Reckless driving is a surefire way to see your insurance rates increase. A reckless driving conviction is a sure sign to insurance companies that a driver is a risky investment, and they will act accordingly. A reckless driving conviction can affect your insurance rates for 3-5 years, and in that time, you could be paying up to 70% more than before your conviction. In some cases, your insurer might not renew your policy at all. While defensive driving courses can help mitigate this increase, it's best to avoid reckless driving altogether to avoid the financial penalties that come with it.

| Characteristics | Values |

|---|---|

| Impact on insurance rates | Increase in insurance rates |

| Duration of impact | 3-5 years |

| Severity | Varies depending on the state and insurer |

| Insurer response | Possible non-renewal of policy |

| Mitigation | Defensive driving courses, switching insurers, checking for discounts |

| Factors considered by insurers | Driving record, age, driving history, car type, mileage, credit history |

Explore related products

What You'll Learn

![]()

Reckless driving convictions and insurance renewal

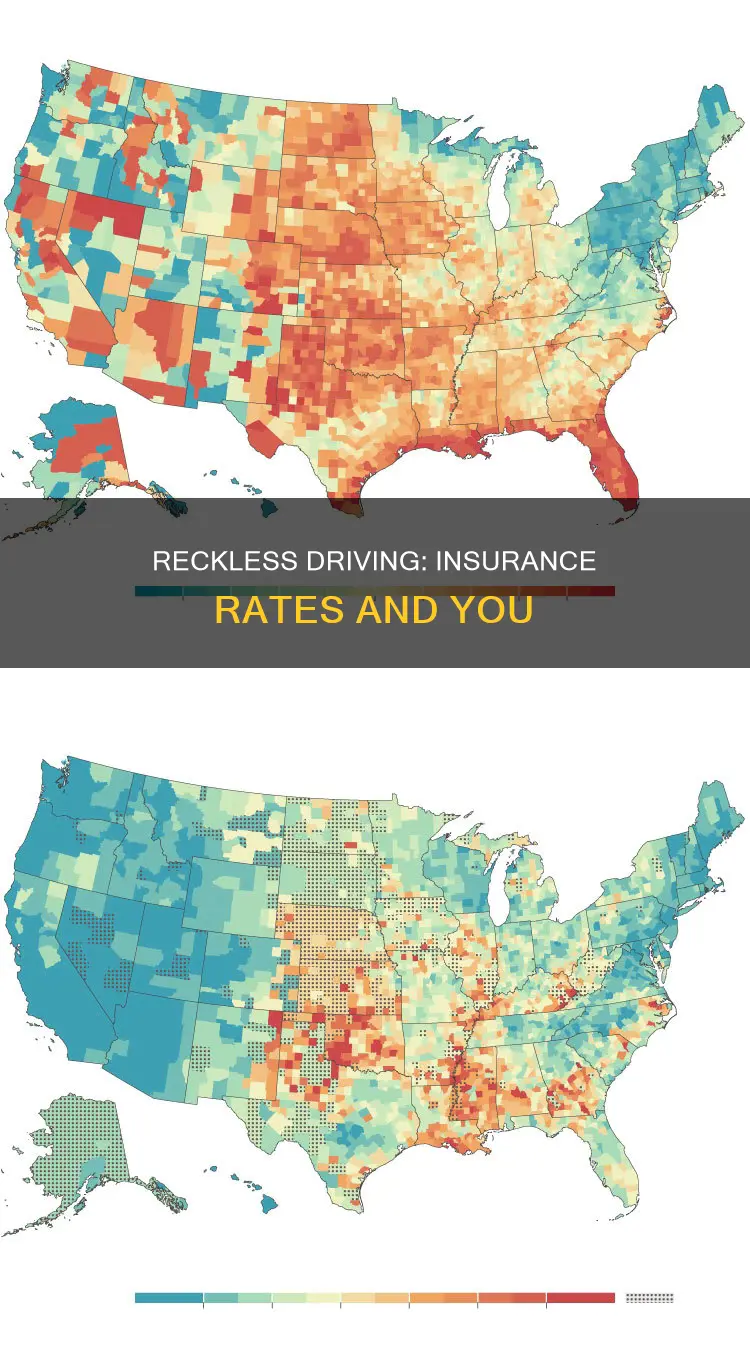

Reckless driving convictions can have a significant impact on insurance renewal, with insurance companies considering such convictions a major violation. This can result in increased insurance costs, with the exact amount depending on factors such as the policyholder's state and insurance company. For example, in Michigan and California, insurance rates can increase by 163% and 147% respectively after a reckless driving ticket. On the other hand, Florida has the lowest rate increase of 37%. Reckless driving convictions can also result in other consequences such as jail time, fines, and license suspensions, which can further impact insurance renewal.

Insurance companies evaluate the risk associated with a driver's history and take into account various factors when determining insurance rate increases. These factors include age, driving history, car type, and mileage. Accumulating points on a driving record due to reckless driving convictions can lead to increased insurance rates, with some states having a corresponding percentage increase in insurance premiums for each point. Additionally, insurance companies may consider the presence of injuries or property damage in reckless driving cases, with injuries often resulting in higher penalties.

The impact of a reckless driving conviction on insurance renewal can vary depending on the driver's history and the specific circumstances of the conviction. For example, a single reckless driving conviction may result in a smaller increase in insurance rates compared to multiple convictions within a short period. Insurance companies may also offer accident forgiveness programs that take into account factors such as the length of time with the insurance company and the driver's age. Additionally, drivers can explore legal options and take precautions to mitigate the impact of a reckless driving conviction on their insurance renewal, such as checking for discounts or shopping around for the best rate.

While a reckless driving conviction can have significant financial implications, it is generally considered less financially crippling than a DUI offense. This is because reckless driving is often classified as a "serious violation", whereas a DUI is typically classified as a "major violation". As a result, insurance companies may charge higher rates for DUI offenses compared to reckless driving. However, it is important to note that the specific algorithms used by insurance companies to calculate rates are not released, and each company may offer a different rate to the same driver.

Overall, a reckless driving conviction is likely to result in increased insurance rates and can have long-lasting consequences on a driver's insurance record. It is advisable for drivers to understand the legal and financial implications of reckless driving and take the necessary precautions to avoid such convictions to mitigate the impact on their insurance renewal and driving privileges.

Auto Insurance Policy for Teenagers in Texas: When to Add

You may want to see also

Explore related products

![]()

How insurers calculate insurance rates

Reckless driving will undoubtedly impact your insurance rates. A reckless driving conviction shows insurance companies that the driver is willing to take unnecessary risks when operating a motor vehicle, and insurers will see such a driver as a risky investment. This results in higher insurance rates.

Insurers calculate insurance rates based on factors that indicate how likely a driver is to file a claim. These factors include age, driving history, car type, and mileage. Each insurer will offer a slightly different rate to the same driver, as the specific algorithms used to calculate prices are not released. However, certain patterns can be observed:

- New drivers are seen as riskier investments, so their rates are higher than older drivers.

- A reckless driving conviction is treated as a four-point violation and results in points being added to a driver's record. Accumulating points leads to increased insurance rates.

- A reckless driving conviction can lead to an insurer not renewing a driver's auto insurance policy.

- A reckless driving incident that results in an injury and a claim on bodily injury liability coverage will increase insurance rates.

- A reckless driving incident that leads to property damage to the car in excess of a certain amount will also increase insurance rates.

- In most states, credit history is used to determine car insurance rates. There is a correlation between bad credit and filing claims, with people with good credit seen as more responsible.

- Traffic violations, such as speeding or failure to yield, can cause insurance rates to rise.

- Other factors that can increase insurance rates include DUIs, bad credit, and speeding tickets.

Does Towing a Boat Affect Your Auto Insurance?

You may want to see also

Explore related products

![]()

Reckless driving and driving records

Reckless driving significantly affects both your driving record and insurance rates. Reckless driving is a four-point violation, and accumulating points on your driving record can lead to increased insurance rates, potential driving privilege suspensions, and other penalties. A reckless driving conviction is generally considered a "major violation" by insurance companies, indicating that the driver has the potential to take unnecessary risks when operating a motor vehicle. These risks can lead to accidents with expensive insurance claims for injuries or property damage.

Insurance companies evaluate risk based on a driver's entire driving history, not just the points. A reckless driving ticket is usually enough to cause a large increase in premiums because most insurance companies classify it as a "serious violation". The increase in insurance rates due to reckless driving varies depending on the state and insurance company. For example, in Michigan and California, the insurance rates increase by 163% and 147%, respectively, while in Florida, the average increase is only 37%. On average, reckless driving convictions increase insurance rates by 82% or $1,568, while DUI offences can double insurance rates.

The number of points accumulated by a driver can also have a correlating percentage increase in insurance premiums. For instance, a violation that is equal to 1 point may result in a 25% increase. Reckless driving in Virginia is a 6-point ticket, and these points are assessed against a driver's record and can be used to suspend a person's license if enough points are accrued. However, a driver can avoid these points on their license by pleading nolo contendere (no contest) to a charge of reckless driving, although this is subject to a judge's approval and the driver not having pleaded no contest to another moving violation within the last five years.

In addition to the number of points, insurance companies consider various other factors when determining insurance rate increases, such as the driver's age, experience level, length of good driving, and whether the reckless driving case involved injuries to other persons. Some insurance companies also have accident forgiveness programs where they may waive a surcharge as a result of an accident, taking into account factors such as the length of time a driver has been with the insurance company and the driver's age.

Maximizing Auto Injury Insurance Claims: Coding and Billing Tips

You may want to see also

Explore related products

![]()

Reckless driving and insurance costs for new drivers

Reckless driving is a serious offence that can have significant consequences for new drivers, including an increase in insurance costs. A reckless driving conviction indicates to insurance companies that a driver is more likely to take unnecessary risks, leading to potential accidents and subsequent insurance claims. As a result, insurance companies view reckless driving as a "major violation", similar to drunk driving or hit-and-run incidents.

For new drivers, a reckless driving conviction can result in substantially higher insurance rates. New drivers are already considered riskier investments by insurance companies, and adding a reckless driving charge to their record can cause a substantial increase in their premiums. The exact increase in insurance rates will depend on various factors, including the driver's age, driving history, car type, and mileage. Additionally, each insurance company uses its own algorithms to calculate rates, resulting in slight variations in the quotes offered to the same driver.

The impact of a reckless driving conviction on insurance rates can be long-lasting. In most states, reckless driving remains on a driver's record for an extended period, affecting insurance rates for 3-5 years. During this time, drivers may find it challenging to obtain affordable insurance coverage, as insurers are under no obligation to provide favourable rates or even offer a policy to high-risk drivers.

To mitigate the financial consequences, it is advisable for new drivers to contest reckless driving charges with the assistance of a skilled defence attorney. A successful defence could result in reduced charges or dismissal, thereby minimising the impact on insurance rates. Additionally, new drivers can explore opportunities to lower their insurance premiums by taking advantage of discounts offered by insurers, such as pay-in-full or defensive driving discounts. Shopping around and comparing rates from different insurance companies can also help identify more affordable options.

While a reckless driving conviction can have significant financial implications for new drivers, taking proactive steps to improve their driving record and demonstrate responsibility can help reduce the long-term impact on their insurance costs.

Gap Auto Insurance: Getting Your Refund

You may want to see also

Explore related products

![]()

How to reduce insurance rates after reckless driving

Reckless driving is a serious violation that can have a significant impact on insurance rates. A reckless driving conviction indicates to insurance companies that the driver is willing to take unnecessary risks, which can lead to accidents and costly insurance claims. As a result, insurance providers may increase premiums, refuse to renew policies, or even cancel coverage altogether. The increase in insurance rates varies depending on the state, insurance provider, and driving record, with some states like Hawaii seeing increases of up to 242%, while others like Texas see increases as low as 41%.

- Shop around and compare rates from different insurance providers. Each insurance company calculates premiums using its own system, so it's important to get multiple quotes.

- Check for discounts offered by your insurer, such as pay-in-full or defensive driving discounts.

- Improve your credit score. Insurance companies often use credit history to determine car insurance rates, and there is a correlation between bad credit and filing claims.

- Fight the ticket in court, if possible. In some cases, an attorney may be able to get a moving violation reduced to a non-moving violation, which can help keep points off your driving record and maintain lower rates.

- Consider switching to an insurance provider that specialises in high-risk drivers. These providers may offer more competitive rates for drivers with reckless driving convictions.

It's important to note that a reckless driving conviction will typically impact insurance rates for 3-5 years. During this time, it's crucial to drive safely and avoid any further violations that could further increase insurance costs.

Erie Auto Insurance: Understanding Extended Coverage Options

You may want to see also

Frequently asked questions

Yes, reckless driving is likely to impact insurance rates. A reckless driving conviction is a sure sign to insurance companies that the driver is a risky investment, which will lead to an increase in insurance premiums.

This depends on the insurance company and the state. On average, insurance rates increase by $858 in Texas after a reckless driving ticket.

A reckless driving conviction will impact insurance rates for at least three years, which is how long violations typically stay on a person's driving record. In most cases, the impact lasts between 3-5 years.

There are a few ways to reduce insurance rates after a reckless driving conviction. Some insurance companies offer discounts for drivers who take defensive driving courses. It is also worth checking what other discounts your insurer offers, such as a pay-in-full discount. Another option is to switch insurers to find a better deal.

Insurance rates are calculated based on factors that indicate how likely a driver is to file a claim, including age, driving history, car type, and mileage. Other factors that impact insurance rates include credit history, previous traffic violations, and the number of drivers on the policy.