costs in an accident.

Home Insurance: Safeguarding Your Property

Home insurance protects against damage to your house and personal belongings, as well as liability claims. Policies typically cover perils like fire, theft, and storms but exclude floods and earthquakes, requiring separate policies. For example, a standard policy for a $300,000 home might cost $1,200–$1,500 annually, while flood insurance adds $600–$1,000. Practical tip: Inventory your belongings and ensure your coverage limits reflect their value.

Business Insurance: Mitigating Operational Risks

Business insurance shields companies from financial losses due to lawsuits, property damage, and employee injuries. General liability insurance is essential for most businesses, covering claims like bodily injury and property damage. For instance, a small retail store might pay $500–$1,000 annually for general liability, while a construction company could spend $5,000–$10,000 due to higher risks. Additionally, workers’ compensation is mandatory in most states, covering employee injuries. Analysis: Tailor your coverage to your industry’s risks and legal requirements.

In summary, each type of insurance serves a distinct purpose, addressing specific risks and financial vulnerabilities. By understanding these options, you can build a comprehensive protection plan tailored to your needs.

Life Insurance: Target's Comprehensive Coverage Explained

You may want to see also

Explore related products

![]()

Policy Structure: Premiums, deductibles, coverage limits, and claim processes detailed

Insurance policies are the backbone of financial protection, but their structure can often seem like a maze of jargon and fine print. At the heart of every policy lies a delicate balance between premiums, deductibles, coverage limits, and claim processes—each element playing a critical role in determining both cost and protection. Understanding these components is essential for anyone looking to navigate the insurance landscape effectively.

Consider premiums, the recurring payments policyholders make to maintain coverage. These are not arbitrary; they are calculated based on risk factors such as age, health, location, and the type of coverage selected. For instance, a 30-year-old nonsmoker might pay $300 annually for a $500,000 life insurance policy, while a 50-year-old smoker could face premiums exceeding $1,200 for the same coverage. The takeaway? Premiums are a direct reflection of perceived risk, and understanding this can help you anticipate costs and shop for policies that align with your budget.

Deductibles, on the other hand, represent the out-of-pocket amount you must pay before insurance coverage kicks in. For example, in a health insurance policy with a $1,000 deductible, you’re responsible for the first $1,000 of medical expenses. Deductibles are a trade-off: higher deductibles typically lower your premiums, but they also mean greater financial responsibility in the event of a claim. A practical tip: if you’re generally healthy and rarely visit the doctor, opting for a high-deductible plan paired with a health savings account (HSA) could save you money in the long run.

Coverage limits define the maximum amount an insurer will pay for a covered loss. In auto insurance, for instance, liability coverage might cap at $100,000 per person and $300,000 per accident. Exceeding these limits leaves you personally liable for additional costs. Here’s where analysis becomes crucial: assess your assets and potential risks to determine if your coverage limits are adequate. For example, if you own a home worth $500,000, a liability limit of $300,000 may leave you exposed in the event of a lawsuit.

Finally, the claim process is the moment of truth for any insurance policy. It typically involves notifying the insurer, providing documentation, and awaiting approval. Delays often stem from incomplete or inaccurate information, so keep detailed records of incidents, damages, and expenses. A persuasive argument for policyholders: familiarize yourself with your insurer’s claim procedures in advance. Knowing what to expect—and what’s expected of you—can streamline the process and reduce stress during an already challenging time.

In summary, a well-structured insurance policy is a symphony of premiums, deductibles, coverage limits, and claim processes. Each component serves a distinct purpose, and understanding their interplay empowers you to make informed decisions. Whether you’re selecting a new policy or reviewing an existing one, focus on these elements to ensure your coverage meets your needs without breaking the bank.

Nevada Insurance Broker Fee Disclosure: A Clear and Transparent Guide

You may want to see also

Explore related products

![]()

Insurance Providers: Comparison of companies, agents, brokers, and online platforms

Insurance providers come in various forms, each with distinct advantages and limitations. Companies operate directly, offering policies under their own brand, which can streamline communication but may limit product diversity. For instance, State Farm and Allstate provide bundled services like auto and home insurance, leveraging brand loyalty for cross-selling. Agents, often exclusive to one company, offer personalized service but are constrained by their employer’s product range. Brokers, in contrast, act as intermediaries, sourcing policies from multiple providers to tailor solutions to client needs, though this may involve higher fees. Online platforms like Policygenius or Lemonade democratize access, using algorithms to compare policies, but lack the nuanced advice a human agent or broker can provide.

Consider a 35-year-old homeowner seeking comprehensive coverage. A direct company might offer a 10% discount for bundling home and auto policies, but the terms may not be competitive. An agent could expedite claims processing due to direct company ties, yet their options are confined to their employer’s offerings. A broker might identify a niche provider with better flood coverage for a coastal property, albeit at a higher premium. An online platform could present 15 quotes in minutes, ideal for tech-savvy users, but the absence of human guidance could lead to oversight in policy details.

When evaluating cost efficiency, direct companies often win for bundled discounts, while brokers may secure better rates for specialized risks. Agents provide value through relationship-based service, particularly for complex claims. Online platforms excel in transparency, displaying side-by-side comparisons, but beware of hidden fees or exclusions buried in fine print. For instance, a $500 deductible on a health plan might save $200 annually, but ensure it doesn’t compromise essential coverage.

Practical tip: Before committing, ask providers for a coverage gap analysis. Companies and agents may offer this as part of their service, while brokers and platforms might charge a fee. For example, a broker might identify a $100,000 liability gap in a homeowner’s policy, justifying their higher cost through enhanced protection.

In conclusion, the choice of provider hinges on priorities: companies for simplicity, agents for personalized service, brokers for customization, and online platforms for convenience. A hybrid approach—using a platform to shortlist options, then consulting a broker for refinement—can maximize both efficiency and coverage quality. Always review policy details, not just premiums, to avoid costly surprises.

Does Allstate Insure Yachts? Coverage Options and Policy Details Explained

You may want to see also

Explore related products

![]()

Risk Assessment: How insurers evaluate risks to determine policy terms and costs

Insurance is a promise of financial protection, but it’s not a one-size-fits-all deal. Behind every policy lies a meticulous process of risk assessment, where insurers dissect potential dangers to tailor terms and costs. This evaluation isn’t arbitrary; it’s a science grounded in data, statistics, and predictive models. For instance, a 35-year-old nonsmoker with a healthy lifestyle will likely pay significantly less for life insurance than a 50-year-old smoker with pre-existing conditions. Insurers analyze factors like age, health, occupation, and lifestyle to gauge the likelihood of a claim, ensuring premiums reflect the risk involved.

Consider auto insurance, where risk assessment takes a more dynamic form. Insurers examine driving history, vehicle type, and even geographic location to determine rates. A teenager with a speeding ticket driving a high-performance car in a densely populated city will face higher premiums than a middle-aged driver with a clean record operating a sedan in a rural area. Telematics devices, which track driving behavior in real-time, further refine this process, offering discounts to safe drivers. This granular approach ensures that policy costs align with individual risk profiles, incentivizing safer habits.

For businesses, risk assessment is equally critical but more complex. Commercial insurers evaluate factors like industry type, revenue size, and safety protocols. A construction company with a history of workplace accidents will face higher liability premiums than a tech startup operating in a low-risk office environment. Insurers may also require on-site inspections or compliance audits to mitigate potential hazards. For example, a manufacturer might need to install fire suppression systems or train employees on safety protocols to secure favorable rates. This proactive approach not only reduces premiums but also minimizes the likelihood of costly claims.

The takeaway? Risk assessment is the backbone of insurance, shaping policies to fit individual and organizational needs. By understanding how insurers evaluate risks—whether through health screenings, driving data, or business audits—policyholders can take actionable steps to lower costs. For individuals, this might mean quitting smoking or improving credit scores. For businesses, it could involve investing in safety equipment or employee training. Ultimately, transparency in risk assessment empowers consumers to make informed decisions, turning insurance from a necessary expense into a strategic tool for financial security.

Uber Insurance Requirements: Must Your Name Be on the Policy?

You may want to see also

Explore related products

![]()

Claims Process: Steps to file, investigate, and settle insurance claims efficiently

Filing an insurance claim can feel like navigating a labyrinth, but understanding the process transforms it from daunting to manageable. The journey begins with notification, where policyholders promptly inform their insurer about the incident. This step is critical; delays can complicate or even void claims. For instance, auto accidents require immediate reporting, often within 24 to 48 hours, while property damage claims might allow up to 72 hours. Always check your policy’s specific requirements to avoid pitfalls.

Once notified, the insurer initiates investigation, a phase that demands meticulous documentation. Policyholders should gather evidence such as photos, police reports, medical records, or repair estimates. Insurers may dispatch adjusters to assess the damage firsthand, particularly for high-value claims. For example, a fire-damaged home might require a structural engineer’s report, while a medical claim could necessitate detailed treatment records. Transparency and accuracy during this stage are non-negotiable; discrepancies can lead to denials or delays.

The settlement phase is where efficiency meets fairness. Insurers evaluate the claim based on policy terms, coverage limits, and the evidence provided. For instance, a health insurance claim might cover 80% of hospitalization costs after a deductible is met, while a car insurance claim could reimburse up to the vehicle’s market value. Policyholders should review the settlement offer carefully, questioning any discrepancies. If dissatisfied, they can appeal, often requiring additional documentation or a third-party review.

To streamline the process, policyholders should maintain open communication with their insurer, keep detailed records, and understand their policy’s nuances. For example, knowing whether your auto insurance includes rental car coverage can save time and frustration post-accident. Similarly, being aware of exclusions—like flood damage in a standard homeowners policy—prevents unrealistic expectations. By proactively engaging in each step, policyholders can transform a potentially stressful claims process into a smooth, efficient resolution.

Retired Military: What Life Insurance Benefits Are Available?

You may want to see also

Frequently asked questions

Insurance coverage typically includes financial protection against specific risks or losses, such as medical expenses, property damage, liability claims, or loss of income. The exact coverage depends on the type of insurance policy (e.g., health, auto, home, life) and the terms outlined in the contract.

Insurance premiums are determined based on factors like the insured’s risk profile, the type and amount of coverage, and the insurer’s historical claims data. For example, auto insurance premiums may consider driving history, while health insurance premiums may factor in age and medical history.

An insurance policy document is a formal contract that outlines the terms, conditions, coverage limits, exclusions, and obligations of both the insured and the insurer. It typically includes sections like declarations (policy details), definitions, coverage descriptions, and claims procedures.

![Airbrush Foundation Set with Soft Makeup Brush, [Light Weight], [Long Lasting], [Anti-aging Ingredient], [Oil Control Formula], Full Coverage Foundation for All Skin Type, 02# Nude](https://m.media-amazon.com/images/I/61LXhNuTHsL._AC_UL320_.jpg)