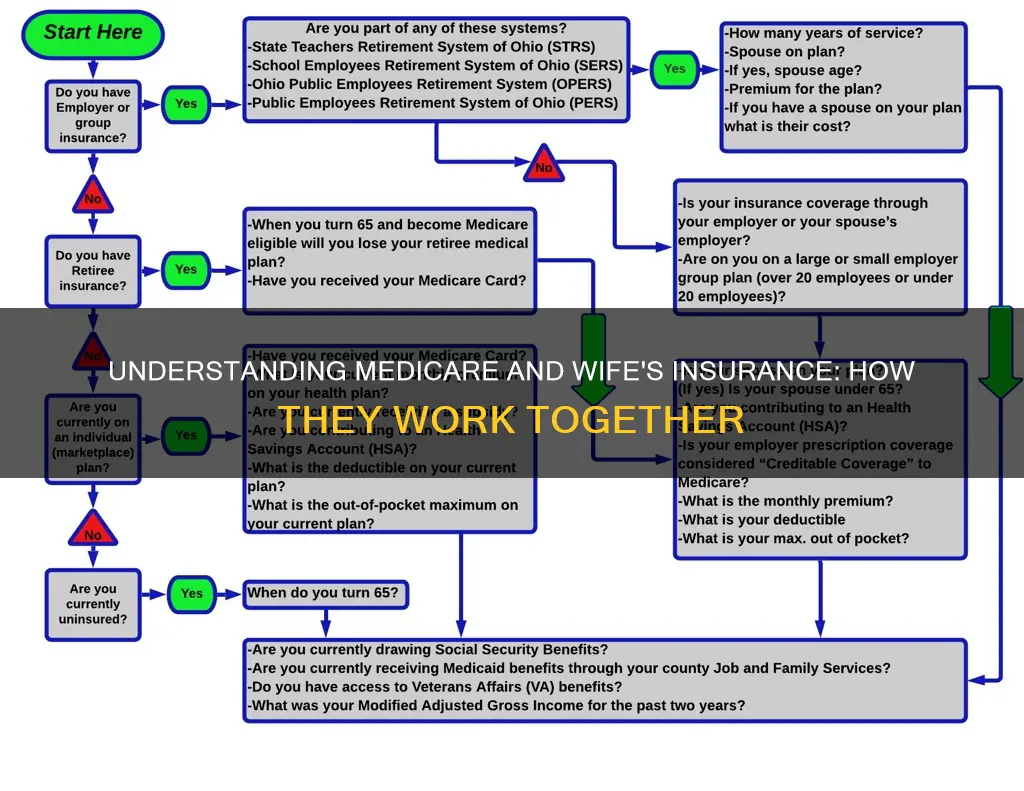

If you are covered by your wife's employer's health insurance plan, you may not need to sign up for Medicare at 65. This depends on the size of the company she works for and the type of coverage you have. If her company has 20 or more employees, it is considered a Group Health Plan (GHP), and your insurance will pay primary. In this case, you don't need to sign up for Medicare Part A and Part B at 65, as the company-sponsored health insurance will continue to pay medical bills first. However, if her company has fewer than 20 employees, it is considered a Small Group Health Plan (SGHP), and your insurance will pay secondary to Medicare, so you will need to sign up for Parts A and B when you turn 65 to avoid gaps in coverage.

Explore related products

$19.95 $9.07

What You'll Learn

![]()

Medicare Parts A, B, C and D

Medicare is a federal health insurance program for individuals aged 65 and older, and some people under 65 with certain disabilities or conditions. It has four parts: A, B, C, and D.

Part A

Part A covers inpatient care in hospitals, skilled nursing facility care, hospice care, and home health care. Most people get Part A premium-free at the age of 65 based on taxes paid while working. However, some people also pay a premium for Part A.

Part B

Part B is also included in Original Medicare. You are responsible for a monthly premium for Part B. You can also shop for and buy supplemental coverage that helps pay your out-of-pocket costs (like your 20% coinsurance). If your spouse is not working and is 65 years old, they can enroll in Part A and Part B when you do, without being penalized for late enrollment.

Part C

Part C, also known as Medicare Advantage, is an alternative to Parts A and B that bundles several coverage types, including Parts A, B, and usually D. It may be offered by a private company that offers an alternative to Original Medicare for your health and drug coverage. These plans may have different out-of-pocket costs than Original Medicare.

Part D

Part D helps cover the cost of prescription drugs. You must sign up for Part A or Part B before enrolling in Part D. You can get Part D by joining a Medicare Advantage Plan with drug coverage or by joining a separate Medicare drug plan in addition to Original Medicare.

Shutdown Impact: Medicaid Insurance Status and Your Coverage

You may want to see also

Explore related products

![A Monster With A Thousand Heads [English Subtitled]](https://m.media-amazon.com/images/I/91Lv2l7wzzL._AC_UL320_.jpg)

![]()

Medicare supplement insurance plans

Medigap plans are structured alphabetically, with Plans A through G providing benefits at higher premiums and limited out-of-pocket costs, while Plans K through N are cost-sharing plans offering similar benefits at lower premiums but with higher out-of-pocket expenses. The availability of these plans may vary depending on the state and an individual's specific circumstances. For example, Plans C and F are not available to individuals new to Medicare after January 1, 2020, and Plan F also offers a high-deductible option in certain states.

When it comes to a spouse's insurance working with Medicare, it's important to understand that Medicare plans are issued to individuals only. Each person, even if married or in a domestic partnership, must have their own separate plan. However, a spouse can be covered as a dependent under their partner's employer-sponsored insurance, which can work hand-in-hand with Medicare. Additionally, Medicare allows for coordination of benefits, where multiple payers (such as Medicare and a group health plan) are involved. In such cases, the primary payer pays up to its coverage limits and then sends the remaining balance to the secondary payer.

It is always recommended to consult with the employer's health care benefits department and insurance providers to understand how Medicare interacts with existing coverage and to make informed decisions about health insurance options.

Applying for Medical Insurance in Nevada: A Step-by-Step Guide

You may want to see also

![]()

Medicare and employer insurance

Medicare plans are issued to individuals only, meaning each person has their own separate plan, even if married or in a domestic partnership. This means that your wife's insurance will not automatically work with your Medicare. However, there are some ways that your wife's insurance may influence your Medicare plan.

Firstly, if your wife has insurance through her employer, you may not need to sign up for Medicare at 65. This depends on the size of the company your wife works for. If it is a large employer, defined as a company with 20 or more employees, you do not need to sign up for Medicare at 65. The company-sponsored health insurance will continue to be what pays medical bills first, as the primary payer. In this case, you can stick with your insurance plan as long as you have "creditable coverage". This means that Medicare considers it to be as good as Part D. You should receive a notice from the plan provider every September letting you know whether your coverage is creditable. If you lose this coverage, you will be eligible for a special enrollment period to purchase a Part D plan without incurring a late enrollment penalty.

If your wife's company has fewer than 20 employees, you will need to sign up for Medicare Parts A, B, and likely D if Medicare is meant to pay primary. In this case, your insurance will pay secondary to Medicare. You should ask your wife's HR representative if the insurance is creditable. If you do not have creditable coverage, you should apply for Medicare Parts A and B.

If you are covered by your wife's employer plan and eligible for Medicare, you have a few options. You can enroll in Medicare Parts A & B, Part D prescription drug coverage, or a Medicare Advantage (Part C) plan. You can also add a Medicare supplement insurance plan to Original Medicare (Parts A & B) to help with out-of-pocket costs. You can enroll as early as three months before the month in which you turn 65. This is the start of your Initial Enrollment Period, which also includes the month of your 65th birthday and the next three months. If you are able to delay enrolling, you will have a Special Enrollment Period of eight months that begins when the employer coverage is lost or when your wife retires.

How Long Do Accidents Affect Insurance Rates?

You may want to see also

![]()

Medicare and prescription drug coverage

Medicare prescription drug coverage, also known as Medicare Part D, is available to those aged 65 and over who are enrolled in Medicare Parts A and B. If you are under 65, you may still be eligible for Medicare due to disability or End-Stage Renal Disease. It is important to note that your Medicare insurance policy covers only you, and your spouse or family members cannot be included in your coverage. Your spouse must have a separate, individual policy.

If you have Medicare and other health insurance, each type of coverage is called a "payer". The "primary payer" pays up to the limits of its coverage, and then sends the rest of the balance to the "secondary payer". If the secondary payer does not cover the remaining balance, you may be responsible for the remaining costs. This order of payment is called "coordination of benefits".

There are two main ways to get Medicare drug coverage. Firstly, you can join a Medicare Advantage Plan (Part C) or other Medicare health plan with drug coverage. You will get your Part A, Part B, and Medicare drug coverage (Part D) through a single plan. You must have Part A and Part B to join a Medicare Advantage Plan, and you will usually get your drug coverage through that plan.

The second way to get Medicare drug coverage is to join a separate Medicare drug plan. If you are in a Private Fee-for-Service Plan that does not include Part D, you can join a separate Medicare drug plan without losing your current health coverage. However, if you are in a Health Maintenance Organization, HMO Point-of-Service Plan, or Preferred Provider Organization, and you join a separate drug plan, you will be disenrolled from your Medicare Advantage Plan and returned to Original Medicare.

If you have creditable coverage through your spouse's private insurance, you do not need to sign up for a Part D Prescription Drug plan. However, if you do not have creditable coverage, you have a special enrollment period of 63 days after your coverage ends to enroll without penalty.

Starbucks' Medical Insurance: What You Need to Know

You may want to see also

![]()

Medicare and retirement plans

Medicare plans are issued to individuals only. Each person has their own separate plan, even if married or in a domestic partnership. Your spouse or family members cannot be included in your coverage. For your spouse to have Medicare coverage, they must have a separate, individual policy.

If your spouse is younger than you and not working when they turn 65, they may be eligible to receive Medicare benefits based on your work record even if you are not retired or receiving Medicare coverage yourself. If your spouse is younger than 65 and receives disability benefits from Social Security for a period of 24 months, they automatically become eligible for Medicare on the 25th month.

If your spouse is not working and is 65 years old, they have the option to remain on your employer health insurance policy while simultaneously enrolling in Medicare Part A (with no premium) if you have reached 62 years of age. You and your spouse can enroll in Original Medicare Part B when you reach the age of 65 without being penalized for late enrollment if your employer health insurance coverage is comparable to what Medicare recipients receive.

If your spouse works for a company with 20 or more employees, that's considered a Group Health Plan (GHP), and your insurance will pay primary. In a Small Group Health Plan (SGHP) with less than 20 employees, your insurance will pay secondary to Medicare, so you need to sign up for Parts A, B, and likely D if Medicare is meant to pay primary.

If you have Medicare and other health insurance, each type of coverage is called a "payer." The "primary payer" pays up to the limits of its coverage, then sends the rest of the balance to the "secondary payer." If the “secondary payer” doesn’t cover the remaining balance, you may be responsible for the rest of the costs.

Friday Health Insurance: Is It Medicaid or Private?

You may want to see also

Frequently asked questions

No, Medicare plans are issued to individuals only. Each person has their own separate plan, even if married or in a domestic partnership.

If you have Medicare and your wife has other health insurance, each type of coverage is called a "payer". The "primary payer" pays up to the limits of its coverage, then sends the rest of the balance to the "secondary payer". If the secondary payer doesn’t cover the remaining balance, you may be responsible for the rest of the costs.

If your wife has creditable coverage through her private insurance, she does not need to sign up for Medicare. Her private insurance coverage is creditable if she works for a company with at least 20 employees.

If your wife's company has fewer than 20 employees, her insurance will pay secondary to Medicare, so she needs to sign up for Parts A, B, and likely D if Medicare is meant to pay primary.